.png)

Only 10% of financial services firms have deployed AI agents at scale, even though 80% of them are already running pilots, according to Capgemini's World Cloud Report for Financial Services 2026. That gap between experimenting and shipping is the real story of agentic AI in banking right now.

The bottleneck rarely sits with the model itself. McKinsey estimates that the technology component of an agentic rollout, the agents and the orchestration layer, accounts for no more than 20 to 25 percent of the value a bank can capture. The rest comes from how a bank redesigns its processes, its risk controls, and who supervises what the agent does. Banks that treat an AI agent like a smarter chatbot plug it in and wait for chatbot-sized results. Banks that treat it like a new class of operator, one that needs oversight, escalation paths, and an audit trail, are the ones pulling ahead.

This post looks at what actually separates an AI agent from the rule-based bots banks have run for years, why the industry's adoption curve is outrunning its governance curve, and what today's hybrid, human-in-the-loop model already looks like in production at banks including BPER Banca and PostFinance — the stage the industry is actually at, ahead of full agentic orchestration.

AI agents are a different technology than chatbots, not just a newer one

Banks have used artificial intelligence for years, from rules-based fraud-detection scoring to newer generative tools that draft text on request. Agentic AI is a further step, and it's easiest to see against what came immediately before it: the chatbot. For a decade, "bank chatbot" meant a decision tree: a script matched a customer's wording to a pre-written answer, and anything outside the script escalated to a human. An AI agent works differently. It can plan a sequence of steps, call other systems, and adjust that plan as it gathers information, without a human writing out every branch in advance.

Rule-based bots answer scripts; agents plan and act

The distinction is architectural, not a marketing upgrade. Deloitte frames the shift as one from tools that respond to a single prompt to systems that operate with a measure of autonomy inside a bank's actual workflows. A rule-based bot can tell a customer their balance. An agent can check the balance, cross-reference a pending dispute, draft a resolution, and route it for approval, chaining several steps a scripted bot would need a human to stitch together manually.

That shift also has organisational consequences most banks haven't reckoned with yet. Deloitte's research argues that as agents take on more central roles in day-to-day execution, decision-making authority inside the bank needs to be redrawn alongside them, with rigid hierarchies giving way to flatter structures built for faster information flow between human and AI-driven teams.

Autonomy without oversight is the industry's current risk

Most banks know what agentic AI is; few have deployed it responsibly. EY's Parthenon survey found 99% familiarity with agentic AI among banking respondents, but only 31% have moved past that awareness into actual implementation. The same survey found regulatory compliance and data privacy concerns, cited by 71% and 67% of respondents respectively, as the two barriers banks name most often when explaining why they've stalled.

That hesitation is rational once an agent starts making decisions rather than only answering questions. The distance between "everyone knows what this is" and "few have deployed it responsibly" is where most of the industry's current agentic AI risk sits.

Adoption is outpacing governance across the industry

The pilot-to-production gap isn't unique to any one bank. It shows up across every recent industry survey, and it's widening exactly as regulators start paying closer attention.

Pilots are everywhere; scaled deployment is rare

The industry's own numbers describe a bottleneck, not a technology gap. McKinsey's operations practice has a name for it: pilot purgatory, the pattern of banks running narrow, disconnected AI pilots indefinitely without ever committing to the operating-model changes that scaling actually requires. Customer service tops the list of processes banks are deploying AI agents against at scale, named by 75% of banks in the same Capgemini research cited above, ahead of fraud detection (64%), loan processing (61%), and customer onboarding and know-your-customer checks (59%). That banks are prioritising the highest-visibility, highest-volume workflow first is unsurprising. What's notable is how few have actually escaped pilot purgatory to get there, whichever process they're applying it to.

Regulators are closing the gap fast

The compliance clock is now the more urgent deadline, not the technology roadmap. EY's Global Financial Services Regulatory Outlook 2026 reports that more than 70% of banking firms are using agentic AI to some degree, with 16% fully deployed and 52% still running pilots. That adoption is happening as the EU AI Act's high-risk obligations, covering credit scoring, fraud detection and anti-money-laundering systems, begin taking effect in 2026.

The European Banking Authority's own mapping exercise, published in November 2025, found that the majority of AI use cases at its supervised institutions already fall into the Act's high-risk category. That's not a narrow edge case. It means most banks' existing AI deployments, agentic or otherwise, are already inside the scope of a law with real documentation, oversight, and audit-trail requirements attached to it.

The banks capturing value treat agents as operators, not tools

Every stat above points to the same conclusion: the technology is available, the governance is catching up, and the banks ahead of the curve are the ones that built oversight in from the start rather than retrofitting it.

Human oversight for regulated steps, autonomy for the rest

Hybrid logic, not full autonomy, is what's actually working. McKinsey's research into frontline banking teams found that relationship managers at many commercial banks spend just 25 to 30 percent of their time in direct client dialogue, well below top-quartile institutions, with the rest lost to prospecting, admin, and internal approvals. Agentic AI's clearest near-term value isn't replacing the client conversation; it's absorbing the work around it, so deterministic, rule-based logic handles the regulated, auditable steps while an AI-driven router handles the open-ended parts of a request.

Relationship teams become supervisors, not casualties

The workforce shift is real, but it's a reallocation, not a reduction. Deloitte's research on AI-assisted customer service found that 70% of banking executives surveyed expect AI to shift human agents toward higher-value roles, with 53% expecting agents to need stronger technical or analytical skills as a result. The same pattern shows up in Capgemini's research: a meaningful share of banks and insurers are creating entirely new roles specifically to supervise what their AI agents do, rather than assuming the agents run unattended. Human agents remain accountable for judgment, empathy, and final resolution, exactly the parts of the job an agent can't take over. That's consistent with Unblu's broader guidance on customer service for banks and financial services, which makes the same case: efficiency gains hold only when technology augments an agent's judgment rather than replacing it.

What's live today is assisted automation, and that's the point

Every stat above describes an industry still mostly in pilot. What's actually running in production at scale, at Unblu customers and elsewhere, is the hybrid model this post has been building toward: automation and real-time suggestion layered under a human who makes the final call, not an autonomous agent working unsupervised. That's not a lesser version of agentic AI — it's the stage the whole industry is at, per the 10%-at-scale figure cited earlier.

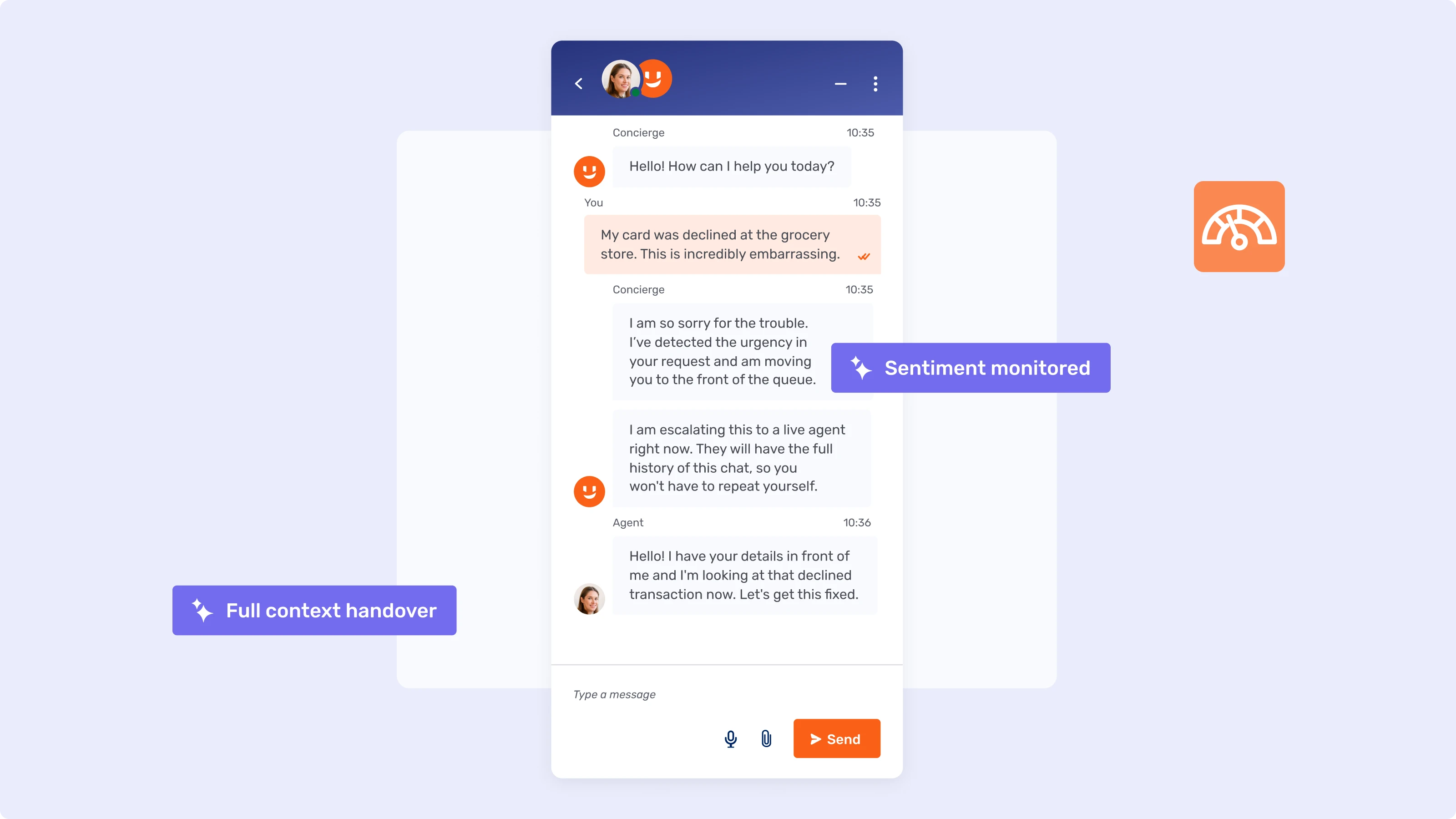

Suggestion Support proves the human-in-the-loop model, not autonomous decision-making

BPER Banca's rollout is a clean example of assistance, not autonomy. After adding Unblu's Suggestion Support to its agent workflow, alongside Live Chat and a Salesforce-integrated agent desk, BPER cut average handle time by 20%. The bank enabled 700 advisors with the tool and a set of bank-approved knowledge documents, meaning the suggestions the system surfaces are grounded in content the bank itself has vetted. Nothing here plans or executes a multi-step task on its own — the system surfaces a suggestion, and the human agent decides whether to accept, edit, or dismiss it. That's the assisted layer of agentic AI, not the orchestration layer.

Automation absorbs volume; a human still owns the judgment calls

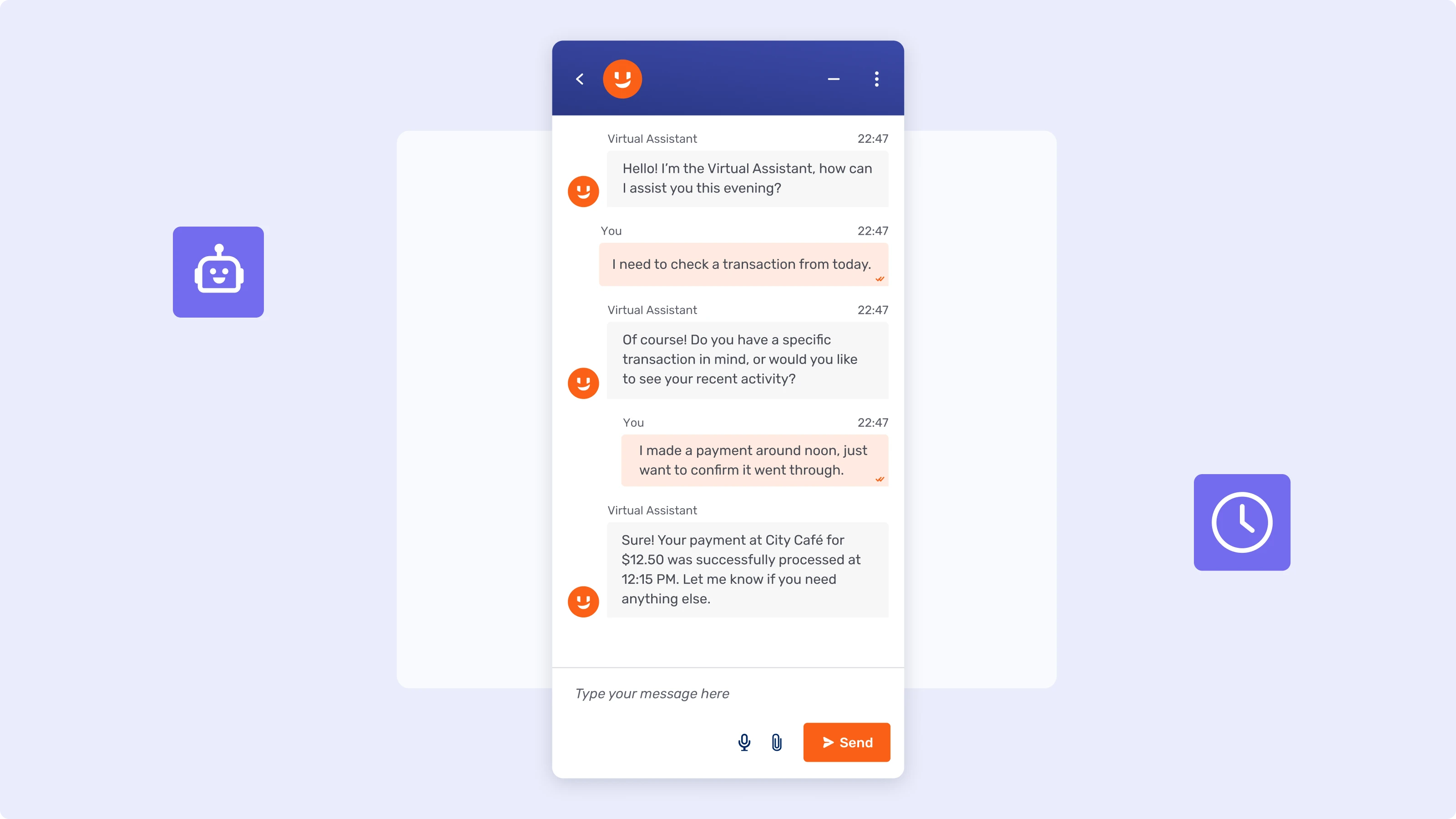

The same pattern shows up at different scales of automation, not autonomy. PostFinance runs a heavier automation load on the customer-facing side: over 1 million bot interactions a year, with 25% of inquiries resolved entirely through written channels, delivering efficiency gains the bank estimates at roughly 40 full-time roles' worth of capacity. UBS runs a chatbot layer that resolves around half of inquiries without agent involvement and escalates the rest with context intact. Both are automation and chatbot deployments in the sense this post defined earlier, not autonomous agents that plan and adapt — and that's exactly consistent with where most of the industry sits today.

Where this goes next

Agentic AI in banking isn't a single leap from chatbot to autonomous agent. It's an incremental handoff of well-defined, lower-risk tasks to a system that can plan and act, while regulated, high-stakes decisions stay behind a human sign-off. The deployments above show the hybrid stage of that journey; the fully agentic orchestration layer, matching an intent-based router to autonomous multi-step actions, is newer across the industry, and production case studies for it are still emerging. The banks pulling ahead in 2026 aren't necessarily the ones with the most sophisticated model. They're the ones that can prove, to a regulator and to their own risk committee, exactly what their system did and why.

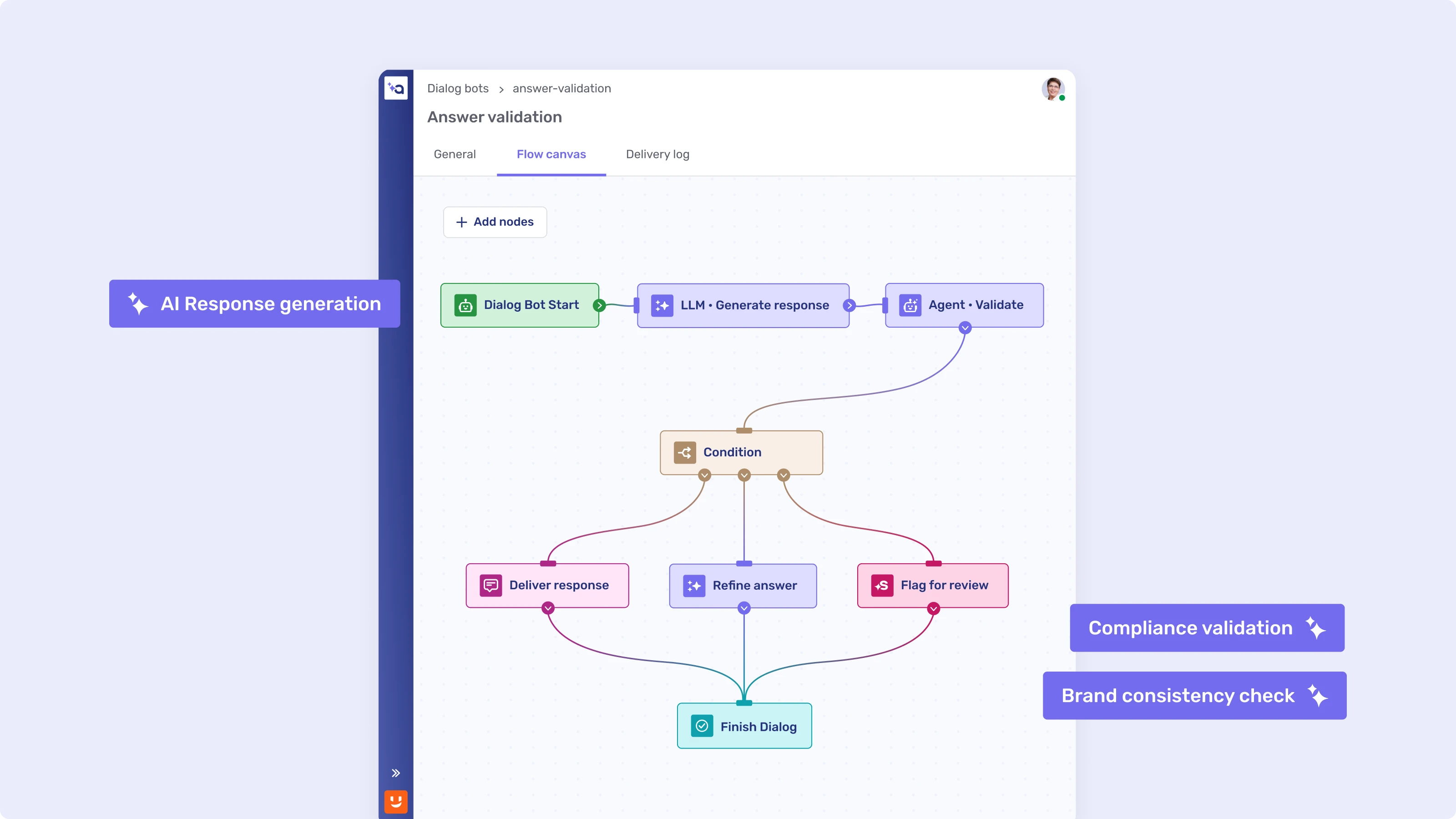

Unblu Aria is designed for exactly this hybrid stage. Its orchestration layer pairs deterministic, rule-based flows for regulated steps with an LLM-driven router for open-ended requests, while Suggestion Support keeps a human agent in the loop with the same context an autonomous system would use, deployable against Unblu-managed Azure infrastructure or a bank's own LLM keys, including on-premise models, where data control has to stay in-house.

Want to see how Aria's hybrid logic fits your compliance requirements? Book a demo.