.png)

The gap between client-facing and advisor-facing mobile tools is becoming a measurable retention risk for private banks – and it's closer to the surface than most digital roadmaps acknowledge.

According to Capgemini's World Wealth Report 2025, 81% of next-gen HNWIs plan to leave their parent's wealth management firm within one to two years of receiving their inheritance. The most cited reason isn't fees. It isn't performance. It's digital: 46% point specifically to a lack of services on their preferred channels.

That number sits differently depending on where you sit in a private bank. For heads of digital, it's a structural problem in the technology roadmap. For heads of private banking, it's a pipeline risk – the next generation of high-net-worth clients evaluating the digital client experience against every other product in their lives before they've even received the wealth.

The thing is, both readings are correct.

Poor advisor tools is a retention problem, not just a UX problem

The conversation around digital tools in wealth management has focused almost entirely on the client-facing side: the client portal, the mobile app, the self-service dashboard. The advisor side has lagged – and the consequences are showing up in retention data.

The chain from digital tools to AUM flight

The data linking advisor tool dissatisfaction to client attrition is direct.

According to Capgemini's World Wealth Report 2025, 47% of relationship managers are dissatisfied with the tools provided by their firm. Among dissatisfied RMs, 1 in 4 say they are likely to leave within twelve months. And when a wealth manager leaves a private bank, so does the book: Capgemini found that 62% of next-gen HNWIs say they would follow their advisor to a new firm.

That chain is that poor tooling leads to RM dissatisfaction, which increases churn, and affects AUM. JD Power's 2025 US Wealth Management Digital Experience Study found that consistency between the advisor experience and the client experience is the single strongest predictor of retention at full-service firms.

What next-gen clients are actually measuring you against

Around 46% of next-gen HNWIs cite a lack of services on their preferred channels as their primary reason for leaving, making it a direct measure of client satisfaction with digital access.

That figure, from Capgemini's World Wealth Report 2025, carries a specific implication. The issue is that it isn't the quality of advice that's failing, it's the delivery channel.

What next-gen clients mean by 'preferred channels' is simpler than it sounds. They mean mobile-first, responsive, and branded. They've grown up with apps that are fast, coherent, and carry consistent design. When the advisor-client channel doesn't match – when the financial advisor is sending documents via email, managing the relationship through a desktop-first portal, or communicating via consumer messaging apps – the experience reads as institutional indifference. Only 17% of wealth management clients describe their experience as seamless across channels, per JD Power. 55% name digital quality as a factor in their decision to stay or leave.

Why consumer messaging apps make the problem worse

The instinctive response to a channel gap is to fill it with whatever's available. For most financial advisors, that means WhatsApp, iMessage, or a personal email address. It's quick. It's familiar. And it creates a different category of problem.

The brand coherence problem

When a client messages their wealth manager on WhatsApp, the experience isn't yours.

The interface is Meta's. The notifications are Meta's. The data retention model is Meta's. From a pure brand perspective, every advisor-initiated WhatsApp conversation is an endorsement of a competitor's product in the middle of your client engagement.

The compliance dimension gets the most attention – US regulators have levied over $2.2 billion in fines against major financial institutions since 2021 for off-channel communications, and the regulatory compliance requirements for record-keeping and data retention continue to tighten. But the brand problem is harder to fine. When you allow a fragmented digital estate to represent your firm, you're signalling something to clients that no amount of advisor skill can easily contradict.

What a fragmented digital estate signals to clients

Inconsistency in the digital estate signals that the firm hasn't made a considered commitment to the relationship.

This matters most when the relationship is newest – which is exactly when wealth transfer events happen.

The Great Wealth Transfer isn't a slow-burn trend. In total, $83.5 trillion is moving between generations by 2048. The moment of wealth transfer – an inheritance, a consolidation of assets – is a decision point: stay with the incumbent firm, or move. For ultra-high net worth clients, that decision is made with full awareness of what premium digital services look like elsewhere. A relationship managed partly through WhatsApp and partly through a desktop portal doesn't read as a premium private wealth service. It reads as a firm that hasn't decided what it is.

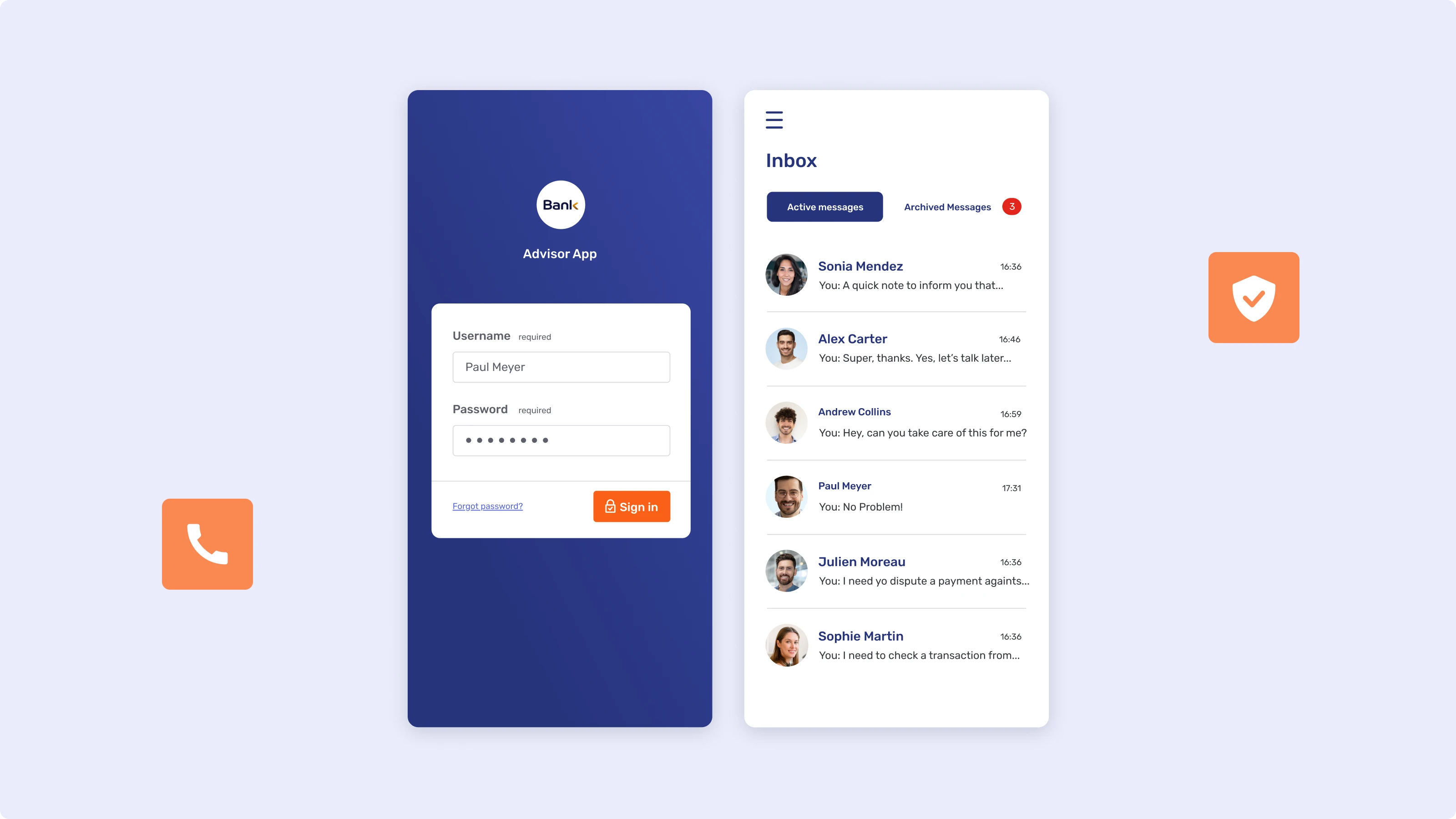

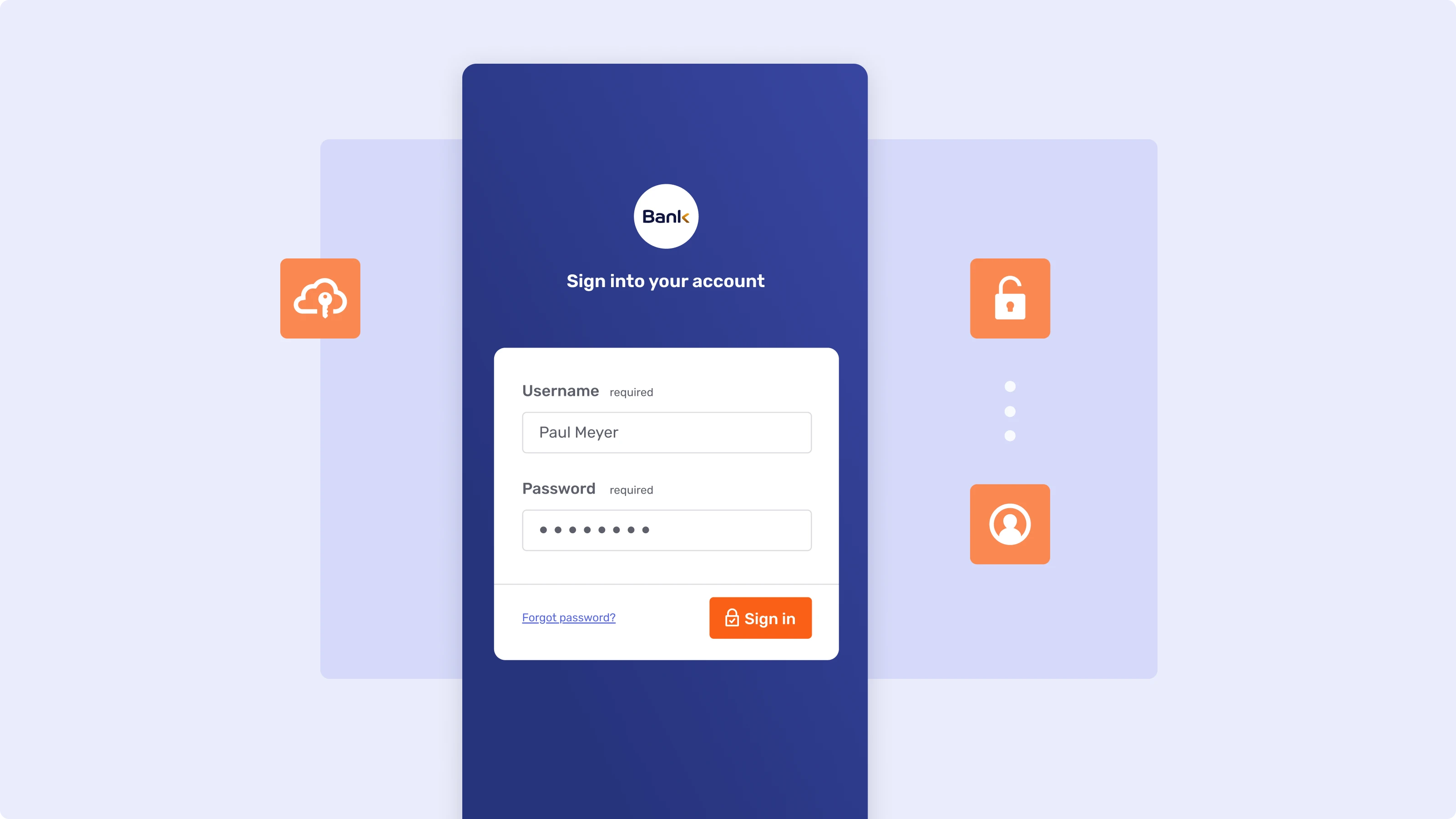

What a branded advisor app actually delivers

A brandable advisor app is a white-label iOS and Android application published under the institution's own brand – a core component of any serious wealth advisory digital strategy. Wealth managers download it from the App Store or Google Play, authenticate, and immediately have a compliant, branded channel for client communication. The institution controls the digital client experience; the client sees only the bank's identity.

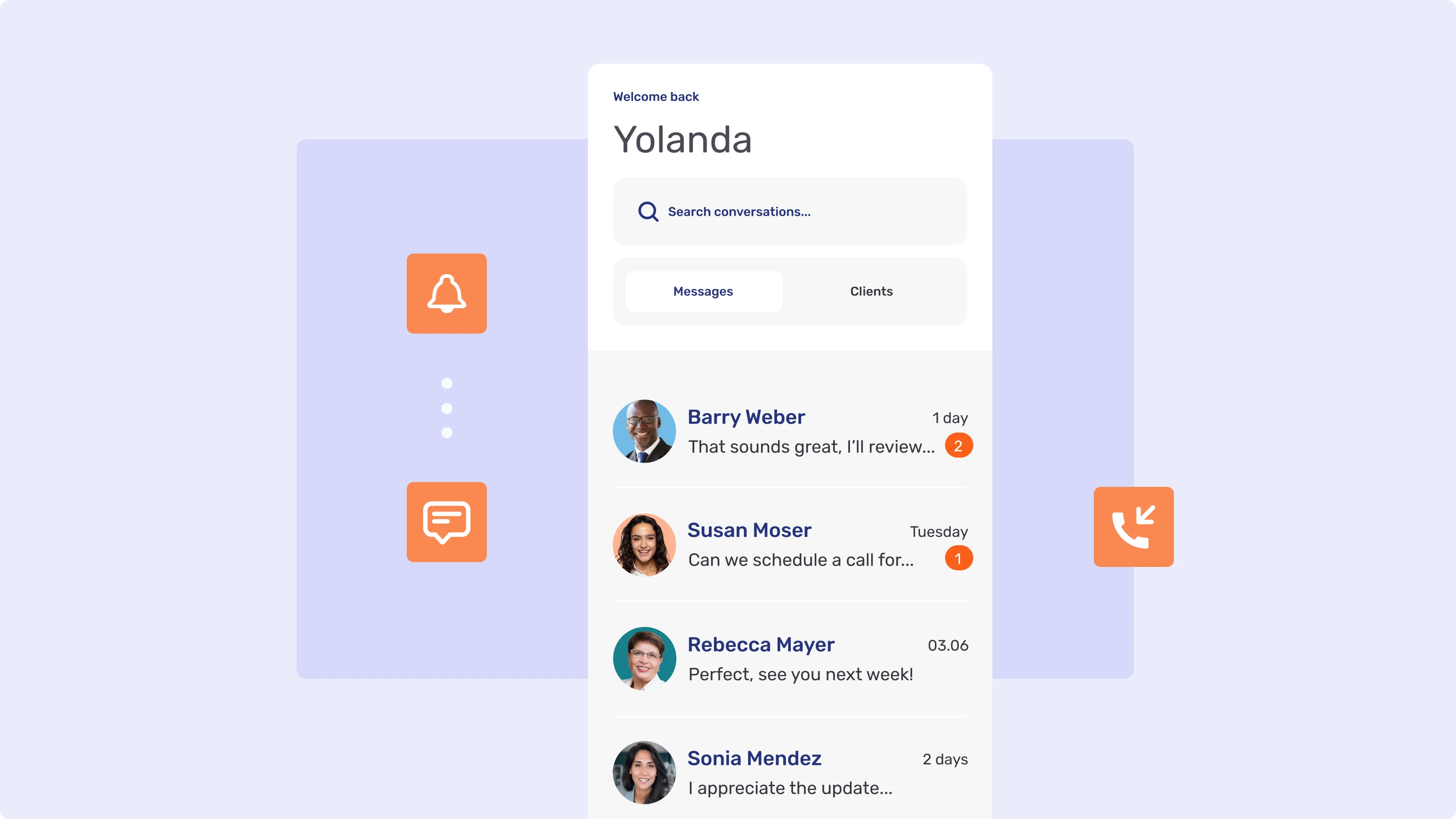

The full communication stack, under your identity

The core value of a branded advisor app isn't a single feature – it's the consolidation of the full communication stack behind a single brand identity.

Secure Messenger, Video & Voice calls, Document Collaboration, Co-Browsing, push notifications: all served from an interface that carries the institution's logo, colour palette, and authentication flows.

For the client, this matters because it creates coherent client engagement across every interaction, whether that's a routine document exchange or an urgent inbound call. For the wealth manager, it eliminates the need to manage three separate tools to serve one client. For the compliance team, every interaction is captured, logged, and auditable from day one.

Enterprise-grade security without the build cost

The security bar for a regulated financial services mobile application is well-defined.

The OWASP Mobile Application Security Verification Standard (MASVS) sets out the controls any financial mobile app must meet, and meeting them through a custom build programme takes months and significant investment.

A brandable app is a pre-built white-label solution: the security architecture – including OWASP MASVS-aligned controls for app attestation, rooting detection, keyboard security, screen capture prevention, and device binding – is already in place. The institution configures its own brand identity, authentication flows, and feature set without running a development programme. The result is a faster path to compliant digital services, at a fraction of the cost and risk of building from scratch.

Closing the gap between client expectations and advisor reality

The AUM retention risk most private wealth leaders are managing is the obvious one: performance, fees, competitive offers. The one that's harder to manage is the one you can't see in a quarterly review – the slow signal of a fragmented digital estate that tells clients, at each interaction, that the relationship isn't being taken seriously at the institutional level.

A branded advisor app doesn't solve the deeper questions of investment strategy or service model. But it closes the most visible gap in the client experience: the one between what clients see when they interact with the firm's consumer-facing channels and what they see when they interact with their wealth manager.

Unblu's Secure Messenger, Video & Voice, Document Collaboration, and push notification capabilities are available as a brandable advisor app or embedded via the Unblu SDK – deployed in cloud, Swiss sovereign cloud, or on-premise environments depending on the institution's regulatory requirements and infrastructure preferences.