.png)

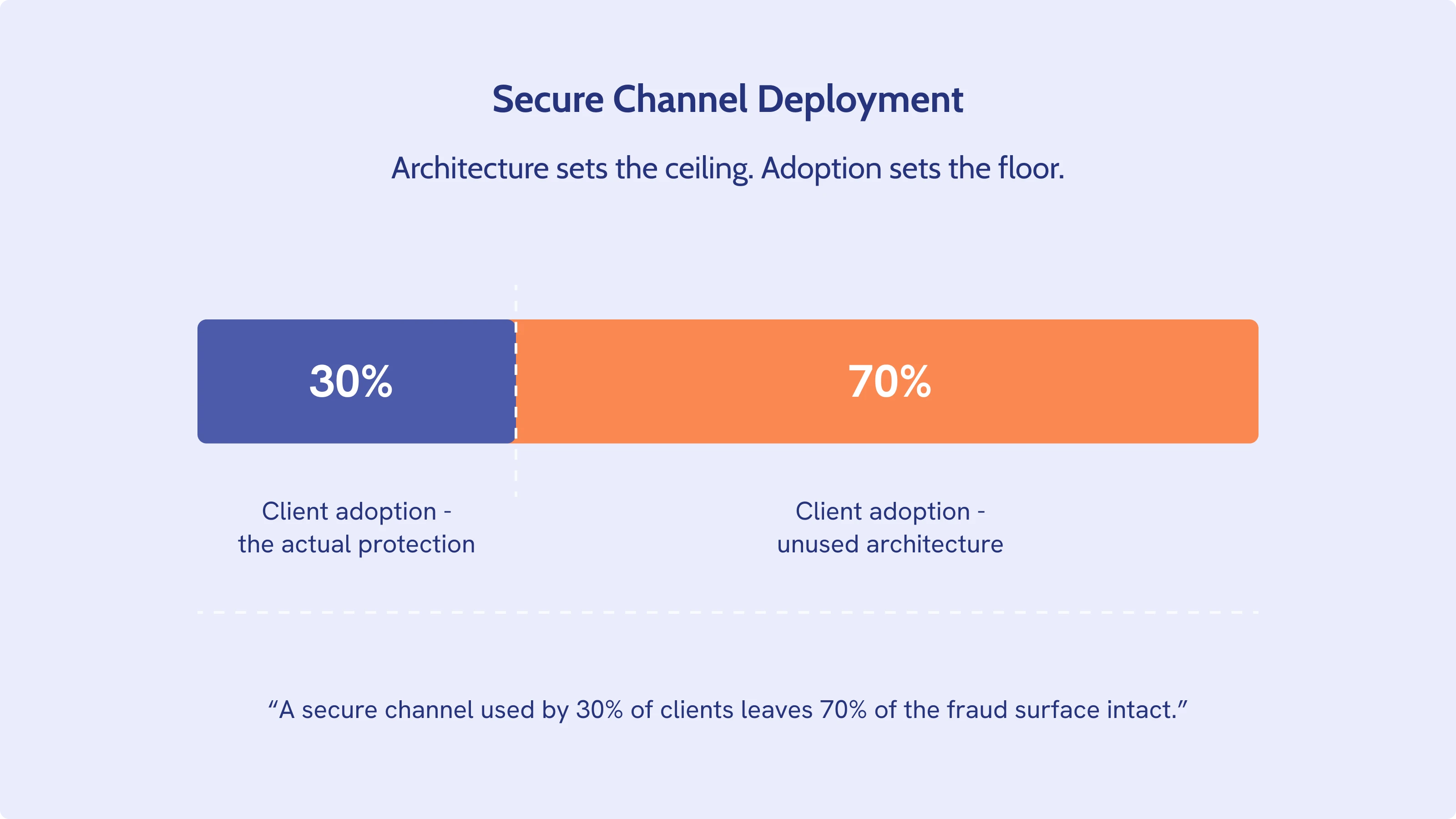

AI-cloned voices, deepfake video calls, and channel-spoofed payment scams now sit inside the wealth advisor relationship itself. A secure channel used by 30% of clients leaves 70% of the fraud surface intact – here's what closes the gap.

Deloitte's Center for Financial Services projects that generative-AI-enabled fraud losses in the United States will reach $40 billion by 2027, up from $12.3 billion in 2023. When you crunch the numbers, it represents a 32% compound annual growth rate driven by deepfake voice, AI-generated email, and synthetic identity attacks.

This is the new Artificial Intelligence fraud risk profile that wealth firms now face. The 15th EY and IIF Global Bank Risk Management Survey reports financial crime has jumped to 43% on the bank-risk agenda, up from 23% a year earlier, with digital fraud climbing to 59% from 23%.

For wealth advisory firms, those numbers land in a specific place: client communication. Phishing emails, spoofed advisor calls, AI-cloned voicemails, and WhatsApp messages from "your relationship manager" all share the same architecture problem. The client has no way to verify who is on the other end of the channel.

Architecture defines what is possible. Adoption converts capability into protection. A secure channel used by 30% of clients still leaves 70% of the fraud surface intact, which is why the question for wealth firms in 2026 isn't whether to deploy a compliant communication stack – it's how to make it the default channel for the relationship.

Why is the wealth-client fraud surface expanding so quickly?

Three forces have reshaped the wealth-advisor fraud risk surface in the last 24 months: cheap AI impersonation, redrawn regulatory liability, and the residual fallout from off-channel communications enforcement. Each is consequential alone. Together they are rewriting what "secure client communication" has to mean for any firm holding wealth on a private banking or wealth advisory balance sheet.

AI has collapsed the cost of impersonation

Synthetic voice and video can now be generated from a few seconds of public audio, and the financial sector is the primary target.

In February 2024, an Arup finance employee in Hong Kong transferred $25 million after a video conference in which every participant – including the CFO – was AI-generated. Average losses from individual deepfake fraud incidents now exceed $500,000, and in the US alone, deepfake-related fraud losses reached $1.1 billion in 2025, triple the previous year.

For wealth clients, the threat profile is sharper than retail banking. A private bank's client roster is a curated list of HNWIs and ultra-HNWIs, each with a social media footprint, conference appearances, and podcast clips that supply the raw audio for voice cloning.

Deepfake technology has reshaped identity theft for wealth clients in particular: a fraudster who clones the voice of an advisor or a client's family member can authorize a transaction or extract identifying information without ever needing to compromise a credential. Fraudsters no longer need scale; they need a target list, and that list is increasingly easy to assemble.

Regulators are redrawing the liability map

Fraud risk allocation has shifted aggressively on both sides of the Atlantic, raising the cost of failing to prevent client-side fraud.

The UK Payment Systems Regulator brought authorized push payment reimbursement into force on 7 October 2024, splitting liability for scam losses 50:50 between sending and receiving banks for the first time, with an £85,000 maximum claim. The FCA has paired the rules with its Consumer Duty regime, signalling that firms with "inadequate systems to detect and prevent scams" will breach the Duty even where the customer authorized the payment.

In the European Union, the Digital Operational Resilience Act entered application on 17 January 2025, harmonizing operational resilience rules across roughly 22,000 financial entities – including ICT third-party providers. For wealth advisory firms operating across the EU, the implication is that operational, cyber, and fraud risk are now scrutinized under one regime, with the management body held directly accountable.

Off-channel communications enforcement is now a permanent feature

Since 2021, the SEC and FINRA have collected more than $2.2 billion in fines from over 100 firms for failing to capture business communications conducted on personal phones and consumer messaging apps.

The 2024 wave alone added more than $600 million in penalties, with another $63 million in January 2025. The enforcement direction is clear: every business conversation has to be captured inside an audited channel, regardless of which app the advisor or client opens to start it. Firms that have leaned on policy bans rather than infrastructure now face a difficult choice – enforce a ban that clients increasingly resent, or replace the unrecorded channel with one that captures the conversation by design.

Off-channel enforcement also surfaces the insider threat dimension supervisory teams now have to take seriously. When advisor conversations live outside the firm's audit perimeter, the firm loses visibility into deliberate misconduct as well as inadvertent leaks – unrecorded calls used to steer clients toward off-platform investment fraud, fee arrangements no compliance officer sees, or disclosure breaches that only surface in regulatory subpoenas.

Where does the fraud surface actually live?

Wealth advisory fraud isn't primarily a payment-rails problem or an authentication problem. It is a channel problem. The point at which a client decides "this is my bank" or "this is my advisor" is the point at which the fraud surface either narrows or expands.

The channel of contact is the vulnerability

Consumer messaging apps, email, and unverified phone calls share one structural weakness – the client has no way to verify that the entity on the other end is actually the bank.

WhatsApp messages can be sent from any phone number, including spoofed numbers. Emails arrive from lookalike domains. Phone calls come from caller-ID-spoofed lines and are answered by AI-cloned voices. None of these channels carries a cryptographic guarantee that the sender is who they claim to be. A request from "the relationship manager" – to verify a transaction, click a link, or join a Zoom call – looks identical whether it's from the real advisor or a fraudster who scraped LinkedIn the night before.

The most damaging fraud category for HNW clients in 2026 isn't direct credential phishing but channel impersonation. The fraudster doesn't try to steal a password. They impersonate the advisor in a channel the client trusts. This is the substrate for both business email compromise – where fraudsters intercept or spoof email threads to redirect payments – and the broader category of social engineering attacks that target the moment of decision rather than the security perimeter.

Authentication is the first line, not the last

Where the channel originates determines whether fraud has somewhere to enter.

If a client opens their bank's app, authenticates with the bank's own SSO or strong customer authentication, and only then enters a messaging or video conversation, the channel itself is verified. The fraudster cannot reach the client through that path without first compromising the bank's authentication system. If the client opens WhatsApp instead, the channel is unauthenticated by default, and the only verification available is whatever heuristic the client applies to a phone number and a profile photo.

The distinction matters because it determines where defence is even possible. Detection-based fraud controls – monitoring for unusual transaction patterns, flagging suspicious payment beneficiaries – sit at the back end. Architectural fraud controls sit at the front end, before the fraudster has any vector to reach the client.

What does architecturally fraud-resistant communication look like?

The architecture that closes the channel-impersonation surface is straightforward to specify and increasingly straightforward to deploy. Three components do most of the work: an authenticated messaging channel, voice and video that can't be spoofed, and visual co-presence on the screens where money actually moves.

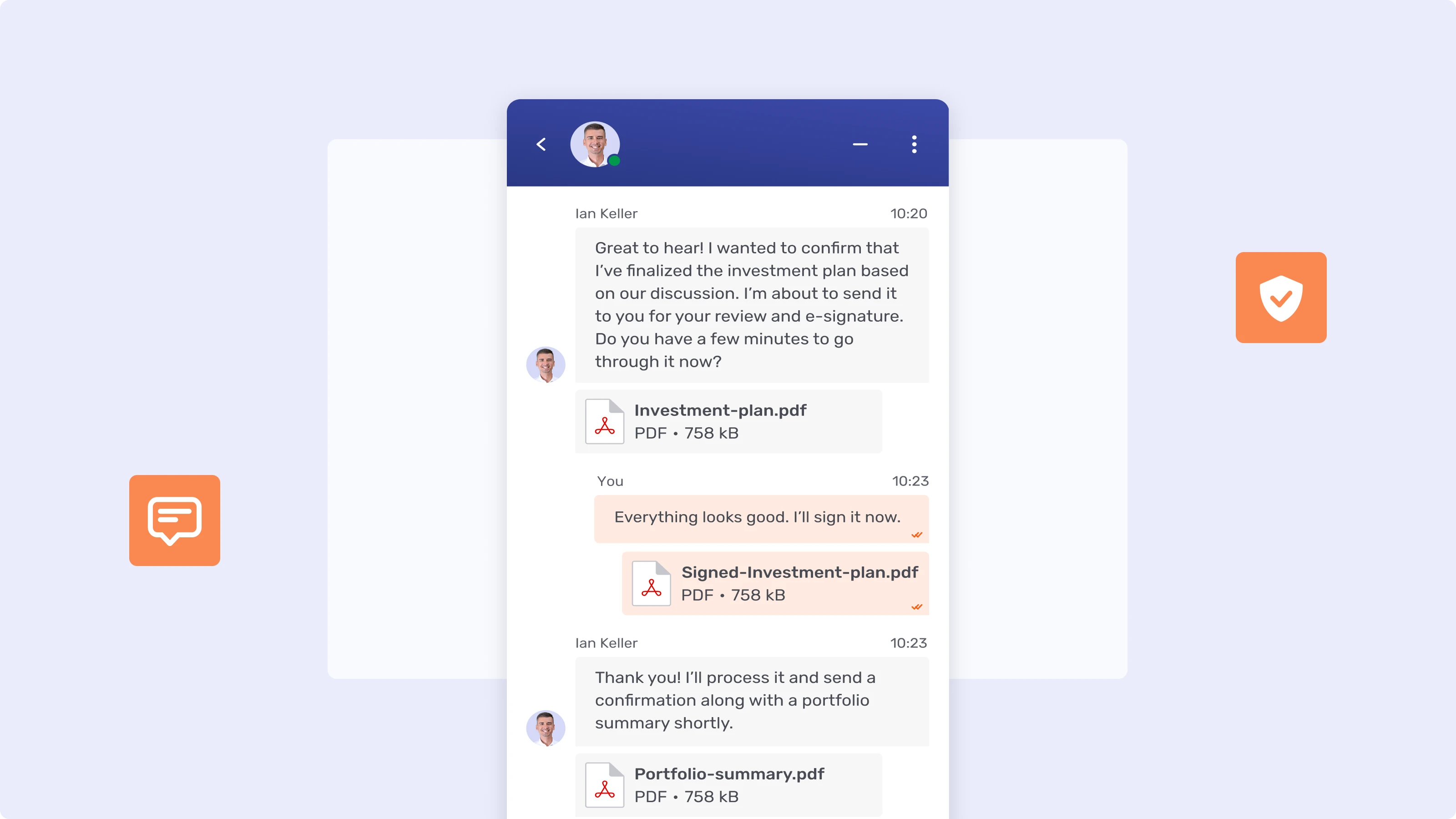

One authenticated channel, behind the bank's perimeter

Every message between client and advisor should originate inside a session the bank itself authenticated.

In practice this means a secure messaging channel embedded inside the bank's app or portal, accessed through the same SSO the client uses for account access. Every message originates from a verified session, every advisor identity is bank-issued, and no separate set of credentials exists to be phished – the only credentials in play are the ones the bank already governs. Message history is encrypted, archived, and full-text searchable inside the bank's perimeter, so recordkeeping requirements are met by default rather than as an afterthought.

For the client, the experience is closer to WhatsApp than to legacy banking software – asynchronous, conversational, with read receipts and document sharing – but every interaction is auditable. For the firm, every conversation, every deletion, and every supervisor view is captured.

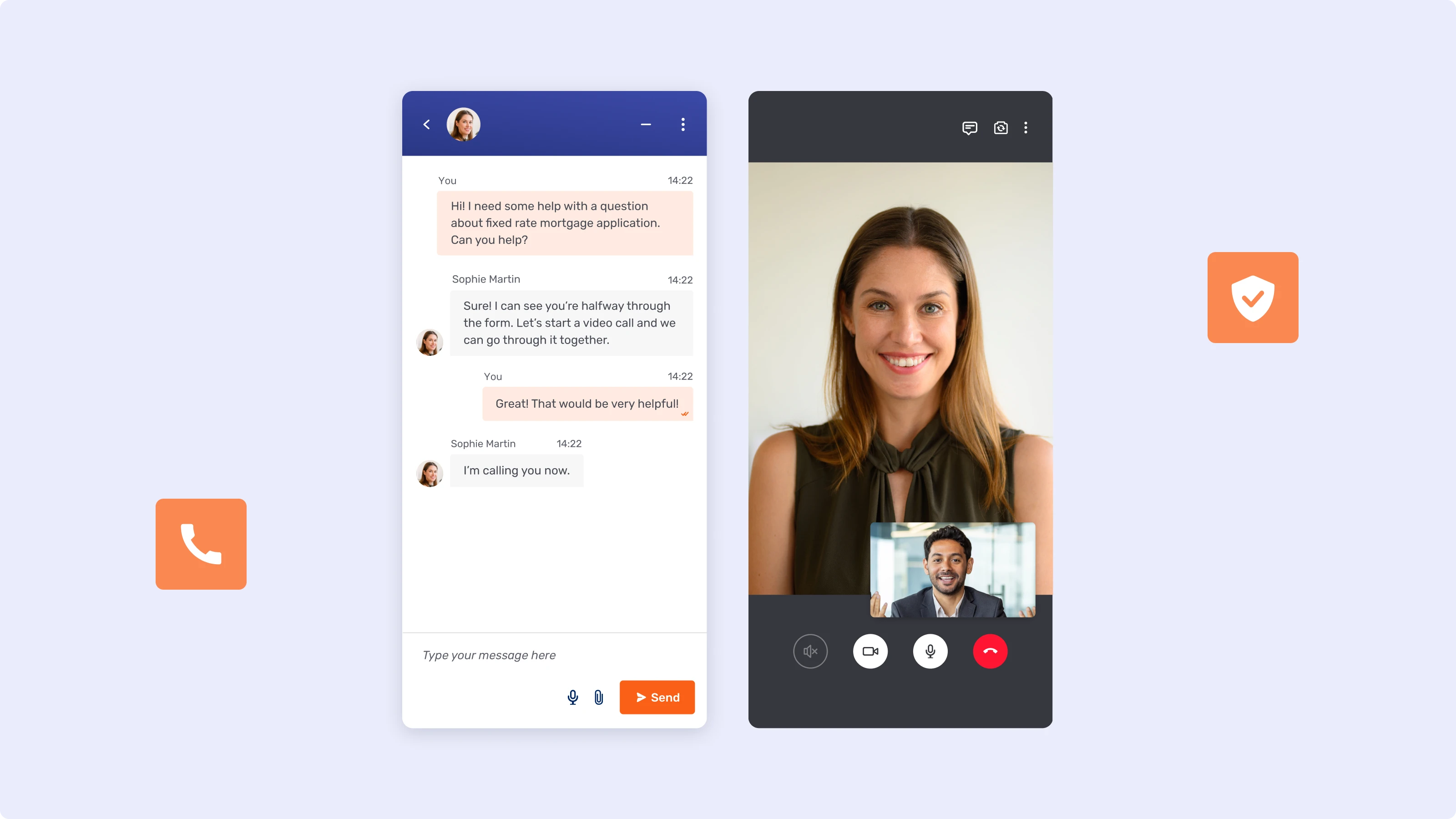

Voice and video calls that can't be spoofed

A video call only protects against deepfake vishing if both ends of the call sit inside the bank's authentication system.

Most wealth firms still rely on Zoom, Teams, or open dial-in numbers for client calls. Each of those carries a spoofable artefact – a meeting link, a phone number, an email invitation – that a fraudster can imitate.

Replace the external link with a "call your advisor" button inside the authenticated app, and the spoofable surface disappears: the client cannot be redirected to a fake call, because there is no public-facing URL or phone number to redirect them to. Caller and recipient identity are verified on both sides before the call connects, and the same authentication infrastructure that protects the messaging channel protects the voice channel.

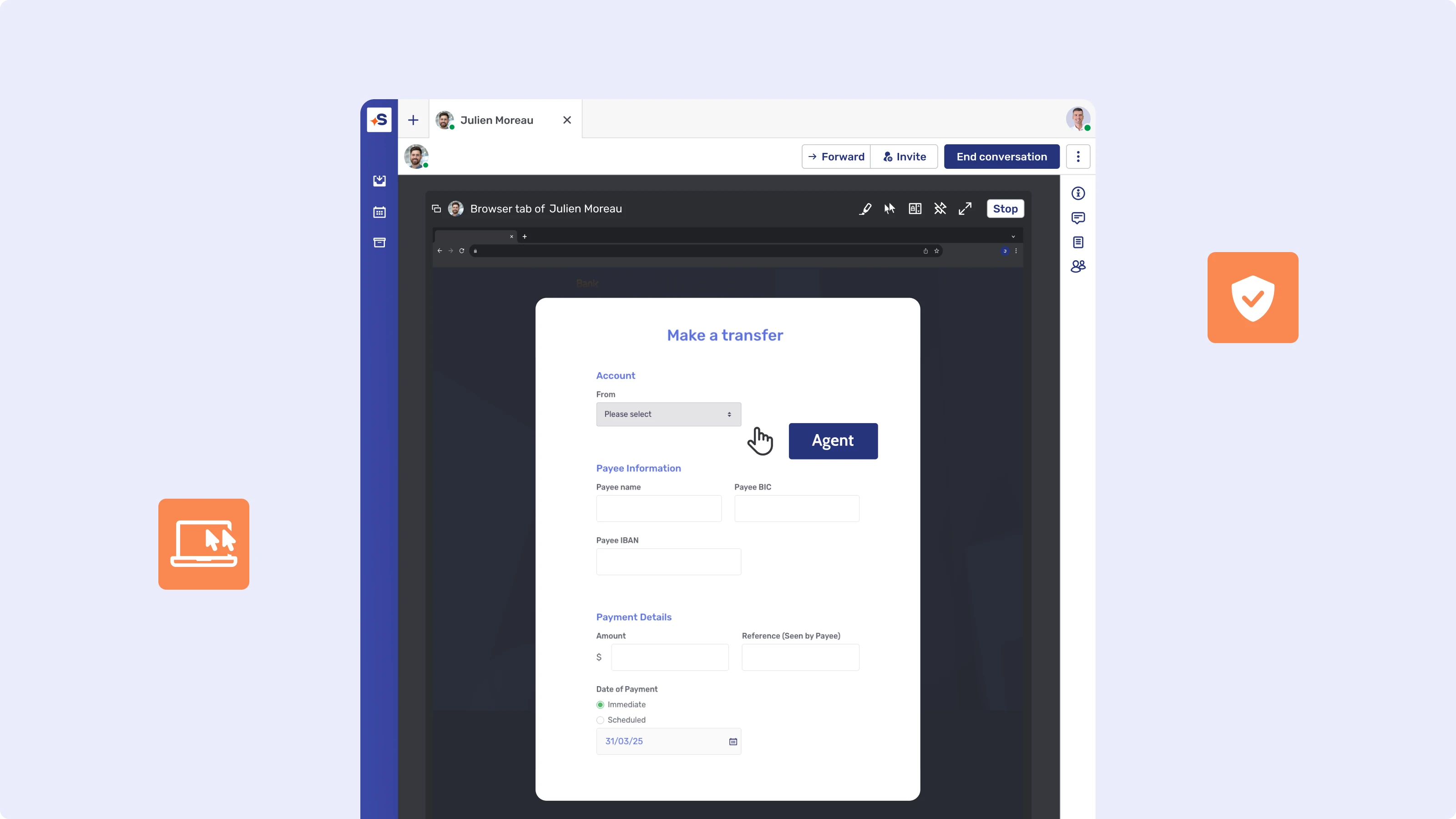

Visual verification before money moves

Most authorized push payment scams happen because the client confirms the payment alone, under pressure, on a screen they cannot show to anyone.

Co-Browsing changes that. The advisor sees the same payment screen the client sees, in real time, before the transaction is confirmed – verifying beneficiary, amount, and purpose. Sensitive fields are automatically masked from the advisor's view, so visibility is bounded by design. Co-Browsing is not screen-sharing in the consumer sense; there is no third-party software installed on the client's device, and no path for the advisor (or anyone impersonating them) to take control. The fraudster's leverage – isolating the client at the moment of payment – disappears the moment the advisor is on the screen.

How do leading firms move adoption from 30% to 70%?

Deploying a secure channel is the easy half. Getting clients to actually use it – instead of reverting to WhatsApp or replying from a personal email – is the half that decides whether the fraud surface actually shrinks. The pattern across firms that have moved adoption past the inflection point looks similar.

Meet clients on their preferred channel, without leaving the perimeter

Client channel preferences vary by market, generation, and geography, and trying to migrate every client onto a single new app underestimates how sticky existing habits are.

A client in Geneva may default to email; a client in Dubai may insist on WhatsApp; a Singapore-based next-generation HNWI may treat WeChat as the primary channel. Capgemini's 2025 World Wealth Report found that 46% of next-generation HNWIs cite a lack of services on their preferred digital channels as a reason to switch firms.

Compliant WhatsApp and SMS connectors route those channels through the same audited advisor workbench, so the conversation reaches the client where they already are while the firm retains a single audit trail. The fraud control is preserved because both sides of the channel run inside the bank's perimeter – the client experience is consumer-grade, the back-end discipline is not.

Make the secure channel faster than email

Adoption follows productivity, not policy.

The same Capgemini study finds 47% of relationship managers dissatisfied with their firm's digital tools – a number that maps directly to why advisors revert to personal email or WhatsApp under pressure. Embedded AI changes the calculus. Conversation summaries, AI writing support, captions and live translation, and a bot offering real-time answer suggestions inside the advisor's workspace mean the secure channel becomes the path of least resistance rather than the compliance overhead.

Once advisors prefer the secure channel – because it composes a follow-up in 30 seconds instead of two minutes, because it surfaces the client's last conversation without a search, because it translates a German-language reply into English in real time – the adoption curve bends without policy enforcement. AI runs inside the bank's compliance perimeter rather than outside it; every prompt and every output is audited.

Architecture sets the ceiling, adoption sets the floor

A wealth advisory firm with a perfectly designed secure communication architecture and 30% client adoption has 30% of the protection. The remaining fraud surface is the unused architecture. This is the inversion that makes 2026 different from previous fraud cycles – the technology problem is largely solved, and the operating problem is now what decides exposure.

The firms that will measurably reduce their fraud surface over the next twelve months will do three things in combination: collapse client communication onto an authenticated channel inside the bank's perimeter, meet clients on their preferred channels through compliant connectors rather than forcing migration, and make the secure channel faster than the alternative through embedded AI productivity.

Underneath all three is the same logic: fraud risk management is no longer a back-office function bolted on to client communication – it is a property of the channel itself. Firms that treat regulatory compliance as a by-product of the architecture, rather than a separate workstream, will absorb new rules with less disruption and less direct financial loss.

Unblu Secure Messenger, Video & Voice, Co-Browsing, Document Collaboration, and Aria are deployed across private banks, retail banks, and wealth advisory firms in cloud, Swiss sovereign cloud, and on-premise configurations – all sitting inside the bank's authentication, audit, and compliance perimeter.