.png)

The retail banking landscape in 2026 is defined by a paradoxical challenge: digital adoption has peaked, yet customer trust remains fragile. While inflation has stabilized, persistent geopolitical uncertainty continues to weigh on consumer sentiment, requiring bank leaders to move beyond simple agility toward deep strategic foresight.

In this environment, technology is no longer just a tool for operational efficiency; it is the primary driver of emotional resonance and customer advocacy. The stakes are measurable: research indicates that banks with high advocacy scores grow revenues 1.7x faster than their peers. Yet, a significant gap remains, as most current digital channels are still described by customers as "emotionally devoid."

As digital transformation becomes the standard baseline – with over 50% of bank decision-makers now actively advancing these initiatives – differentiation no longer hinges on mere digital presence. Instead, long-term success is determined by delivering truly customer-centric, omnichannel engagement that prioritizes humanized, seamless collaboration across all touchpoints.

To maintain engagement without increasing risk exposure or falling behind shifting global regulations, banks must move toward a model that fosters trust through "Digital Memory" and agentic intelligence. Despite the uncertainty of a fractured geopolitical landscape, 2026 offers promising opportunities for those ready to bridge the gap between digital technologies and human empathy.

Customer Experience in Retail Banking

Customer experience in retail banking is one of the definitive areas that determine long-term success in a retail environment. As digital transformation has largely become standard across incumbents, with over 50% of bank decision-makers actively advancing these initiatives in 2026, differentiation now hinges on delivering truly customer‑centric, omnichannel engagement (Unblu’s post on banking customer experience trends).

The fact is, top-tier customer experience in retail banking today means more than digital presence – it means humanized, seamless collaboration across all touchpoints backed by measurable business impact.

This is especially true when we consider the overarching trends that are reshaping the industry. Yes, it will be challenging. But, despite these challenges, there are many promising opportunities mixed with the uncertainty.

Here’s our pick of what key trends you should look out for in 2026.

1. Continued economic uncertainty

It has been a difficult few years for citizens around the world, with the crisis of the global pandemic giving way to geopolitical instability and high interest rates. As the Financial Conduct Authority in the UK said in an open letter to retail banks:

“We saw market stresses including geopolitical tensions, volatile asset prices, weak global growth, inflationary pressures, and rising interest rates. The cost of living rose significantly, putting pressure on the finances of households and small and medium enterprises (SMEs).”

While interest rates are much lower in 2026, many of the other factors remain the same, with a fractured geopolitical landscape that threatens escalation at all times. To further complicate matters, there has been an almost unprecedented global shift in political rulers as the historic year for global elections leaves feelings of trepidation regarding how new entrants will act upon their mandate. Deloitte highlights this as one of the key messages for retail banks, advising them to “keep on their toes” as we enter a brave, somewhat unfamiliar, world.

The outlook is not entirely pessimistic for traditional banking institutions, however. A PwC report highlights how increased regulation on Big Tech and other non-traditional players could “push technology players out of the industry and increase barriers to entry” – resulting in an opportunity for banks to rebuild trust among the customer base.

Other cautious opportunities appear to be rearing their head in the coming year, including a boost in noninterest income (impacting topline growth), hope for credit quality normalization, and higher deposit costs to control interest rates.

2. Solving the “emotional deficit”

As we move into 2026, a stark reality has emerged: digital channels have become functionally efficient but emotionally devoid. While the industry has mastered the "how" of digital transactions, it has often neglected the "why" behind customer loyalty. According to the Accenture Global Banking Consumer Study (2025), banks that achieve high customer advocacy grow revenues 1.7x faster than their peers. Yet, most digital interactions remain cold and transactional, failing to build the trust necessary for long-term retention.

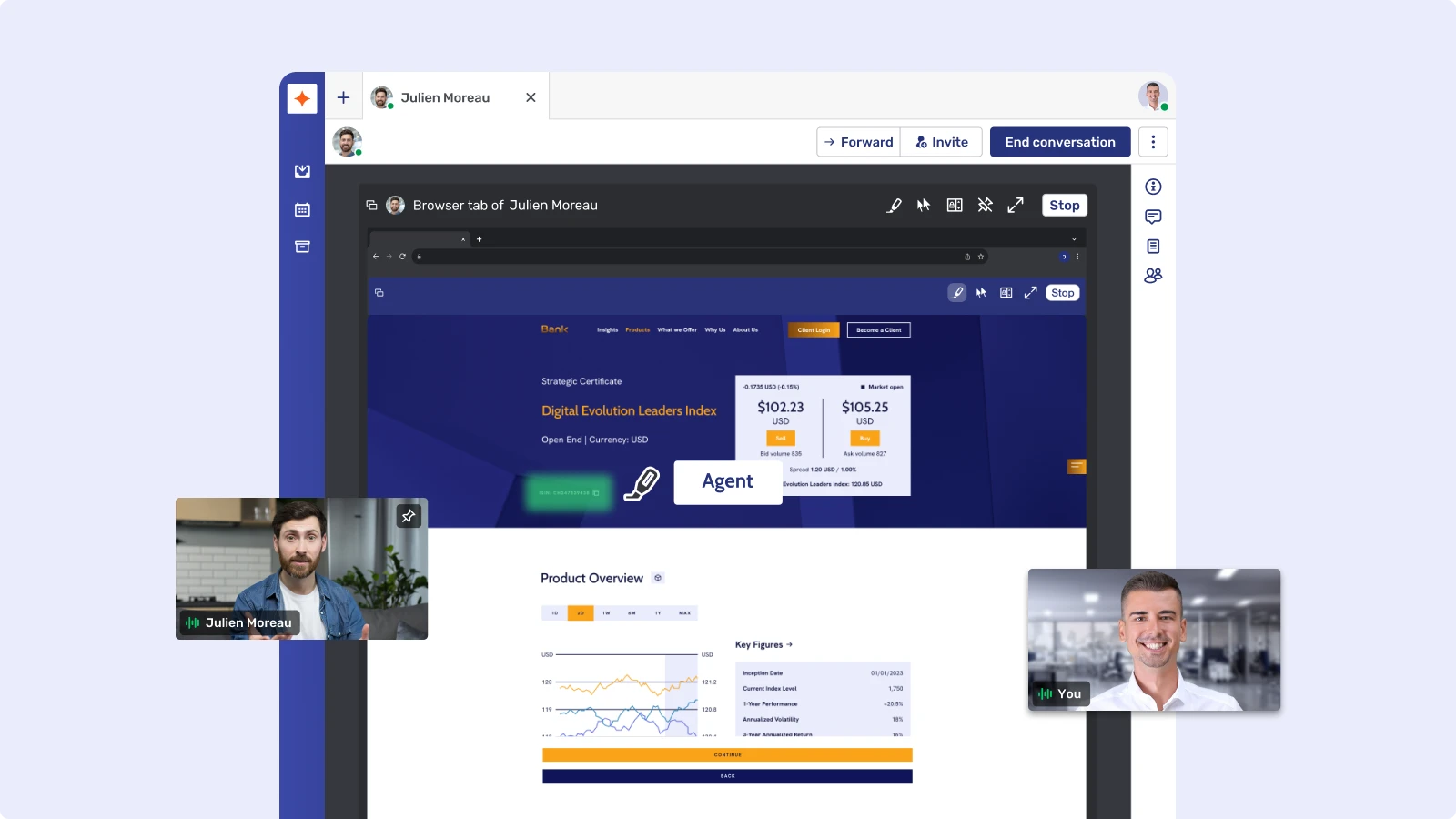

Deloitte reports that 50% of retail clients still choose their primary bank based on personal referrals rather than digital advertising, highlighting that human connection remains the ultimate differentiator. To foster true loyalty, institutions must transition from merely "correct" service toward emotional resonance. This requires leveraging high-touch digital tools – such as Co-Browsing and video chat – that simulate the warmth and reassurance of a face-to-face meeting, finally bridging the gap between digital convenience and human empathy.

3. From transformation to agentic autonomy

In 2026, the focus for retail banking has decisively shifted from incremental digital changes to Agentic Orchestration. Banks are now adopting what McKinsey calls the “Agentic Paradigm,” moving past isolated AI projects to implement interoperable AI agents that manage entire workflows, from complex mortgage applications to real-time fraud monitoring.

This strategic pivot to Agentic Intelligence is essential for combating the high rate of customer abandonment during digital onboarding, a critical issue highlighted by Capgemini’s 2025 World Retail Banking Report, which found that 47% of customers quit the process due to a poor experience. Advanced AI agents can autonomously resolve application obstacles as they arise.

The move allows traditional retail banks to transition to an "agent-augmented" model, where automation enhances the human connection rather than replacing it. For example, automating regulatory compliance can free up human staff, enabling them to provide high-empathy support precisely when a customer is struggling. McKinsey estimates this can cut report preparation time by 30% to 50%.

4. Mobile banking & in-app collaboration

Mobile apps have officially become the "heart of the relationship" for retail banking, with users averaging 150 interactions per year. However, despite this high frequency, most engagement remains shallow as 45% of weekly usage is limited to checking balances, while 31% is dedicated to basic money transfers.

This suggests that while the "mobile-first" battle has been won, the "engagement-first" battle is just beginning. To protect profitability, incumbents must look beyond the "neobank effect" of mere convenience and focus on in-app advisory collaboration.

By integrating features like Unblu’s Co-Apping, retail banks can transform these frequent, low-complexity touchpoints into high-value sessions. This allows advisors to meet customers exactly where they are – inside the app – to provide real-time guidance on complex financial products, turning a simple transactional tool into a powerful engine for customer advocacy and embedded finance.

5. Establishing "digital memory" for omnichannel mastery

The industry is currently navigating a paradoxical crisis: while digital adoption is at an all-time high, the "hand-off" between channels remains fundamentally broken. The world has gone digital, yet Accenture reveals that 64% of consumers still rely on physical branches for conflict resolution when digital channels fail. The problem? Most are forced to "start over" due to a lack of cross-channel data orchestration.

In 2026, the competitive benchmark is Digital Memory – the ability of an institution to maintain a single, high-fidelity conversation across every touchpoint. While 86% of banking executives now prioritize seamless omnichannel interactions, a massive execution gap remains. Only 21% of service executives currently view customer service as a value driver; the rest still operate under the legacy "cost center" mindset.

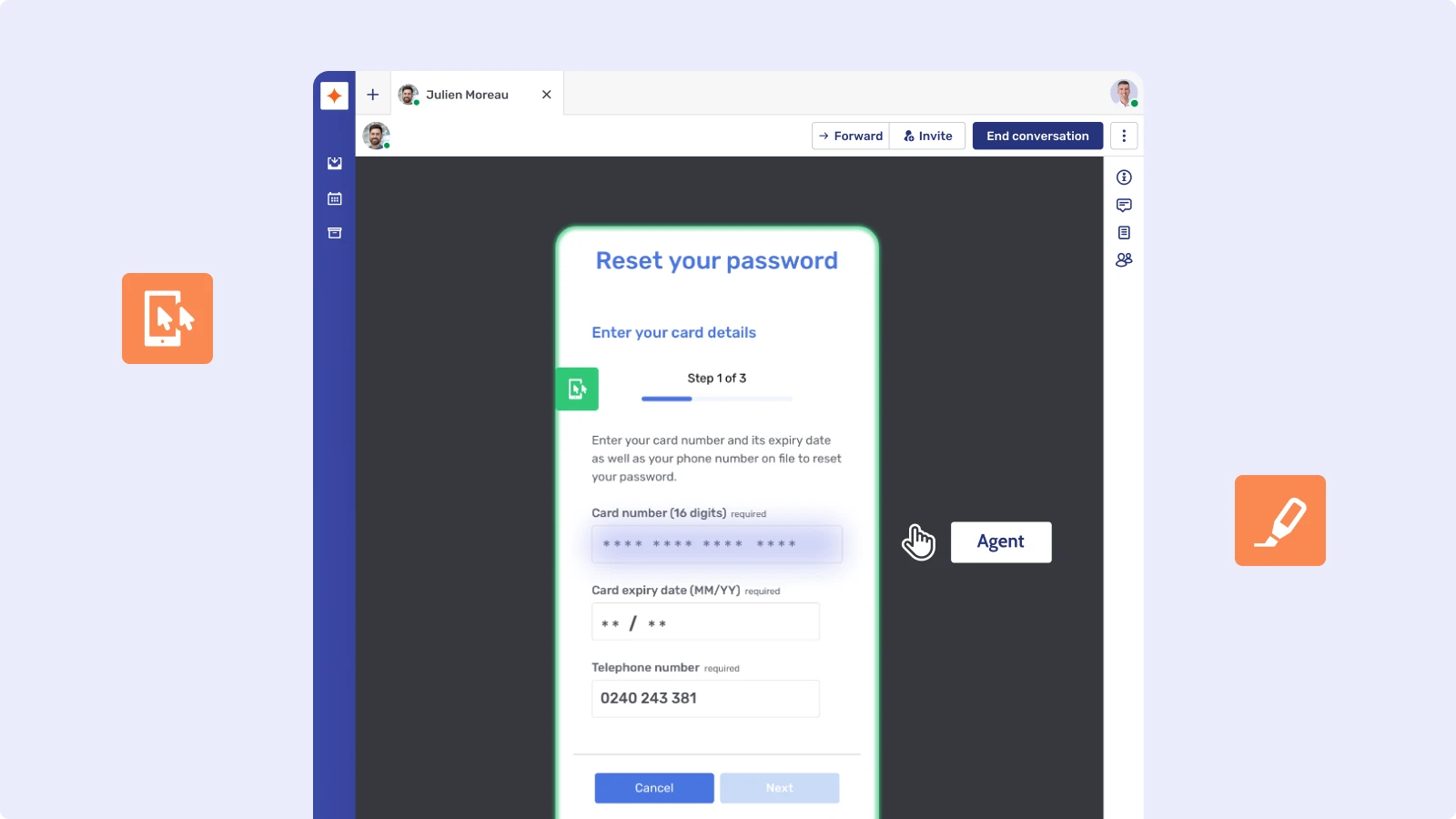

To bridge this gap, tech-forward leaders are implementing interaction layers that provide:

- Persistent Context: Ensuring a live chat initiated in-app is visible to a branch advisor in real-time.

- Seamless Escalation: Moving from an AI agent to a human-led Co-Apping session without losing a single data point.

- Frictionless Resolution: Eliminating the "repetition tax" customers pay when forced to restate their problem.

By institutionalizing Digital Memory, banks can finally redesign branches as specialized experience centers. Whether providing a tangible anchor of trust during economic volatility or offering tailored financial guidance hubs, this approach transforms the branch from a siloed physical space into a high-touch extension of the digital journey.

6. A continued upward trend of ESG

Despite economic uncertainties and financial concerns among consumers, the demand for sustainable practices and products continues. In fact, the emphasis on green consumerism and consciousness remains a significant priority for customers.

Last year, we reported that 66% of global consumers identify sustainability as a primary factor influencing their purchasing decisions, with 32% of consumers anticipating paying a premium for sustainable products, ranging between 22% and 44%.

However, a majority of consumers, totaling 68%, express unwillingness to pay a premium for ESG-related products (Simon Kucher & Partners).

This year, a new report by KPMG found that 48% of customers prefer brands that align with their values, which is having an influence on banking strategies. While cost is still an issue, retail banks are emphasizing sustainability to a greater extent by integrating environmental and social impact measures into their core operations (KPMG).

7. New opportunities with Generative AI

Generative AI has matured from an experimental technology into a fundamental component of financial services.

Best practices for banks to implement artificial intelligence in retail banking services involve transitioning from reactive chatbots to proactive "Agentic AI" that operates with human oversight. Deloitte finds that while 53% of consumers use GenAI regularly, they still prefer human support for complex reassurance.

By deploying Unblu’s AI-human hybrid model, retail banks can ensure that autonomous agents handle routine reasoning while seamlessly escalating complex cases to expert advisors.

Productivity and cost efficiency

With Gen AI, productivity in the retail banking sector is expected to improve by 22-30%, while increasing revenues by 6%. The use cases that are expected to dominate retail banking industry operations include automating loan underwriting for up to $250,000 and reducing credit card delinquency rates by 32%.

The impact of AI

The impact of new AI-generated abilities are expected to result in more emphasis on uniquely human capabilities, particularly in key areas.

One example of this is with the Italian bank BPER, which has adopted a hybrid approach that balances technological advancements with human intelligence with promising results. The bank reports that cross-sell opportunities experience a 65% increase in the conversion rate when an agent is present, moving from just 10% with a fully tech experience to 75% when a human is involved.

Strategic Priorities for 2026

Based on the above information, here are what the strategic priorities should be for banks this year.

BPER: Strategy in action

See how the Italian bank BPER implemented their strategic initiative to create a new hybrid approach to banking. Read the case study.

Closing the Gap: The Path to Human-Centric Growth

As we look toward the remainder of 2026, the outlook for retail banking financial services is increasingly optimistic, provided institutions remain focused on the right priorities. Interest rates have stabilized and Generative AI has matured from a back-office experiment into a front-office engine for growth. However, the "engagement-first" battle is only just beginning.

The defining characteristic of successful banks this year will be their ability to harmonize digital speed with human empathy. By solving the "emotional deficit," institutionalizing "Digital Memory," and leveraging AI as a supportive partner rather than a replacement for staff, banks can eliminate the "repetition tax" and the friction that drives customers away.

In the end, technology is only as valuable as the trust it builds. Retail banking leaders who provide personalized, omnichannel experiences – whether in a physical experience center or through a mobile app – will do more than just weather the storm; they will secure long-term loyalty and drive the next era of revenue growth.