.png)

Nearly two in three bank customers who reached a human agent did so because a chatbot had already failed them. Capgemini's World Retail Banking Report put that figure at 61%, with a further 17% who distrusted the chatbot and asked for a person from the outset. The technology meant to reduce contact volume was quietly generating it.

That is the paradox at the centre of AI in banking customer service. Banks have already deployed it. The open question is whether they deployed it in a way customers trust, and increasingly, in a way regulators accept. Consumer comfort with AI has climbed fast, but it stops at the point of judgment: TD Bank's 2026 AI Insights Report found 78% of people now use AI tools in daily life, yet only 18% would trust AI to make a financial recommendation on its own.

Three things decide which side of that line a bank lands on. The regulator has just made one of them mandatory.

Most AI in banking customer service still deflects without resolving

The problem is rarely AI itself. It is the first generation of it: rigid, rule-bound chatbots deployed to cut cost, with no credible route back to a human when they stall.

A bot that cannot resolve the query only moves the frustration

A chatbot that fails to resolve an issue does not remove a contact; it delays it, and irritates the customer twice on the way. Capgemini's research found more than 60% of customers rated their chatbot experience as no better than average, and that call abandonment had climbed to 12% at tier-one banks and close to 18% at tier-two banks. When the automated layer cannot close the loop, the work returns to the contact centre anyway, now carrying an annoyed customer. The cost was not saved. It was deferred and inflated.

The lesson from that first wave is specific. Deflection is only valuable when it comes with resolution. A containment rate that looks good on a dashboard means nothing if a third of those "contained" conversations resurface as angry calls.

Customers arrive with higher expectations, not lower ones

AI literacy has risen sharply, and with it the expectation that a bank's AI will actually work. A year ago, roughly one in ten consumers used AI to help manage their money. By 2026 that had reached 55%, according to the TD survey reported by Banking Dive. People now measure their bank's assistant against the consumer tools they use every day, and the bar is far higher than it was for a 2021-era decision-tree bot.

Comfort is not the same as trust. The same research shows people will happily let AI draft, summarise, and suggest while reserving the actual financial decision for a human. A service strategy that ignores that distinction, and pushes automation into the moments customers want a person, erodes the relationship it was meant to strengthen.

AI earns its keep in the contact centre when it is scoped to the routine

Scoped correctly, the return is real and large. McKinsey estimates generative AI could add between 200 and 340 billion dollars a year to the global banking sector, most of it from productivity, and customer operations is one of the four functions where the bulk of that value sits.

The clearest wins are in the repetitive, not the complex

AI's strongest return in banking service is absorbing high-volume, low-complexity contacts so human agents are freed for the interactions that need them. McKinsey's 2026 analysis of bank customer care found that 75% of the most common reasons customers call had no self-service option at all: a vast pool of routine, automatable demand sitting on top of agents who should be handling complex cases.

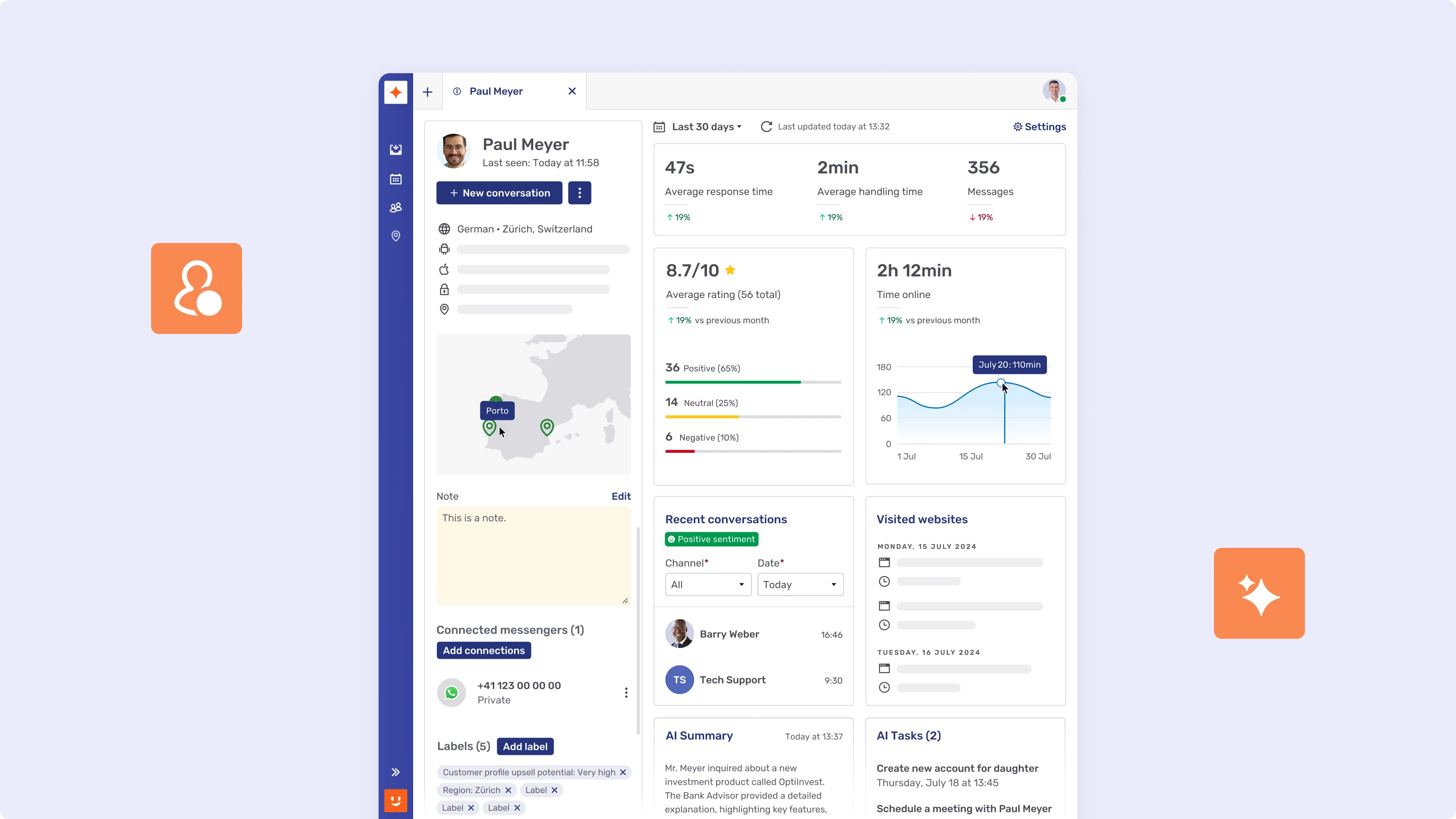

PostFinance shows the pattern in production. Switzerland's PostFinance handles more than a million bot interactions a year against roughly 240,000 conversations that reach an agent, with a quarter of all inquiries now resolved through written channels, and it has freed capacity equivalent to around 40 full-time roles through automation across its channels. The automation is not there to remove the human. It is there to make sure the human is spent on the conversations that justify one.

Augmenting the agent beats replacing the agent

The higher-value use of AI in banking service is making the human faster and sharper, not engineering the human out. Capgemini's 2025 contact-centre work found only 16% of agents satisfied in their roles, and argued the winning move is AI that augments them: surfacing the right knowledge, reading sentiment, and drafting responses so the person can focus on empathy and judgment. Capgemini frames this as the bridge between human warmth and machine efficiency.

The numbers from banks doing this are concrete. BPER Banca cut its average handle time by 20% after putting AI-assisted suggestions into the workflow of around 700 agents. On the customer-facing side, UBS reports that about half of its inquiries are now handled by a chatbot with no agent involvement, and that customer satisfaction over live chat runs 1.4 points higher than over email. In both cases the AI carries the load it is good at and hands over cleanly when it is not.

Customer trust in AI service is designed in, not discovered

Trust in an AI service layer is not a by-product. It is designed in, or it is absent. Three choices decide it.

Escalation has to be real, not a dead end

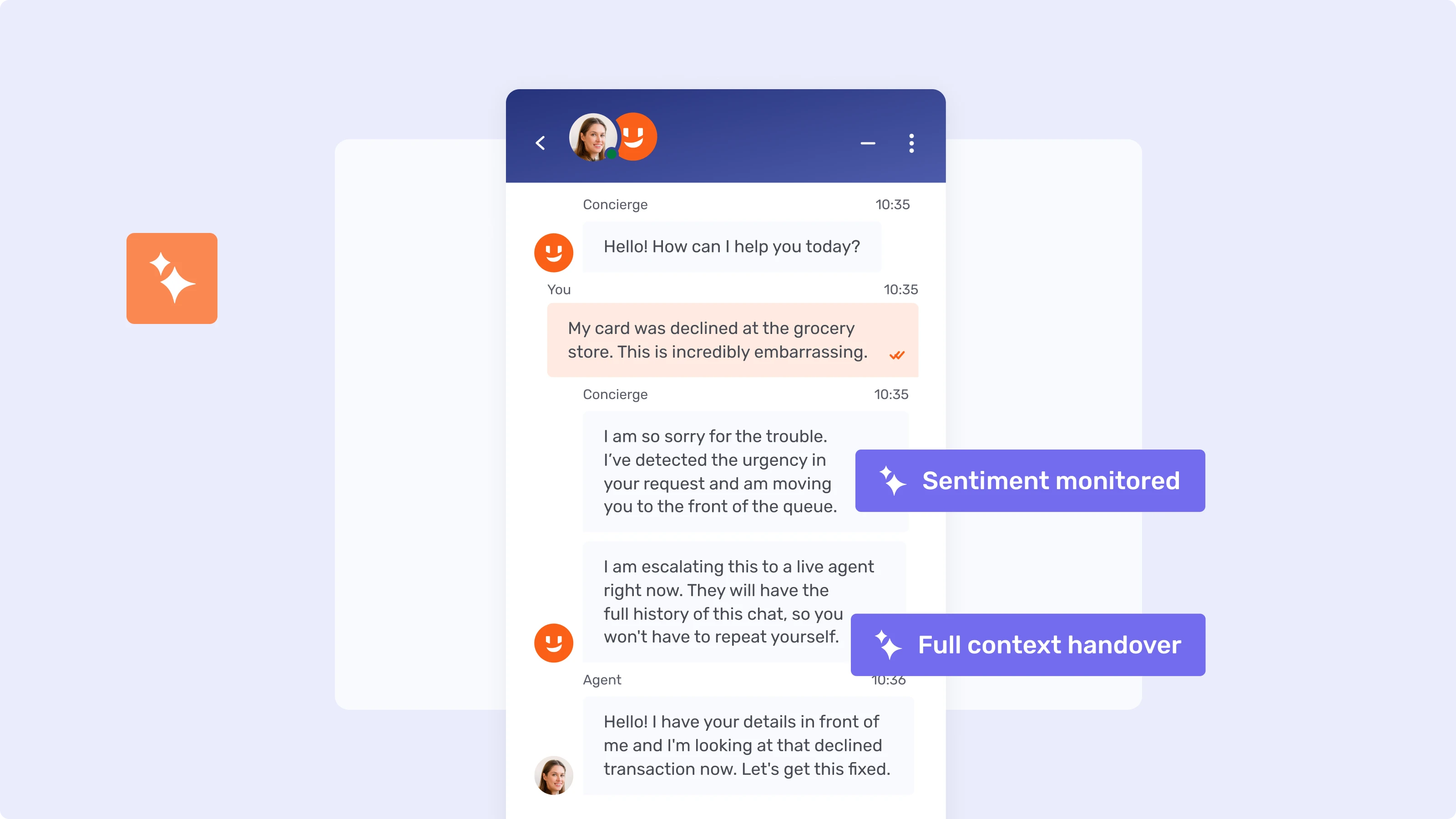

The single largest trust factor is whether a customer can reach a person the instant the AI hits its limit. The 61% who contacted an agent out of chatbot frustration were not rejecting automation in principle; they were reacting to automation with no exit. A handover that carries the full context of the conversation, so the customer never has to repeat themselves, turns a failure point into a save. A handover that drops the customer into a queue with a blank slate confirms every suspicion they had about the bot. The difference is architectural: escalation only works when the AI layer and the human channels are the same system, not two products stitched together after the fact.

The bank has to be able to show what its AI did

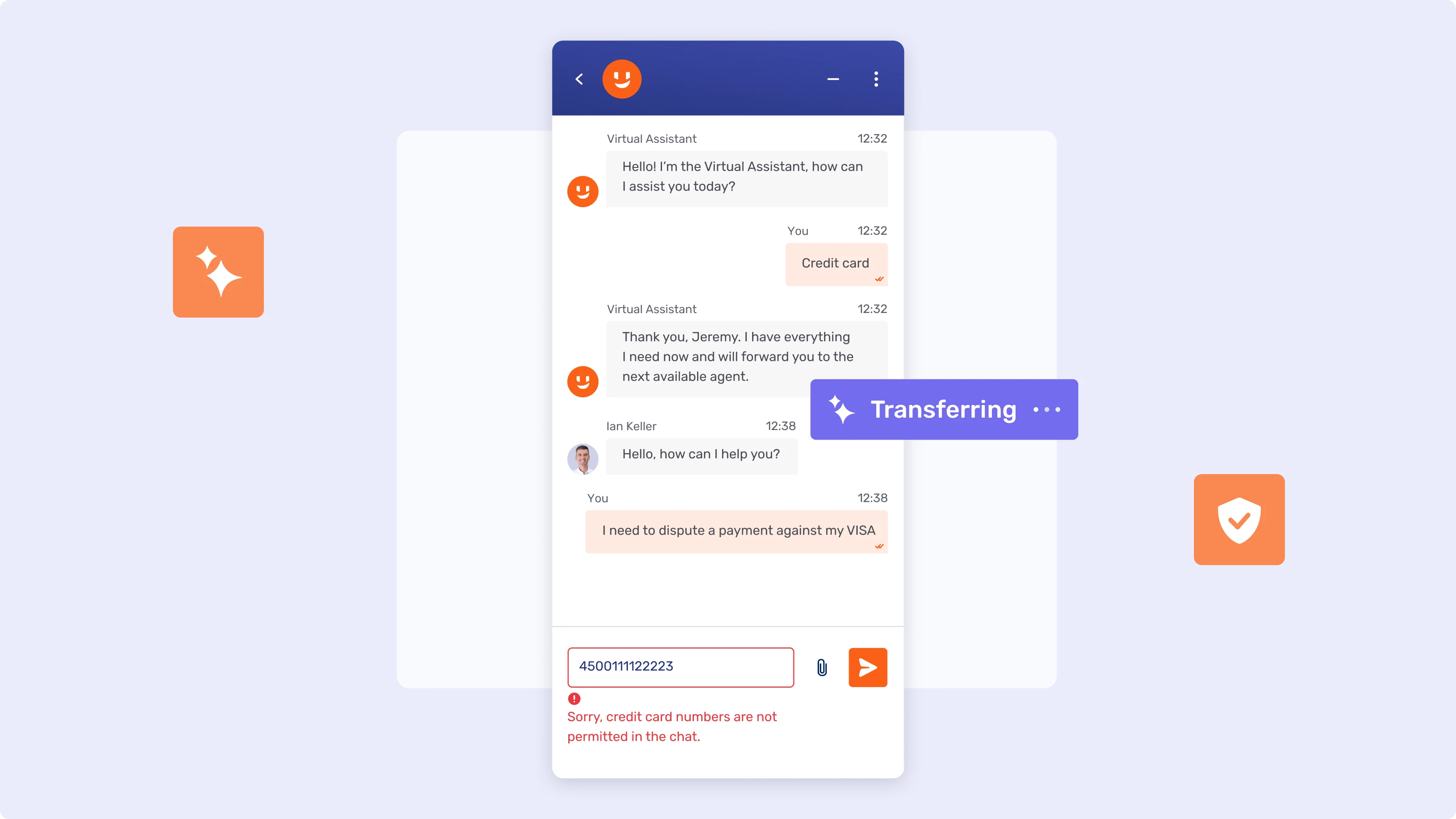

Trustworthy AI in banking service leaves an auditable trail of every automated decision and message. In a regulated industry, "the model handled it" is not an acceptable answer when a customer disputes an outcome. Every automated interaction needs to be logged, retrievable, and explainable after the fact, on the same footing as a recorded call or an archived email. This is where many 2024-era deployments are now exposed: they were tuned for a smooth demo, not for the audit that follows a disputed decision.

Where the data is processed is a trust question, not just an IT one

The location and governance of the data a bank's AI touches shape both its compliance posture and its customers' confidence. Service conversations carry account details, identity data, and financial circumstances. Banks that cannot say precisely where that data is processed, which model saw it, and whether it was used for training will struggle to satisfy either their own risk function or a customer who asks. Control over the data path is fast becoming a precondition for deploying AI in service at all.

Set side by side, the two generations of AI service look less like a difference in technology and more like a difference in design intent:

The EU AI Act now sets the floor for customer-facing AI

As of 2026 this stopped being a strategic choice and became a compliance obligation, and most banks are not ready: Capgemini found only 6% of retail banks had an enterprise-wide roadmap for AI at scale.

Customer-facing AI has to disclose that it is AI

From 2 August 2026, a bank's customer-facing AI must tell customers they are interacting with a machine, not a person. Under the transparency rules of the EU AI Act, conversational systems that interact with people carry a specific disclosure obligation, as legal analysts tracking the Act's application to financial services have set out. The requirement reaches any bank serving customers in the EU, wherever the bank itself is based. Disclosing the agent is operationally simple. The harder part is what disclosure invites: once a customer knows they dealt with AI, scrutiny lands on whether the bank can explain what that AI did.

The moment AI touches an eligibility decision, the bar rises sharply

A service assistant that strays into creditworthiness or eligibility stops being a low-risk chatbot and becomes a high-risk system. The Act treats AI used to assess a person's creditworthiness as high-risk, which brings obligations around risk management, data governance, logging, transparency, and mandatory human oversight. A customer-service bot that answers "am I eligible for this loan?" can cross that line without anyone intending it to. These obligations sit alongside DORA, GDPR, and MiFID II rather than replacing them, so the compliance load compounds rather than consolidates.

Compliance is far cheaper designed in than bolted on

The banks ready for the deadline are the ones that treated auditability and oversight as design constraints from the start, not as a final gate to clear. McKinsey makes exactly this point about bank AI: value is unlocked when risk and compliance are built in as design constraints rather than presented to legal only at the point of scaling. Retrofitting logging, human-in-the-loop controls, and data governance onto a chatbot that was never built for them is the expensive path, and it is the one many early deployments are now walking.

The winners automate the right contacts, not the most

AI in banking customer service has moved past the question of whether to adopt it. Banks already have. The live question is design: whether the automation resolves or merely deflects, whether it hands over to a human cleanly, whether every automated decision can be explained, and whether the whole thing meets a regulatory bar that took effect in 2026. The banks getting real value are not the ones automating the most. They are the ones automating the right contacts and making their human service better with the time that frees up.

That points to a specific kind of platform: one where the AI layer and the human channels are the same system, so escalation carries context, oversight is native, and every interaction is on the record.

Unblu is built for that. Unblu Aria is the layer that orchestrates these flows: its AI virtual agent handles the routine, high-volume customer-facing contacts, while the Unblu Workbench equips human agents with real-time Suggestion Support and summaries for the conversations that need a person. Unblu Spark keeps Live Chat, Secure Messenger, and Video & Voice in the same compliant layer, with human handover and a full audit trail of every interaction. It runs on Unblu Cloud, a Swiss sovereign cloud, or fully on-premise, with the choice of an Unblu-managed or bank-managed model, so the data path stays under the bank's control.