.png)

Along with everything else that has changed in the industry, the concept of loyalty has also changed. Traditionally, banks have equated brand recognition with customer loyalty – and for a long, it worked. But with today’s consumers patterns, banking interactions that instill loyalty are not so much tied to a familiar logo but to the experience – a seamless one that lets a customer pay bills easily and move money around conveniently. Many banks have to catch up with this new reality and shift in customer perspective. The value of their brand is no longer about how well they can hold their customers’ money, but about their ability to enable the customer to move it securely and seamlessly, while supporting their decisions. As Financial Brand sees it, with consumer behaviour and technology disruption fueling social and commercial change at an unprecedented rate, the concept of loyalty in banking won’t be challenged and disrupted. Rather, it will be reinvented to be personal and pleasurable.

Loyalty = Personalisation

The Boston Consulting Group reports that personalisation is one of the primary drivers in customer satisfaction and economic value in banking.

Personalisation means making interactions simple, convenient and relevant. But making things easy isn’t easy for banks, so where do we start?

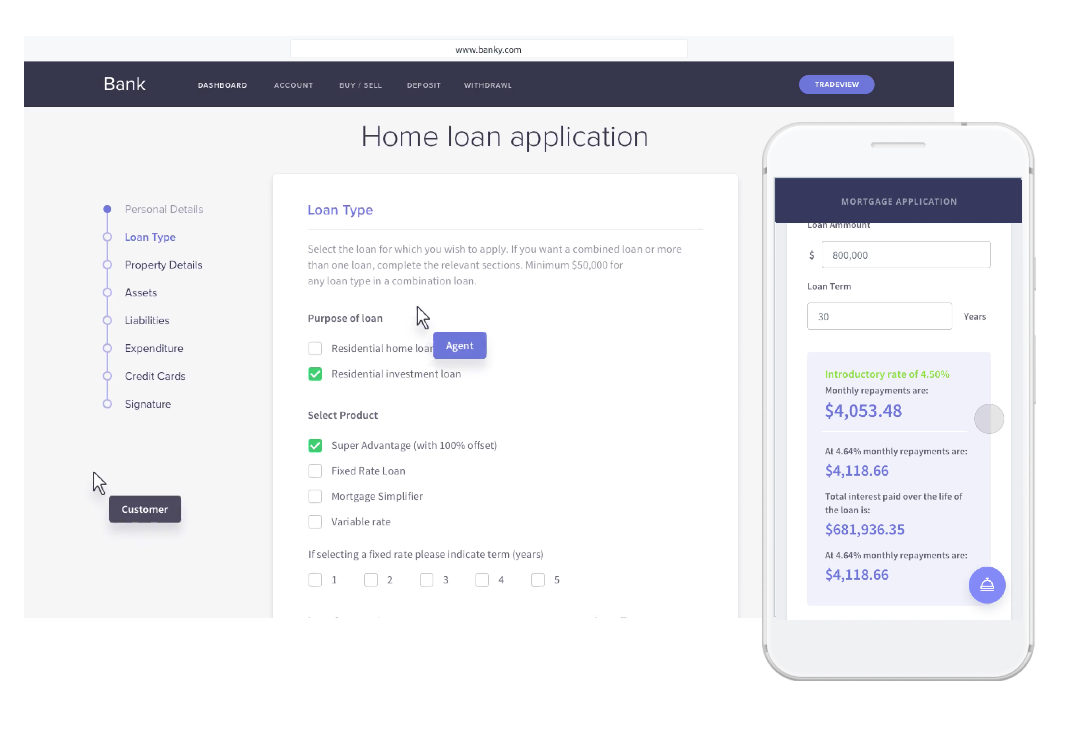

Personal = make it mobile

Personalisation often means making interactions mobile. Mobile apps have gained traction by making routine interactions easy to carry out anywhere, anytime. Apps are now playing a key role in sales and service, according to a recent Bain’s global consumer survey. Almost one-third of sales or service interactions in the past quarter occurred via mobile.

But mobile has to be a simple, intuitive experience. Ideally, a mobile app should be as close as possible to a one-click visit, allowing customers to check their account balance without needing to log-in. But an app that takes twice as long to log in to and doesn’t provide instant notifications is not simple. Expenditures that appear days after a transaction is not delightful. Monthly statements with no insight into spending patterns or tools to plan for future budgets is not helpful. So banks need to be cognizant that their (half-hearted) mobile efforts are not eroding away at loyalty.

Personalisation = Invest in Digital

According to a recent McKinsey article, the scales of banking was once a local scale game: more branches led to higher share of deposits. Digitisation now complicates this equation. “In the coming years, digital presence will start to outweigh local scale, and therefore significant digital investment will continue to drive higher growth or ROE.”

But it’s not all doom and gloom for traditional banks or for those lagging in digital transformation. With the advent of open banking and open application programming interfaces (API), the frustrating mobile or digital experience can be galvanised into something meaningful. Banks can use a third-party “layer” to enhance their digital systems and create the seamless, personal experiences customers want. Because what matters to customers is how well they can conduct their day-to-day interactions. According to a global Bain consumer survey, the battle is won or lost with every day banking because these daily interactions impact Net Promoter Score. So banks have compelling reasons to push forward with their digital transformation – the lower cost, and the fact that digital interactions —especially mobile—consistently create more customer delight for routine transactions than do traditional channels.

Of course, employees are, and will remain essential to creating loyalty, especially with complex product offerings, service and giving personal advice. But the way in which they interact with customers is changing. Rather than interact at a bank, they’ll likely communicate via mobile chat or video. This gives banks another avenue to provide interactions that delight. For instance, an employee can reduce paperwork (a big delight) while advising customers using the latest in digital tools. With the right mix of human expertise and digital or mobile tools, banks can become more customer-centric, and fix pain points and engage individually with the customer – and these are all interactions with loyalty-producing outcomes.

Banks should take a cue from the ideal loyalty-producing experience they are pursuing – it’s pleasurable and personal. In the same way, engendering loyalty shouldn’t be thought of as a technology or compliance initiative hoisted on banks because of changing legislation and consumer desires. It’s simpler and more human than that. It’s the continuous pursuit of becoming a bank that listens and communicates with each individual customer.