.png)

What’s in store for the retail banking industry and credit unions?

This year, customer experience is less about the big transformation initiatives and more about finding avenues for differentiation through customer-centricity to find that all-important competitive edge.

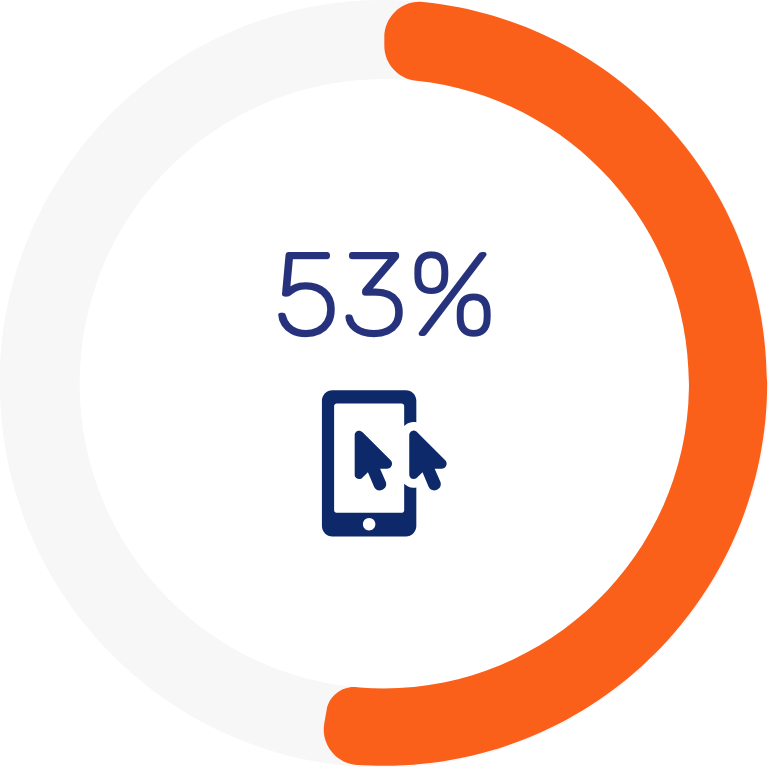

The forces of digitalization are easing as most retail banks have already attained a certain level of maturity, with only a few remaining that are starting entirely from scratch. Instead, the spotlight is now shifting towards continuous digital transformation progress. More than half (53%) of decision-makers at banks report ongoing efforts to enhance their digital transformation endeavors, marking a 20% increase since 2021.

Over half of bank decision-makers (53%) are actively advancing their digital transformation efforts.

Despite the overall positive trend, not all incumbent banks share the same success story. Surprisingly, 1% still claim they have no interest whatsoever in digital transformation, and another 8% have no plans for implementation initiatives. Moderately better, 10% are still in the planning phase, signifying that a combined 19% of global banking decision-makers have yet to leverage the potential of digital experiences.

For the 10% of retail banking organizations in the planning stage, a number of barriers are hindering progress. Among the surveyed individuals, 33% cite the company’s advanced technology strategy as one of the most challenging aspects of their role. This is accompanied by related challenges in data and project management, with 29% and 27% respectively.

Customer experience in banking refers to the overall perception a customer has of their interactions with a bank across all touchpoints – whether online, via mobile apps, over the phone, or in person.

It encompasses everything from how easy it is to open an account or get support, to how personalized and seamless the services feel. In today’s competitive landscape, delivering a consistent, intuitive, and emotionally satisfying experience is key to building trust, loyalty, and long-term value in banking relationships.

Customer experience trends across financial services

It’s worth noting that the trends below are largely tailored to the retail banking industry. If you would like to find out more about trends in the wealth management industry, we would recommend looking at our article here. For more general retail banking industry trends, you can find more information in this post – and for a digital banking focus you can find future industry-defining trends here.

Key trends in financial services

There are a number of key trends that must be harnessed in the retail banking sector and the financial services industry to improve customer experience.

1. Mobile-first communication channels

Contact center managers are continuing their efforts to streamline operations by reducing the complexity of vendor relationships they manage. The aim is to enhance customer choice and flexibility while delivering improved interaction experiences in online banking through features like video chat or Co-Browsing. A well-established system of this nature can alleviate frustration by eliminating the need for customers to repeat information or input details they’ve already provided.

However, when it comes to a mobile environment, there are less than stellar reports of customer satisfaction. One survey by Capgemini found that only 35% expressed high satisfaction with their banking app experience, with 59% unhappy.

As a result, with high levels of mobile app users, there is a mounting demand to offer these experiences within a mobile-first context. One crucial tool to enhance the conversational engagement experience in this context is Mobile Co-Browsing or Co-Apping. Despite being less commonly used compared to traditional Co-Browsing, there aren’t a huge number of solutions on the market and limited awareness.

Organizations that have embraced this tool are realizing substantial value in its application, both in avoiding poor experiences and maximizing remote human interaction. A recent example from a Unblu customer illustrates this, with their agents initiating 300,000 Co-Apping sessions to address customer issues in the first year, compared to approximately 65,000 traditional Co-Browsing sessions during the same period.

Neobanks grabbing the competitive market

Given poor experiences reported on traditional mobile banking applications, there has been an opportunity for innovative banks to grab a foothold. In Spain, the fintech company Revolut has managed to get nearly 20% of new customer accounts, more than traditional banks such as BBVA, Santander, and CaixaBank.

This is because neobanks are particularly good at delivering personalized services that appeal to younger demographics. The most convincing aspects appear to be customer service, advanced payment capabilities, swift onboarding and account setup, and personalized attention, according to a Capgemini report.

2. Branch are proving resilient

Recent years have shown us that traditional branches are struggling to remain viable. But this immense pressure to survive may taper off as individual consumer preferences align more closely with the availability of branches. According to a JD Power report, 72% of customers express their intention to utilize their nearby branch at a comparable frequency to the previous year, and 38% consider branches to be indispensable.

Broad-based trust in times of crisis

It is clear that branches maintain a crucial role in maintaining customer trust. One example of this was during the Silicon Valley crisis a few years ago. When the bank announced it needed to raise a substantial amount in funds, customer trust fell dramatically and over 42 billion dollars in deposits was withdrawn. This sparked a crisis that was felt around the world.

One report, however, found that the institutions that fared the best during this crisis were those that had strong branch networks. This shows the value that customers still place in having access to a branch when they are feeling insecure about their financial situation or their institution’s health.

Everyday branch banking

Of course, retail banks can’t maintain networks just for when crises emerge. So, what are the customer demands in retail bank branches?

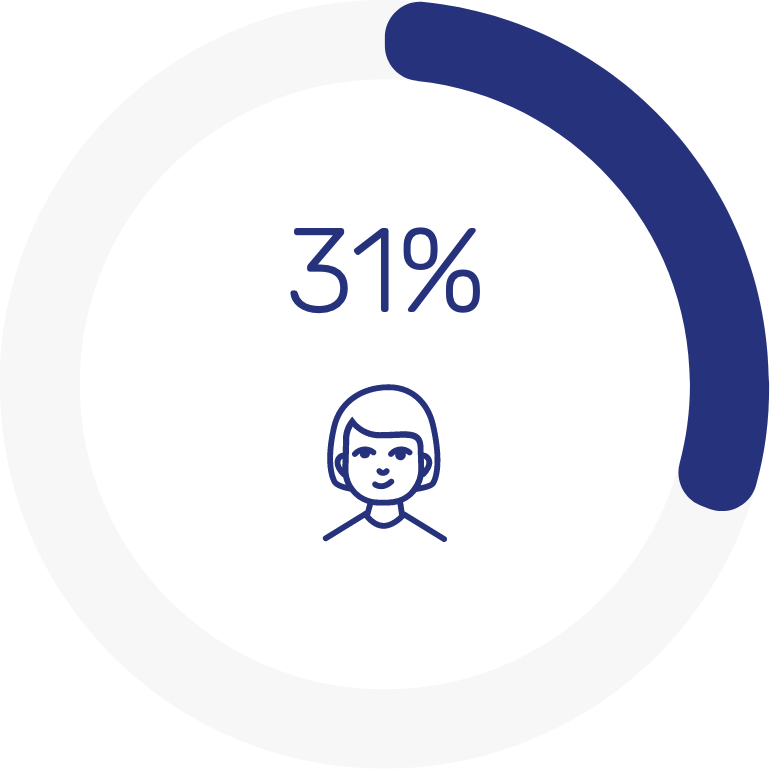

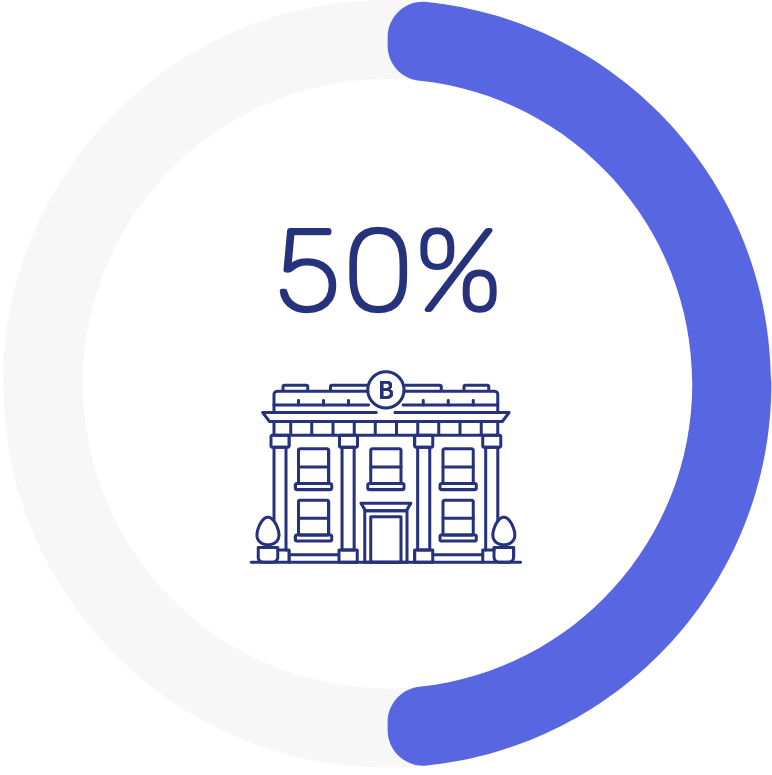

The majority of survey participants would like a more in-depth range of services at their branch. The most sought-after feature is self-service tools, with 64% of customers expressing a preference for them. Additionally, 44% are interested in co-working options, and 31% desire a more immersive and personalized experience. Nearly half of the respondents also indicated a desire for lifestyle products and offerings to be accessible at their branch.

44% of customers show interest in co-working spaces within their banking branches.

A significant 31% of customers are seeking a more immersive and personalized banking experience.

Nearly 50% of survey respondents want lifestyle products and services available at their bank branches

These enhanced options in an in-person environment is perhaps why Revolut is taking a gamble in 2025 with Smart ATMs that can offer much more than simple cash withdrawals. What remains to be seen is if these digital capabilities can overcome the lack of access to in-person support.

The fact is that the use of physical channels tends to grow as customers need more complex advice, with only 39% of consumers obtaining mortgages online. It appears that for complex financial products, having access to a human support agent is still necessary.

However, that being said, there are signs that customers are becoming more comfortable with even larger decisions taking place online. In France, for example, around 25% of digital consumers discuss potential new financial products with their advisors via remote channels , whether Video & Voice, Live Chat, or email. Additionally, nearly 30% of digital product purchases in the country are done through digital signatures. No matter the channel, what remains important is access to human advice.

Want to find out more?

3. Artificial Intelligence: Retail banks must step up and embrace technology

In a short time, Generative AI has moved from being an exciting new development in digital services to being among the most important tools in the entire financial sector.

It has the potential to automate operational tasks and enhance chatbot capabilities, impacting service metrics such as first-contact resolution rates.

This is important as 55% of banks globally (53% of Tier I banks and 58% of Tier II banks) reported FCRs below 70%, which shows room for improvement as 70% is the overall industry benchmark (Capgemini).

Banks need to embrace AI

But some financial institutions are proving slow on the uptake in providing access to technology. In fact, a survey of bank employees rated contact center automation and digitalization as low to moderate, with 81% citing a lower degree of digitalization (Capgemini).

Addressing queries more efficiently and effectively, resulting in enhanced customer satisfaction and lower call abandonment rates, should be a key area of focus in the coming year. This is because call abandonment can be representative of issues in financial technology and self-service at other points in the journey. A recent report found that Tier I banks have an almost 12% abandonment rate, which rises to nearly 18% for Tier II banks globally (Capgemini).

Other areas also require specific attention. One survey by Capgemini also found that staff currently allocate nearly 70% of their time to operational activities, leaving only 30% for ongoing and instant customer interactions (Capgemini). With Generative AI, it’s proving possible to shift employee focus from routine (and often dull) tasks to relationship-building and advisory roles.

What’s more, it’s now increasingly possible to leverage advanced conversational models to enhance chatbot responsiveness and resolution accuracy – hopefully improving on the 61% of bank customers who contacted agents due to poor chatbot resolutions (Capgemini).

Automation and personalization

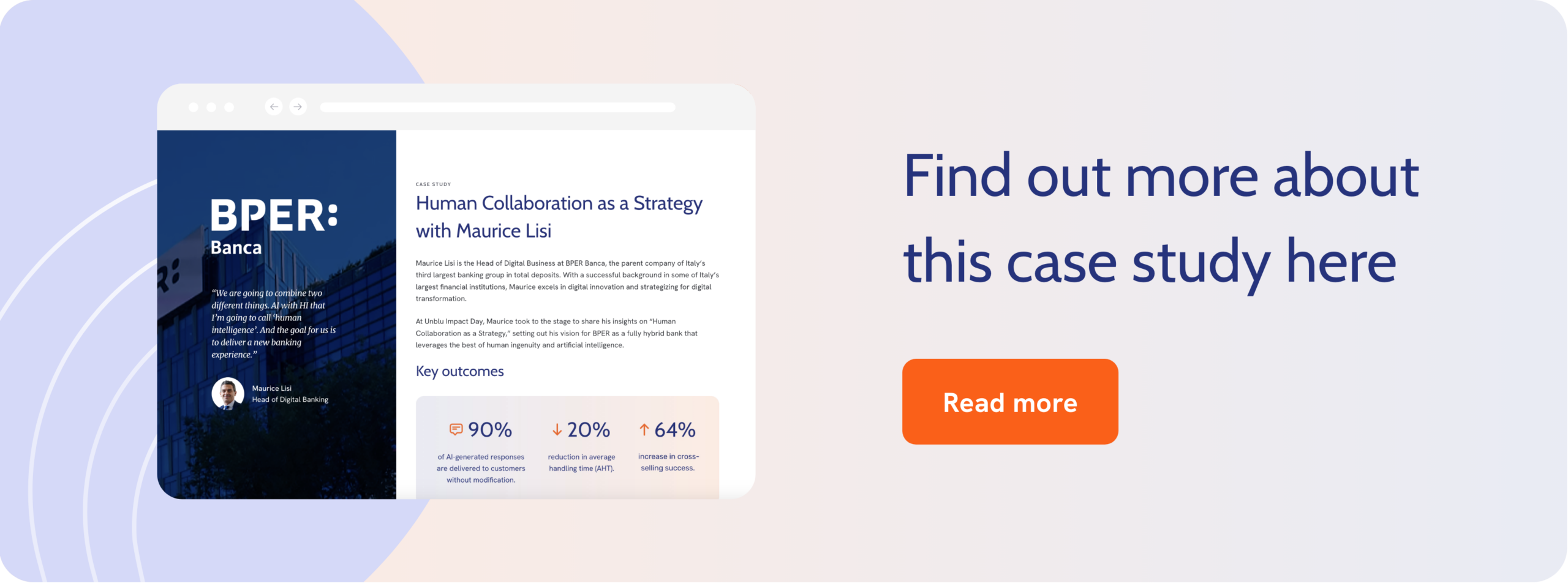

Success in this area requires achieving a balance between automation and human intelligence. One example of this being done well is at BPER Banca where Head of Digital Business Maurice Lisi based the digital strategy around these two pillars.

The Hey BPER virtual assistant leverages natural language processing and machine learning, aiming to handle up to 45% of incoming instant customer inquiries. The idea is to enhance efficiency and free human agents up to focus on more complex tasks – an approach that is proving essential as Generative AI becomes the norm.

4. Hyper-personalization: The opportunity of niche journeys

There is a growing trend of neobanks concentrating on specialized market segments tailored to specific target identities. Instances of this trend include Daylight, a banking platform for the LGBTQ+ community, Credit Karma specializing in loans, and Aspiration, which is dedicated to sustainability-focused banking.

However, not every neobank within these niches is guaranteed to thrive. For instance, Daylight has already declared its closure due to issues stemming from mis-management. Some may have to pivot or undergo acquisition since the market for these specialized offerings is not yet sufficiently mature for sustained expansion.

This doesn’t imply that these strategies lack value altogether. If anything, the emergence of inclusive finance has demonstrated the existence of a demand and potential profitability. Expanding on this, fintech companies or traditional institutions are likely to capitalize on this insight, possibly through acquisitions, to offer products and positive experiences tailored to extremely specific customer journeys.

Although these specialized journeys are not commonplace, when they do align with customer needs, they prove to be exceptionally effective. A case in point is Settld, a financial platform that specifically caters to individuals dealing with the loss of loved ones.

As we enter 2025, there is new evidence of how effective niche journeys are proving. In fact, advanced analytics and AI-powered tools that empower banks to tailor financial product recommendations have resulted in a 5x increase in click-through rates for personalized offers (Deloitte).

Of course, this is only as effective as the quality of the implementation. As KPMG argues, “the investment will be of little value if the emotional dimension of the personalization pillar is missed.” (KPMG)

5. A boom in embedded finance

Embedded finance – meaning the provision of financial services through non-financial channels – is undergoing a surge in growth. In total, 72% of those surveyed anticipate that a majority of financial products will be delivered through this method.

Several applications in Asia are taking the lead in this by integrating e-commerce, rewards, travel booking, on-demand services, games, and more into their lifestyle platforms. Notable instances include Singapore’s Grab and Indonesia’s Gojek platform, which utilize data from deliveries, taxi applications, and digital wallets to develop financial products for underserved customers. Through the utilization of open data, they can effectively evaluate risk levels even in the absence of credit reference agencies.

6. The benefits of social banking

AI-powered capabilities aren’t the only fad set to transform banking customer behaviors entirely.

Social media is changing the game and banks are increasingly using platforms like Instagram, TikTok, and YouTube to connect with younger audiences by building trust through authentic and engaging content (NTT Data).

In fact, a reported 35% of Gen Zs have used social media to search for information, compared to just 21% of Millennials. When we look at older generations, the percentage falls even further, with 13% of Generation X, 11% of Boomers, and only 9% of the Silent Generation using social media to this end.

Another source found that the number of 18-34 year old investors who use Reddit and TikTok to access financial knowledge has jumped dramatically in the last three years, moving from 17% to 26% on Reddit and from 12% to 20% on TikTok.

Strategies for experience-led growth in banking

As the financial industry pivots toward deeper personalization and customer-centricity, experience-led growth has become a strategic imperative. As McKinsey says, banks need to “reimagine, not just de-friction, priority journeys,” finding ways to deliver a smooth CX across touchpoints.

This means that banks in 2025 must prioritize customer experience not as a support function, but as a primary growth engine.

How can this be achieved? Here are some practical frameworks that can be used to implement interaction-based customer experience improvements into your context.

Practical frameworks

- The 3Cs Model – Context, Continuity, Convenience

- Context: Use customer behavior and intent data to personalize interactions in real time.

- Continuity: Ensure omnichannel consistency to ensure conversations continue across chat, video, email, or in-branch without repetition.

- Convenience: Enable self-service, Co-Browsing, and secure Document Collaboration to reduce friction.

- Hybrid engagement layers

- Combine asynchronous (e.g., Secure Messenger) and synchronous (e.g., Live Chat, video banking) channels for flexible customer journeys.

- Adopt conversation orchestration tools that ensure seamless transitions between bots and human advisors.

Action steps

- Invest in collaboration tools: Platforms like Unblu enable secure Co-Browsing and Document Collaboration, turning digital touchpoints into advisory opportunities.

- Implement customer journey Analytics: Use AI to map and refine each step of the user journey, identifying friction points and personalizing outreach.

- Train advisors for digital empathy: Equip frontline staff with skills and tools to replicate the warmth of in-branch service online.

The future of banking in 2025

This year, business leaders in the banking industry should focus on providing superior digital banking experiences. Customer expectations are continuing to evolve and driving customer loyalty is no easy task.

From the actual products to the incorporation of agile technology solutions, the ability of banks to provide agility through technology investments without sacrificing deeper customer engagement (through personalized customer experiences) is paramount.

The banks that will come out on top are those that provide robust digital channels that avoid poor customer experiences and a differentiated product offering. By providing a mix of mobile banking apps, physical branches, and niche products that cater to the entire customer journey, financial sector professionals will be better positioned to drive revenue growth while avoiding bad customer experiences.