.png)

The arrival moment is the part of the branch experience most banks haven't re-engineered – and it's quietly undermining everything else.

Banks have spent heavily on the digital transformation of branch networks. They have digitized advisory workflows, restructured physical layouts to favor client meetings over teller queues, and built hybrid operating models that let a single advisor serve multiple locations. Yet productivity in the banking sector has declined at an average annual rate of 0.3% since 2010, despite this sustained investment. Something is not adding up.

Part of the answer sits at the branch entrance – the first 60 seconds after a client walks through the door.

Why branch digital transformation rarely reaches the front door

Banks have made a strong case for maintaining physical presence alongside digital channels. Two-thirds of consumers still value having a branch in their neighborhood as a sign of stability and availability, and over 40% maintain that in-person interaction remains essential to their banking experience, particularly for complex financial matters.

Mobile banking handles the routine; the branch handles what requires a human. But many digital transformation programs stop short of the most visible point of friction in that branch customer journey: arrival. For banks that have already invested in hybrid branch operating models, this gap is especially visible.

And, thankfully, solvable.

The productivity paradox in physical banking

Branch digital transformation has largely focused on what happens after a client is seated, not on what happens when they walk in.

McKinsey’s research on branch modernization identifies physical locations that are “old, under-occupied, and poorly maintained” as the primary driver of customer dissatisfaction – pointing to a pattern where digital tools and advisory infrastructure receive investment while the entry experience is left unchanged. The result is a mismatch: banks with sophisticated remote advisory capabilities, but an arrival process that still depends entirely on a staff member manually determining why each client has come.

Bold digital transformation of branch networks has been shown to deliver four times higher productivity gains than incremental adjustments. The gap between retail banking institutions that have genuinely re-engineered operations and those that have layered digital tools onto old processes is widening. And arrival management is one area where that gap is most visible.

The arrival moment as an organizational blind spot

Most banks have no systematic way to distinguish, at the point of entry, between a client who needs guidance and one who simply needs to confirm their 2pm appointment.

This is not a failure of intent – it is a structural gap.

Branch reception staff handle every arrival the same way: a greeting, a question about the purpose of the visit, and a manual routing decision. For a client arriving for a pre-booked advisory meeting, this interaction adds nothing. For the advisor waiting, it creates an unpredictable lag. For the digital reception, it means inbound volume that has nothing to do with the customer experience it is designed to deliver.

The European Central Bank recorded a fall in euro area bank branches from 186,000 in 2008 to just 106,000 in 2023 – a reduction of more than 40% in 15 years. The retail banking institutions that have kept branches open have done so by making them more efficient. But operational efficiency at the front door has received far less attention than efficiency in the back office or the advisory room.

What the arrival moment is actually costing

The cost of poor arrival management rarely appears as a line item, which is precisely why it persists. It surfaces in three ways: as advisor time absorbed by logistics, as digital reception capacity consumed by routine routing, and as a customer experience that sets the wrong tone before a meeting has started.

The hidden tax on advisor capacity

Every appointment that requires manual check-in is a small inefficiency, but at branch network scale, those minutes accumulate into a measurable drag on advisor productivity.

When a client arrives for a scheduled advisory session, the ideal outcome is simple: they are confirmed, their advisor is notified, and the meeting begins. In most branches today, this sequence requires at least one human intervention – a staff member recognizing the client, checking a system, and sending a notification through whatever channel the advisor happens to be monitoring. In branches running lean, that same staff member is also managing walk-in inquiries and covering the desk.

Research from The Financial Brand and Candescent notes that reception staff are often “the lowest-paid employees managing the highest-regulated interfaces” in the branch. This is a structural position that makes capability development difficult when the role is still absorbing routine logistics.

The advisor capacity question and the reception logistics question are connected: you cannot fully release an advisor to focus on high-value work if the system that announces a client’s arrival depends on someone manually managing the front desk. This is the gap in the customer journey that bank branch automation programs consistently overlook.

Queue dynamics and customer satisfaction

A branch where walk-in clients and appointment clients compete for the same reception resource will always feel busier than it is. The result is a perception that undermines customer satisfaction before the interaction has begun.

Queue dynamics research consistently shows that perceived wait time is disproportionately shaped by the first two to three minutes of an experience. A client who checks in instantly via a queue management system and is told their advisor has been notified experiences a wait very differently from one standing in an informal queue. The underlying wait may be identical; the customer satisfaction impact is not.

RBR Data Services’ 2024 Global Branch Transformation Report noted that the US alone had approximately 97,000 bank branches as of end-2023. Across networks of that scale, even modest improvements in arrival handling per visit translate into a significant aggregate shift in customer experience, and in how effectively staff capacity is used across the customer journey.

What intelligent arrival management looks like in practice

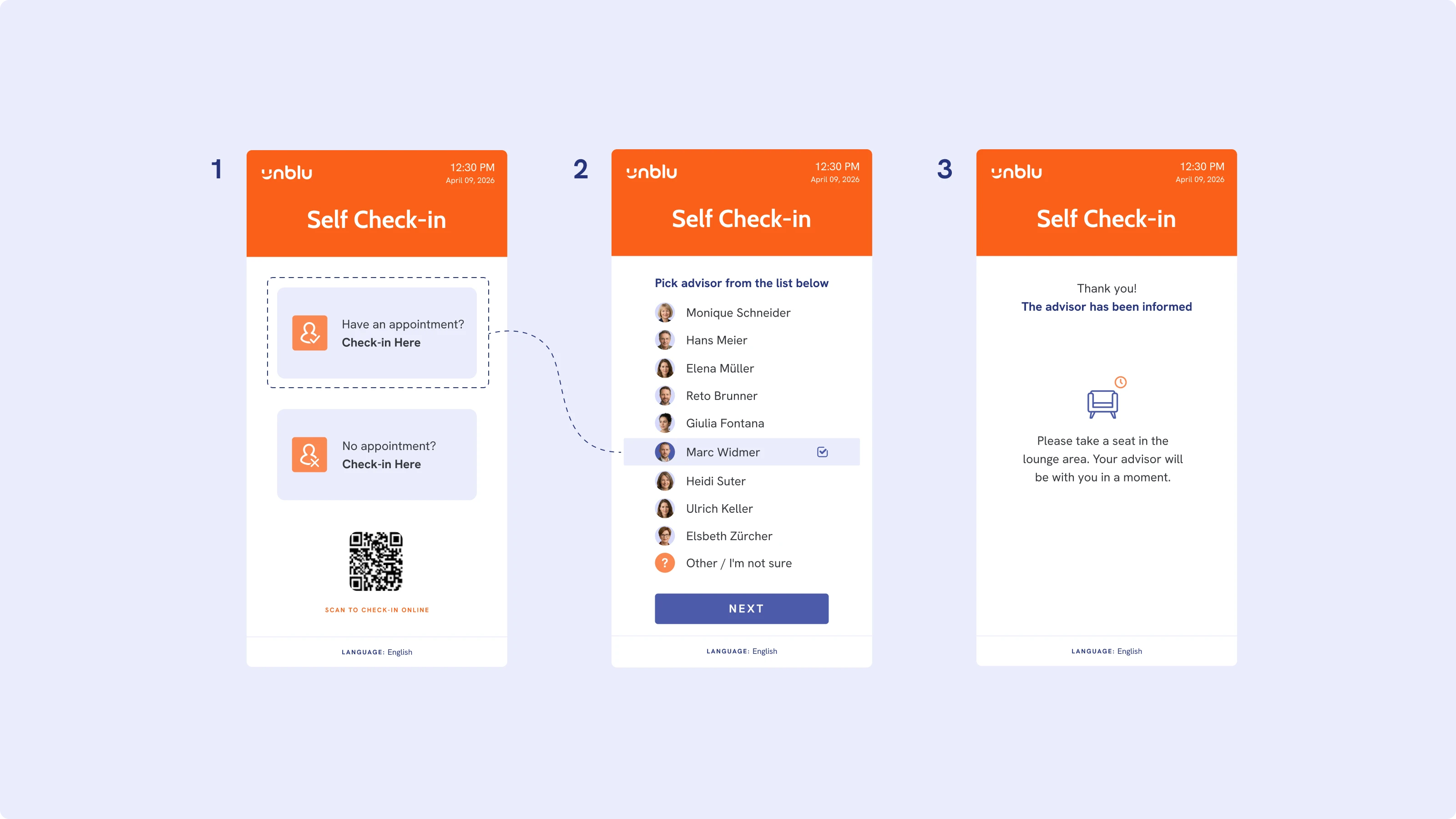

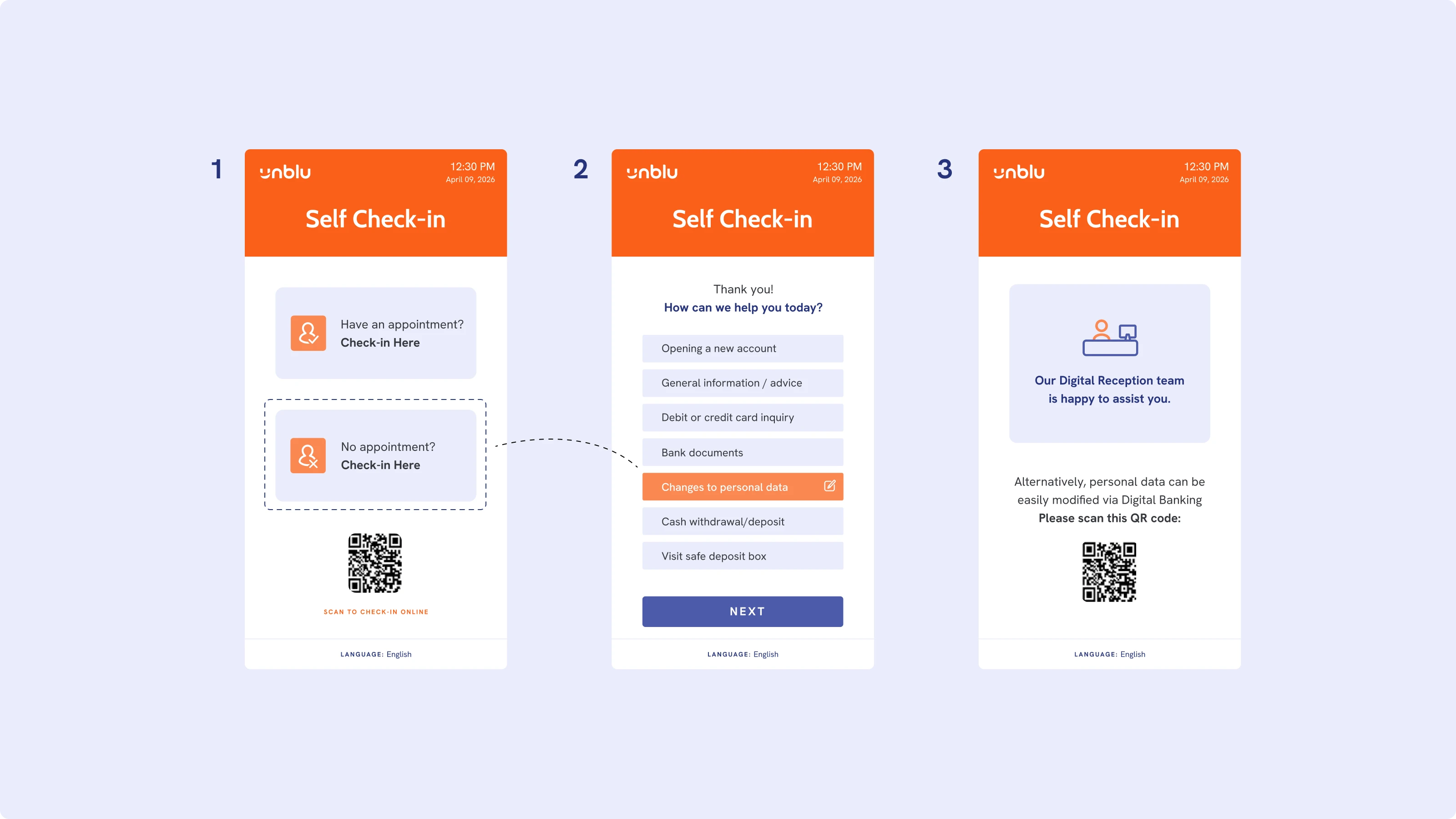

There is a straightforward operational principle at the center of this argument. This is that every arrival requires the same response. A client who has a confirmed appointment at a known time with a named advisor needs confirmation, not consultation. A walk-in client with an unspecified need requires triage, not a queue number.

The two demand different handling, but most bank branches treat them identically.

Separating the routine from the complex at the door

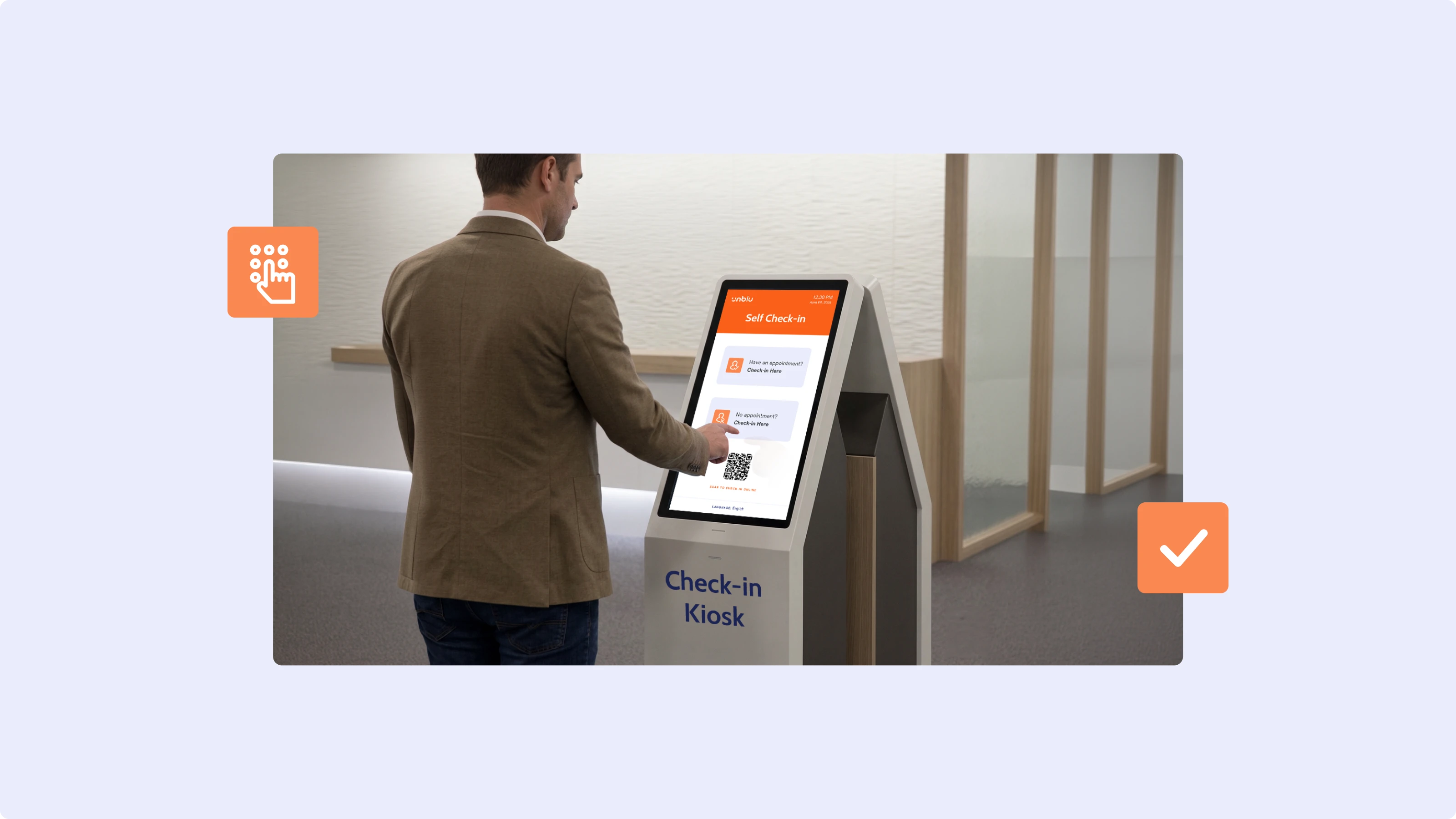

A self-service check-in layer at the branch entrance handles the confirmations and basic triage that currently absorb staff time, routing clients to the right resource without human intervention.

For clients with existing appointments, this means a simple sequence: identify, confirm, notify. The advisor receives an alert through the digital tools already in use – whether that is a collaboration tool like Microsoft Teams or the branch management platform – and the client is directed to the waiting area or meeting room. The reception desk is never involved.

For walk-in clients, the same entry point handles an initial triage: what brings you in, what kind of help do you need, where should you be directed?

Artificial intelligence can support the routing logic at this layer – surfacing the right service path based on client input – without replacing human judgment on genuinely complex inquiries. The check-in layer is a filter, not a gatekeeper.

How this changes what the digital reception actually handles

When arrival logistics are handled at the door, the digital reception is freed to deliver the customer experience it was designed for, as the first point of meaningful human contact for clients who need assistance.

The hybrid branch model – where a remote advisor in contact centers manages the branch entry experience via video – has demonstrated significant operational advantages for retail banking networks. Valiant Bank’s deployment of this model resulted in one advisor serving up to seven branch locations, with clients connected to support within one minute of arrival. These are meaningful gains across the customer journey. But they depend on the digital reception handling the right mix of interactions.

When the digital reception is absorbing appointment confirmations and basic walk-in sorting alongside genuine advisory conversations, two things happen: average handling time increases, and the ratio of meaningful to routine interactions falls. A check-in layer at the entrance resolves both – not by replacing the digital reception, but by giving it a cleaner, more purposeful workload and a better customer experience from the first touchpoint.

How leading banks are rethinking the physical entry point

The broader branch digital transformation trend is well established. Bank of America is investing in 165 new redesigned locations by 2026, moving away from traditional teller lines toward collaborative advisory spaces. Citizens Bank is rightsizing branches into smaller, more focused environments.

In both cases, the logic is the same: branches should exist for the customer journey interactions that benefit from being in person, which means clearing the path to those interactions as efficiently as possible.

The Valiant Bank model and what it demonstrates

Valiant Bank’s branch digital transformation offers a useful reference point – not as a blueprint to copy, but as evidence that re-engineering every stage of the customer journey through a branch produces outcomes that incremental investment cannot.

Valiant, a Swiss retail banking institution for private individuals and SMEs, faced a significant structural problem: a 35% reduction in personal assisted transactions and over half of its branches open for just three hours a day. Rather than manage a slow decline, the bank rebuilt its model around a hybrid operating structure, connecting branch locations to contact centers and significantly reducing setup costs.

The results are documented in Valiant’s case study: new branches opened in three additional regions, opening hours extended to an average of ten hours per day, and advisor capacity redistributed across locations rather than tied to any single branch. The model demonstrates that when every element of the branch operating structure is examined – the advisory room, the digital tools, the routing, the notification flows, and the entry point – the efficiency gains compound.

Extending the operating model, not building a new one

The most durable branch efficiency gains come from completing the digital transformation logic already in motion, not from adding standalone systems to an already complex stack.

Banks that have invested in hybrid branch infrastructure already have the components in place: branch management dashboards, remote advisor workflows in contact centers, notification integrations, digital tools for document collaboration. A check-in use case connects to these components rather than replacing them.

An arrival interaction that triggers a notification to the waiting advisor, routes a walk-in client to the digital reception queue, or supports an omnichannel experience across the customer journey is not a separate product. To put it simply, it is the existing operating model extended to the one moment that most digital transformation programs have left unaddressed.

Artificial intelligence makes this layer increasingly capable over time: routing logic improves with use, wait-time transparency becomes more accurate, and the system learns which arrival patterns correlate with specific advisory needs. The entry point becomes less of a logistics bottleneck and more of a genuine first step in the customer journey.

Research from Candescent shows that while 40% of consumers still value in-person interaction for complex financial matters – opting for the branch over digital channels when decisions carry real weight – the nature of those interactions is shifting toward advice, planning, and relationship management. Banks that align their arrival management to this reality are better positioned to demonstrate the value of their physical network to clients and shareholders alike.

The digital transformation gap that’s still open

Branch efficiency programs tend to measure what happens inside the meeting room: advisor utilization, conversion rates, customer satisfaction scores. These matter. But the digital experience starts before the meeting room – at the moment a client walks through the door and has to wait while reception staff finish with someone else.

The argument for addressing the arrival moment is not primarily about cost reduction, though the cost case is real. It is about coherence. Banks that have invested in sophisticated advisory operations, hybrid networks, and digital transformation across their contact centers deserve a front door that matches. The digital tools to build that front door – as a use case on an existing branch platform – are available today, and the operational logic is straightforward.

Unblu Branch provides the underlying platform: Digital Reception, remote advisor workflows, branch management infrastructure, and the integrations on which intelligent check-in use cases can be built. Available on cloud, Swiss sovereign cloud, or on-premise.