.png)

Digital banking is reaching a point of no return. For years now, the trends have been pushing at greater speeds toward digital innovation, with customer preferences firmly shifting in favor of faster and more varied digital service options. Across demographics, the customer experience needs to be omnichannel – meaning that customers enjoy a flexible, seamless, and streamlined service on the digital channel (or in-person one) of their choosing.

However, there are still plenty of questions, challenges, and uncertainties that are standing in the way of true digital transformation. The current state of digital banking is defined by interplays between challenges and opportunities; speed and caution; and technology and traditional, in-person authenticity.

Online banking service statistics reveal a lot about our current context and the successes and failures that are shaping the new face of digital services in the finance sector.

Key trends at a glance

The statistics below will be discussed in more detail throughout the article. Here’s what you need to know at a glance. Read our digital banking trends article for more in-depth insights.

Global adoption: Mapping the digital banking explosion

While these individual trends highlight shifting consumer behaviors, the collective momentum is driving a massive reallocation of capital across the financial sector. The scale of this shift is reflected in the financial outlook of the sector. The digital banking market size 2030 projections indicate the global market will reach $79.4 billion, growing at a CAGR of 14.5% from 2024. Much of this growth is fueled by the digital banking services segment, which records higher growth as institutions prioritize engagement over simple utility.

This growth is supported by a massive expansion in the global user base. The number of digital banking users worldwide continues to climb, with recent data showing that over 53% of the global population has now migrated to digital-first banking. This widespread adoption accelerates the need for scalable support that maintains a personal touch. As more users enter the ecosystem, successful banks will be those that view customer service as their primary value driver. By humanizing their digital footprint, they aren't just managing money – they're claiming market share through resonance and trust.

Customer loyalty in banking: The "Relationship Gap"

In previous years, we reported that while 62% of banking customers had an “effective” experience, only 48% described it as “emotionally positive”. Now, in 2026, this lack of emotional connection has become a critical business risk. New research from Accenture reveals that despite massive digital investment, most banking relationships remain “functionally correct but emotionally devoid”.

The cost of this emotional disconnect is high. Digital banks that successfully bridge this gap – landing in the top 20% for customer advocacy scores – grow their revenues 1.7x faster globally and 2.6x faster in North America. Without this bond, digital banks risk what analysts call “building leaky buckets,” where new customers are acquired through the front door only to quietly exit through the back due to a lack of customer engagement.

The human element in a digital-first world

To stop this attrition, traditional and challenger banks must focus on two key areas:

- Prompt Resolution: 58% of customers currently believe their bank is failing to deal with queries in a timely manner, which remains the most important factor in satisfaction.

- The Hybrid Balance: While AI expansion is inevitable, the human touch remains the gold standard for trust. Deloitte found that 58% of consumers are less inclined to use a service provided solely by AI, reinforcing the need for a hybrid approach that keeps human experts accessible.

The economics of digital engagement

The shift to digital is fundamentally changing the cost of doing business. The average customer acquisition cost (CAC) for digital banks vs traditional banks remains a point of contrast, with digital-native firms maintaining a 60% to 70% lower cost base. However, ECB data shows digital-only banks spend three times more on marketing than traditional peers.

This dynamic directly impacts the customer lifetime value (CLV) digital banks vs traditional institutions can achieve. A Forrester report found that 87% of banking customers who feel valued will stay with their bank, significantly boosting long-term profitability. While traditional banks maintain a trust score of 87 compared to 74 for neobanks, they must leverage this trust by adopting seamless, high-touch digital journeys that prevent "silent attrition."

The mobile experience plateau

Mobile banking is now the dominant remote channel across the EU for both research (ranging from 62% to 83%) and purchases (typically above 60%). However, usage does not equal excellence. While the hesitation to use mobile has vanished, the expectation for quality has skyrocketed – leading 60% of customers to rate current advanced features as merely 'average'.

Areas of progress in digital banking platforms

Overall, the banking sector has achieved reasonable levels of digital transformation. In total, 71% of global businesses are now digital, although 53% of surveyed banking executives claim their organization is still working on improving their digital transformation efforts by implementing more advanced financial technology.

These initiatives are primarily focused on increased revenue generation – according to 77% of surveyed executives. Aside from this, decision makers value improved customer experiences, increasing operational resilience, and strengthening regulatory compliance.

Some traditional banks are falling behind

Despite the clear shift in consumer behavior, a notable segment of traditional institutions remains stalled. Currently, 19% of surveyed banks are lagging behind necessary transformation benchmarks: 1% report no interest in digital shifts, 8% have no formal implementation plans, and 10% remain stuck in the planning phase.

This lack of progress is largely attributed to internal friction. One-third (33%) of these institutions cite strategy-related challenges as their primary inhibitor, while nearly 30% struggle with data silos and project management hurdles that prevent them from moving beyond the "vision" stage.

Address "The Onboarding Hurdle"

The "front door" of digital banking remains leaky. Recent data from Capgemini found that 47% of prospective customers abandon digital onboarding mid-process. The primary culprit is a lack of automation; currently, only 29% of data collection is automated using AI. This manual friction explains why 86% of bank executives now plan to prioritize omnichannel experiences over the next 12 months.

As the ecosystem expands, so do the risks. Digital banking fraud statistics reveal that while certain traditional fraud types have stabilized, the sophistication of AI-powered social engineering is rising. To disrupt these attacks, organizations are fusing cyber and fraud intelligence across fragmented data sources, ensuring that security measures protect the journey without creating the friction that leads to onboarding abandonment.

New explorations of physical and digital experiences

In 2026, we’re seeing a further blending of the physical and digital to get a leg up on rival banks and better respond to customer demands.

Physical branches hold their footing: From "Indispensable" to "Orchestrated"

The narrative that digital would kill the branch has reached a point of no return – but not in the way many predicted. Instead of bank branch closures, the physical branch has found its footing as a psychological anchor for financial security.

Recent JD Power reporting shows that 72% of customers continue to use their local branch at the same frequency as previous years, with 38% considering them indispensable. This sentiment is backed by Accenture’s 2026 data, which reveals that 63% of global consumers still desire a physical location to help manage their finances.

The "handoff problem"

While the desire for a physical presence remains high, the experience of moving between digital and physical channels is often where the relationship breaks down. This is what experts call the "Handoff Problem".

Currently, 64% of consumers rely on branches specifically for conflict resolution, yet they frequently encounter "fragmented data orchestration". In plain English: the person at the branch often has no idea what you just did in the app. Solving this data handoff has become the top strategic priority for 2026.

Evolving formats and the "Human Touch"

The branch of the future isn't just a smaller version of the branch of the past. It’s becoming more specialized and tech-enabled:

- Smart Formats: 76% of consumers are now willing to use micro-branches or smart banking booths for their needs.

- In-Depth Services: Customers are moving away from using branches for simple tasks, with 64% requesting more self-service tools for basic transactions.

- The Mortgage Gate: High-stakes decisions still require a human anchor, only 39% of consumers feel comfortable obtaining a mortgage entirely online.

Even in markets like France, where 25% of digital consumers now use remote video or voice calls to discuss new products, the ease of access to a "human touch" remains the deciding factor in their loyalty.

For more insight into the future of bank branches, download our ebook!

{{branch-paper-cta1}}

Remote branch channels

A new phenomenon of remote branch visits is likely to become more important as the line between digital and physical experiences continues to blur. Currently, remote access to branch staff plays a modest but notable role throughout Europe, especially in Italy (17%), Portugal (14%), and Spain (14%) for purchases. Other countries show single-digit use, highlighting regional differences in adoption of hybrid service models, although this may change as it becomes more common.

The mobile-first era: Reaching the "Boomer Milestone"

For years, digital banking users were hesitant to use mobile banking apps for intricate digital financial services and activities due to trust issues or technological constraints.

That hesitation has officially vanished. Mobile banking adoption and usage statistics show the channel is now the "universal standard." According to the American Bankers Association, 54% of Americans now cite online and mobile banking apps as their top banking method.

For the first time, 38% of Baby Boomers now prefer mobile apps over online banking via a PC. Forward-thinking banks are moving beyond simple apps to offer high-touch tools like co-browsing and instant document collaboration.

From accessibility to superior experience

With mobile dominance now a prerequisite, the competition has moved to the granular level of user experience. Financial organizations that can deliver a seamless, unified, and comprehensive journey are the ones standing out in 2026.

One of the most effective ways to enhance this experience is through Mobile Collaboration. Forward-thinking banks are moving beyond simple apps to offer:

- Preapproved Loans: Providing instant, easy access to credit directly within the mobile interface.

- Co-Apping: This collaborative banking tool allows agents and customers to browse the app and review documents together in real time.

- Proven Results: One Unblu customer reported that agents initiated 300,000 Co-Apping sessions in a single year to resolve issues – nearly five times the volume of traditional web-based Co-Browsing.

By prioritizing these high-touch digital tools, banks can ensure that the mobile experience feels personalized and supported, rather than just transactional.

From Generative to Agentic AI: The productivity leap

The impact of Artificial Intelligence on the financial services sector has moved beyond simple cost efficiency. While early GenAI models improved productivity by 22–30% and drove a 6% revenue increase in retail banking, the conversation has now shifted toward Agentic AI.

Unlike standard chatbots, Agentic AI acts as a sophisticated productivity tool for human staff. McKinsey reports that these systems are already returning 10–12 hours per week to bankers, effectively increasing their coverage capacity by 40%. This allows employees to shift their focus toward high-value human skills – oversight, complex design, and deep customer interaction.

The Zero-Click Future and AI Agents

By 2026, the very way customers interact with their bank will change fundamentally. Forrester predicts a "Zero-Click" future where human visits to bank websites will drop by 20%.

This isn't due to a lack of interest, but a surge in machine-initiated traffic. AI agents, acting on behalf of the customer, are expected to increase by 40%, handling routine queries and transactions without the user ever needing to open an app or website.

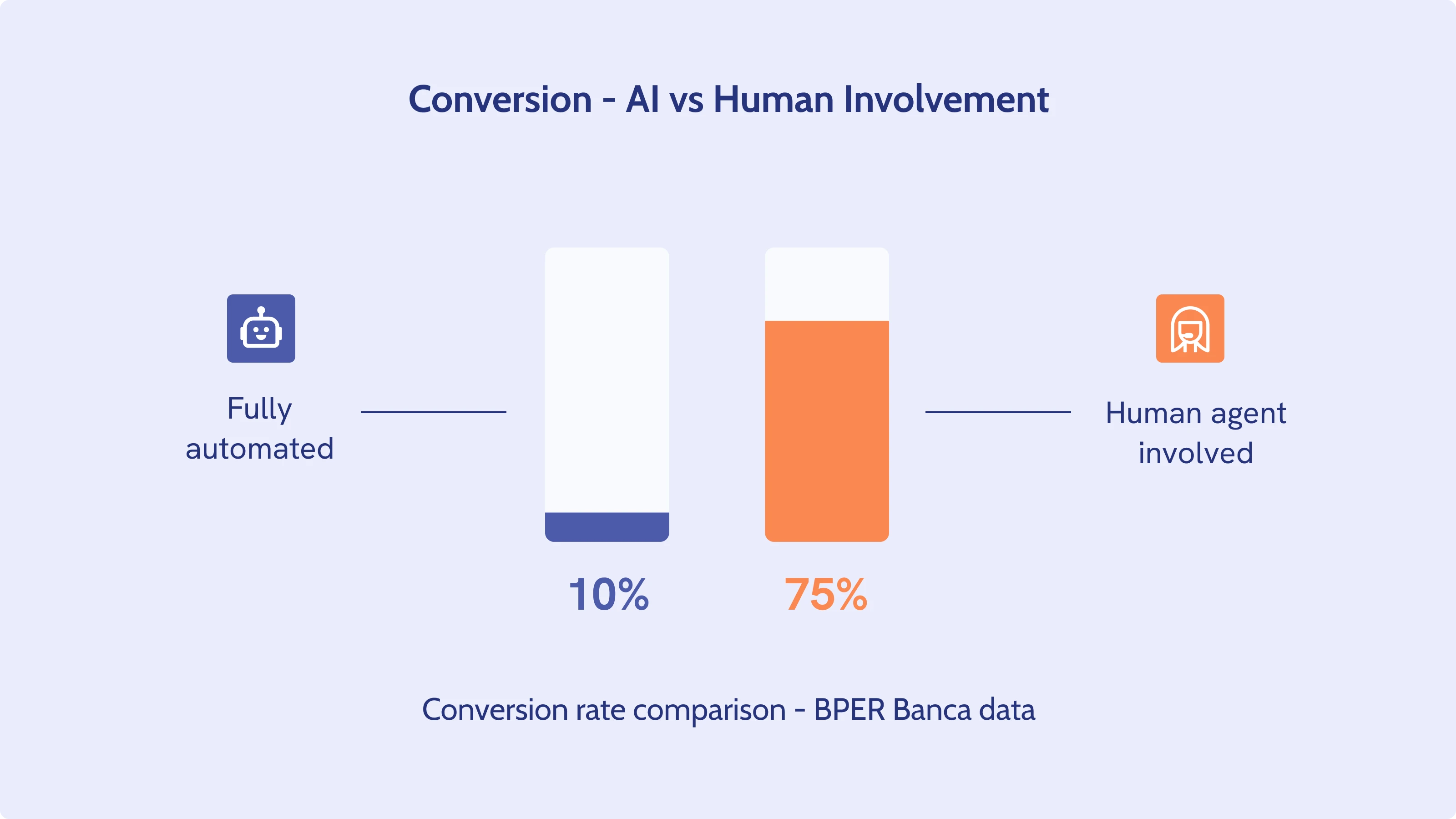

Balancing AI with Human Intelligence

Despite these technological leaps, the "Human Touch" remains the anchor for conversion. Data from BPER Banca highlights that while a fully automated tech experience might see a 10% conversion rate, that number jumps to 75% when a human agent is involved in the process.

Current trends suggest that while AI provides the reach and speed, human intelligence provides the trust and finality needed for complex financial decisions.

Online banking usage and Unblu

The changing context in digital banking is proving challenging for traditional banks and digital banks alike. Online banking statistics and consumer demands are clearly showing that digital banking services must be exceptional to meet customer expectations.

The fact is, the number of digital banking channel users is growing and providing top conversational banking capabilities is the only way to ensure customer satisfaction. Of course, this is easier said than done. The nature of competition is moving more towards the granular level, with mobile banking services, digital tools, digital platforms and more having to offer a greater service experience to stand out. Combined with enhanced focus on security measures and regulations, the digital banking landscape is undoubtedly complex.

That said, the banks that are able to keep ahead of digital banking trends and offer convenient access to support will gain the loyalty of digital banking users and succeed in 2026.