.png)

Generative AI has a wide range of applications in the financial services industry, with the technology helping to increase security, aid in risk management, and even predict upcoming market trends. However, there is one particular use case that promises to have a broad impact on every niche – customer service.

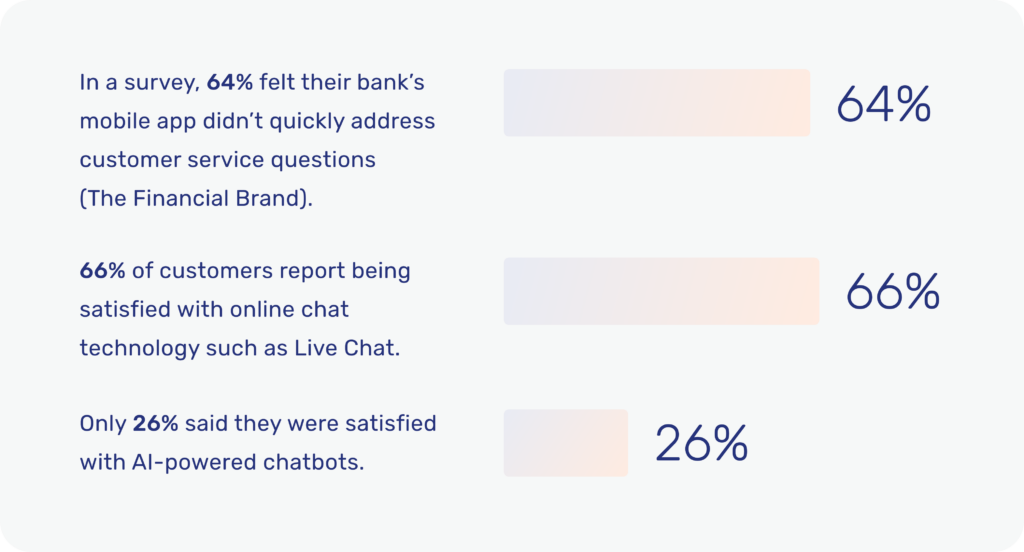

The importance of the customer experience in the banking industry is well documented, and poor service can have a wide-ranging negative impact on customer perception. It could be the 64% of respondents that felt let down by their banking app or inconsistent experiences across channels.

But one specific area of customer service has had a more turbulent relationship with customers than most. While 66% of customers report being satisfied with online chat technology such as Live Chat, only 26% said they were satisfied with AI-powered chatbots. Another survey found that 80% of customers who have used chatbots to inquire about financial products would prefer to not use them again.

Where have chatbots gone wrong in the past?

From the very beginning, artificial intelligence chatbots have been a valuable asset to businesses, drawing on vast amounts of information to boost efficiency and help customers to take care of more simple queries.

So, why haven’t they always been received so well in the banking industry?

The technology was still maturing

When chatbots first became viable tools for customer service, they were adopted by businesses in the financial services sector and beyond with enthusiasm. However, expectations of what organizations thought chatbots could do didn’t necessarily stack up with reality at first.

This was particularly noticeable with regard to understanding emotions. If a customer is contacting their bank for a delicate situation, a chatbot’s response can be less than encouraging.

Say, for example, a customer is having difficulty making payments on a loan and are looking for financial advice or repayment options. It can be an emotional situation and finding the best way forward requires tact and understanding on the part of the agent, something that chatbots weren’t able to identify.

In these cases with complex issues, the responses to user queries or the advice to customers could leave a lot to be desired. For this reason, concerns among customers rose with them believing that the technology couldn’t live up to expectations.

Poor initial implementation practices

Some of the issues with chatbots in the banking industry have been to do with poor implementation plans. A statistic from 2018 found that even though 90% of organizations had chatbot technology, only 4% were using them effectively.

Retail banks’ chatbots, particularly earlier models, required a holistic strategic implementation plan to ensure success. There are a number of areas where failures happened. In some cases, organizations overestimated the effectiveness of the chatbot, expecting it to take care of more complex queries than it was capable of. In other cases, there wasn’t the understanding that the bot needed to be actively trained to their specific use cases. It could also have been a training issue, with customer support teams unable to fully understand how the bot integrates with their own interactions.

Whatever the reason, there were widespread teething issues that affected customer satisfaction and perception. What’s more, to a large extent, these issues are in the past. Fast forward to 2022 and a Deloitte survey found that around 90% of companies were able to resolve complaints more quickly using chatbots and 80% could process higher numbers of calls and contacts.

Struggles with customer engagement and personalized experiences

This is again related to a misunderstanding of the technology’s maturity at the time. When they first came on the market, chatbots had relatively specific use cases for carrying out routine tasks. While they used natural language processing and artificial intelligence, they were essentially smarter versions of more standardized knowledge banks.

It was more a way to access information more easily using relevant keywords than having a bot that was able to truly understand intent and carry out a conversation. For more complex financial operations or loan applications, this was an issue.

With active training, these bots became more powerful but they were still unable to reach the levels of personalization that customers expected – or were told to expect to make informed decisions.

Perceived risks and the privacy of customer data

Security is always top of mind with banking customers. They have low risk tolerance and believe that the potential risks associated with new technologies pose a threat. While financial institutions spend a lot of time and effort on risk management, customers can be slower to convince.

The issue here, particularly in retail banks, is generally one of education and communication. The security measures and fraud detection sensors are just as robust as with any other channel. Any suspicious activity or potential fraud is quickly investigated to avoid financial losses.

Not being transparent enough

Finally, one of the biggest oversights that financial institutions made was to not be upfront about their chatbots. There were two ways that this was a problem.

The first was by not making it clear to customers that they were interacting with a chatbot from the beginning. When customers expected answers from an agent and received chatbot responses instead, the initial reaction was negative. However, if the customer was informed at the beginning that it was a chatbot, they would temper their expectations and have more patience.

The second issue was not educating the customer on how chatbots should be used and the benefits to customers. Many customers interacted with older models of chatbots expecting the kind of experience that LLM-powered versions are able to provide – years before the model was released. This overselling of the capabilities meant that customers were inevitably disappointed with the results and customer adoption was low.

How Generative AI banking integrations are changing the game

There’s no denying that Generative AI technology represents a huge leap forward in terms of what’s possible for providing financial advice or support. Before we get into the specifics, it’s important to remember they already have a strong foundation, strengthened over years of the technology maturing.

A seamless experience around the clock

A key benefit of retail banks’ chatbots is their ability to be active 24/7 and on the channels that customers prefer. It doesn’t matter if it’s web, mobile apps, messaging apps, or whatever else, customers can gain access to the most frequently asked questions that are asked in financial services contexts. As companies train their specific bots, these resources only become more powerful.

Cost centers become revenue generators

Customer service centers in retail banks have long been considered a necessary expense. However, with chatbot features like intelligent routing and greater support efficiency, contact centers are able to better deal with customer queries. By increasing customer satisfaction, agents have more options to leverage the moment of truth and pitch useful financial products.

The Generative AI financial services edge

So, where does Generative AI come in? In general, it enhances all of the benefits of a normal chatbot and human support to achieve shorter sales cycles and better performing First Contact Resolution. More specifically, we can break it down into three specific use cases.

Increased comprehension for better support

Sentiment analysis is a key part of the chatbot experience as the variety of language that we naturally use is immense. Even if the information is available, the human language input needs to match the perceived intent.

This has always been a substantial sticking point for customers, who quickly become frustrated when a bot doesn’t understand their query – particularly for complex questions.

With large language models, the natural language processing capabilities have transformed. As a result, bots are much better able to understand long-tail intents and provide more accurate, human-like responses.

Assistive Intelligence for superior advice

Beyond this, technologies such as GPT, also assists agents or advisors during live chats by suggesting responses. This boosts efficiency of individual Live Chat interactions in a retail bank use case, resulting in hyper-personalized insights for faster support and better resolutions.

Likewise, it helps wealth management clients to make more informed investment decisions by aiding finance professionals with more information. This is because the suggested responses allow financial advisors to double check their advice at the moment of interaction.

Self-training support

Finally, no matter the financial industry chatbot, it needs to be properly trained to each organization’s individual context to truly perform. Generative AI enhanced machine learning capabilities allows it to aid in its own training. The bot trainer assistant can suggest better intents alongside the appropriate responses, making it possible to increase accuracy more quickly.

Ensure a robust customer experience with Unblu

Artificial Intelligence (AI) undoubtedly represents a competitive advantage for the financial services industry, aiding in everything from taking care of common questions to providing valuable insights that ensure a more personalized customer service.

However, to properly address the complexities of the customer journey and ensure strong connections with customers, it needs to be properly implemented.

Unblu’s Generative AI-powered chatbot can be applied to a range of banking applications, helping provide effective customer care and next-level advice even for complex tasks, while ensuring all regulatory requirements are adhered to.

What’s more, our team is on hand to help with the initial setup and can provide ongoing support to ensure excellent experiences for customers or clients.