.png)

What’s in store for the retail banking industry and credit unions? This year, customer experience is less about the big transformation initiatives and more about finding avenues for differentiation through customer-centricity to find that all-important competitive edge.

Customer experience is important in the banking industry because it serves as the primary driver of brand differentiation and long-term value in an increasingly commoditized market. Research into banking strategy indicates that consistent, emotionally satisfying interactions are now the key to building the trust and loyalty required to maintain high-value relationships.

The forces of digitalization are easing as most retail banks have already attained a certain level of maturity. Instead, the spotlight is now shifting towards continuous digital transformation progress. Digital transformation has impacted the banking customer experience by shifting the focus from basic online availability to the seamless orchestration of sophisticated, real-time engagement layers. Industry data shows that 53% of bank decision-makers are currently prioritizing the enhancement of digital experiences, a 20 percent increase since 2021.

Despite the overall positive trend, not all incumbent banks share the same success story. Surprisingly, 1% still claim they have no interest whatsoever in digital transformation, and another 8% have no plans for implementation initiatives. Moderately better, 10% are still in the planning phase, signifying that a combined 19% of global banking decision-makers have yet to leverage the potential of modern digital banking.

For the 10% of retail banking organizations in the planning stage, a number of barriers are hindering progress. Among the surveyed individuals, 33% cite the company’s advanced technology strategy as one of the most challenging aspects of their role. This is often complicated by legacy systems that make it difficult to integrate new tools.

Defining customer experience in 2026

Customer experience in banking refers to the overall perception a customer has of their interactions with a bank across all touchpoints – whether online, via mobile apps, over the phone, or in person. Common challenges banks face in enhancing customer experience include the persistence of legacy systems and a lack of integrated technology strategies that prevent a unified view of the customer.

In today’s competitive landscape, delivering a consistent, intuitive, and emotionally satisfying experience is key to building trust, loyalty, and long-term value in banking relationships.

1. Mobile-first communication channels

Contact center managers are continuing their efforts to streamline operations by reducing vendor complexity. The aim is to enhance customer choice and flexibility while delivering improved interaction experiences in online banking.

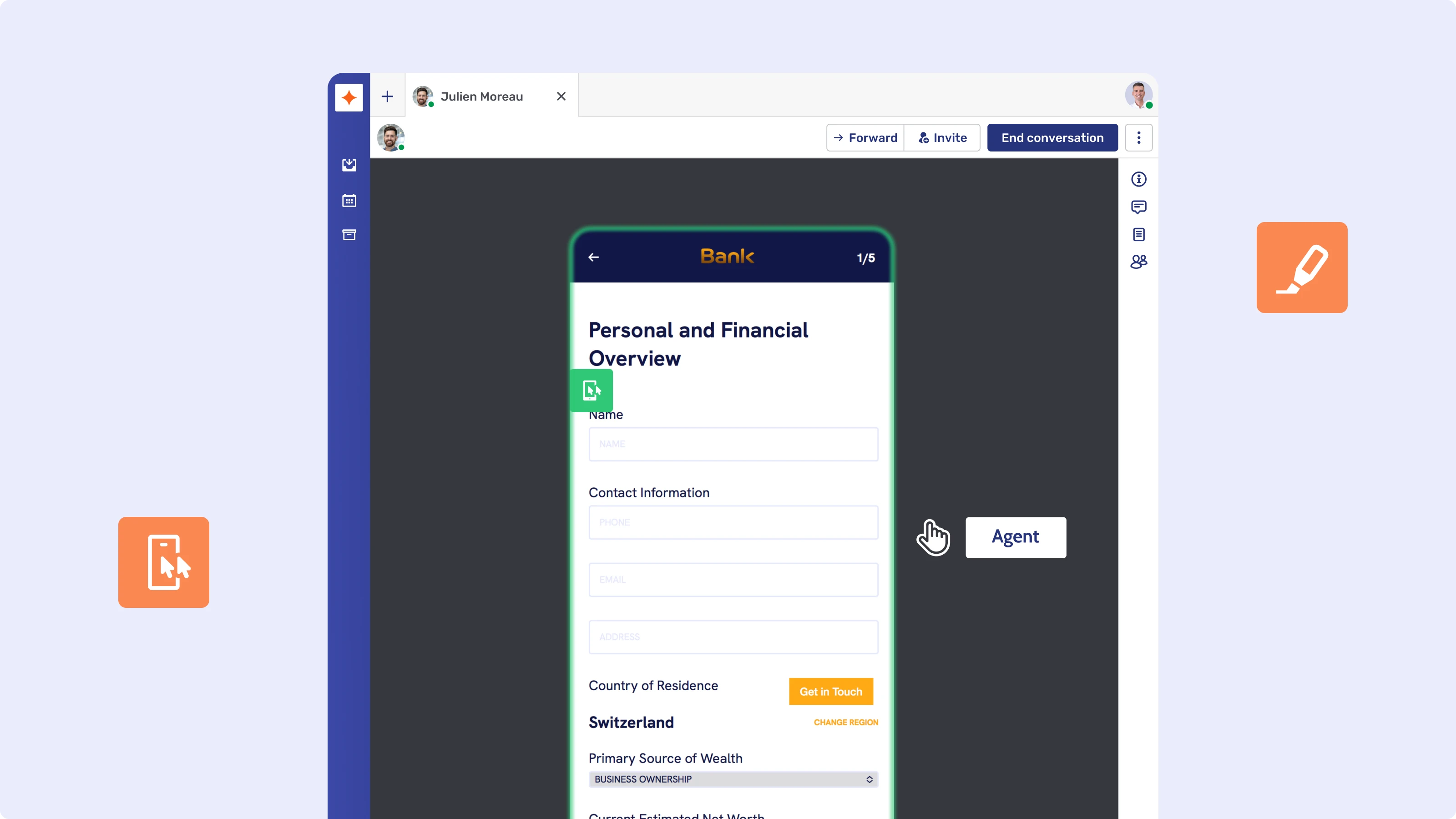

Banks can effectively use mobile apps to enhance customer experience by transforming transactional interfaces into collaborative, real-time advisory workspaces. While the mobile app is now the "heart of the relationship" with 150 interactions per year, Accenture notes that usage remains heavily transactional. There is a massive untapped opportunity to transition these high-frequency touchpoints into advisory opportunities. In 2026, the app must serve as a collaborative workspace. This involves real-time, side-by-side mobile collaboration, empowering agents to visually assist customers and resolve issues faster – and take advantage of new upsell opportunities. But it also means being able to securely send outbound messages to keep the conversation alive or add relevant information.

2. Neo banks grabbing the competitive market

Given poor experiences reported on traditional mobile banking applications, there has been an opportunity for a digital bank or innovative fintech to grab a foothold. In Spain, Revolut has managed to get nearly 20% of new customer accounts, more than traditional banks such as BBVA. This is because neo banks are particularly good at delivering personalized services that appeal to younger demographics through digital-first strategies.

Despite the rise of neobanks, incumbent abandonment rates remain exceptionally high. Capgemini reports that 47% of customers abandon digital account opening mid-process. The root cause? Only 29% of data collection is currently automated using AI, creating unnecessary friction that fails to meet customer expectations.

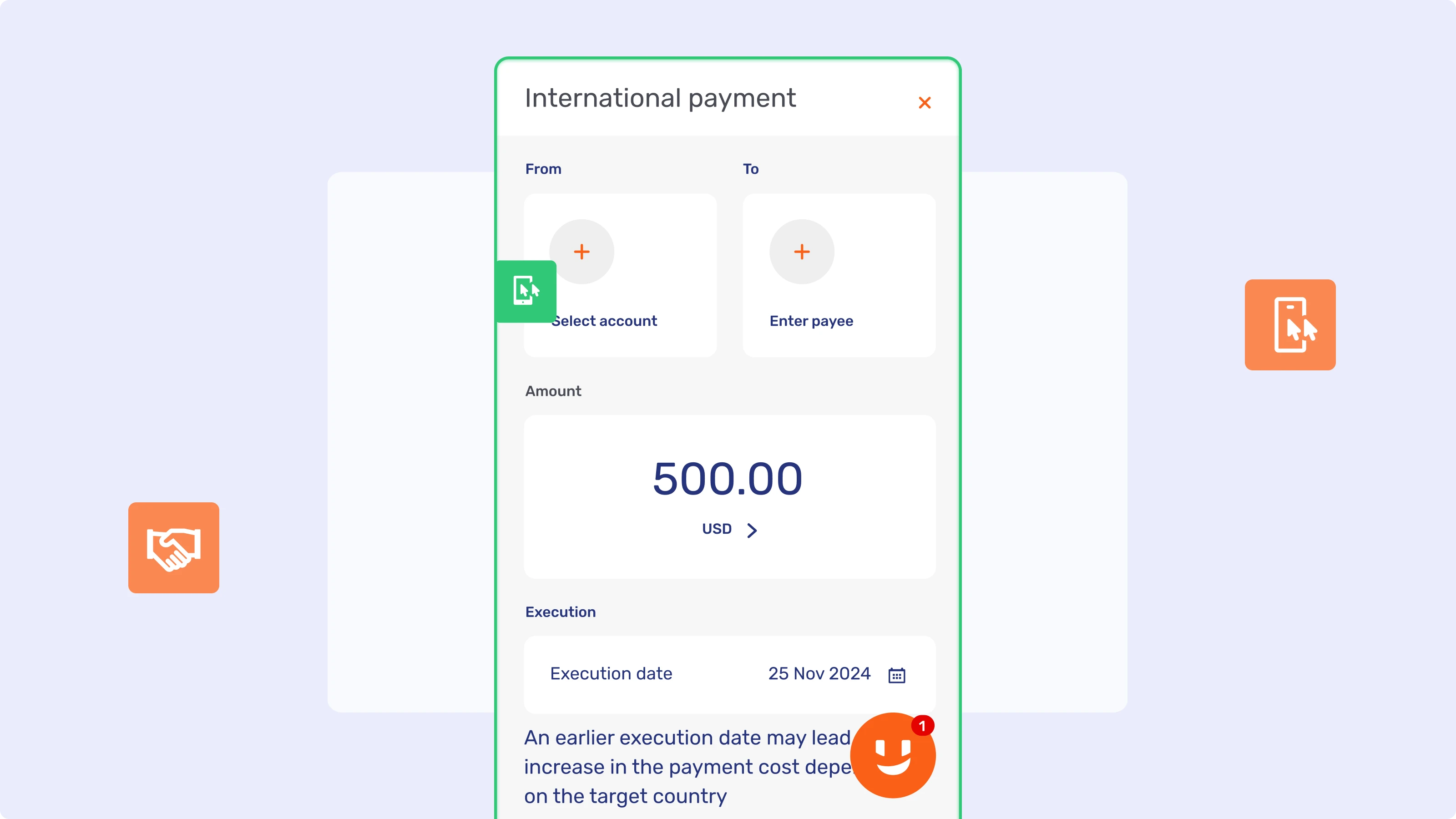

Banks must move beyond "self-service" onboarding. By integrating live collaboration and Mobile Co-Browsing during the application phase, firms can provide the "clarity and reassurance" that are a key consumer requirement for complex financial decisions, effectively slashing abandonment rates.

3. Branches are proving resilient

Recent years have shown us that traditional branches are struggling to remain viable. But this pressure may taper off as individual preferences align more closely with branch availability. According to a JD Power report, 72% of customers express their intention to utilize their nearby branch at a comparable frequency to the previous year, and 38% consider branches to be indispensable.

While the banking network has contracted, the narrative of the "dying branch" has been officially replaced by one of the “relationship hub”. In 2026, the branch is where you go for human-centered financial orchestration.

- Intentional engagement: Accenture’s 2026 Banking Trends report highlights that in a world of deepfakes, a physical branch projects "safety and soundness." Their research shows that 63% of global consumers still want a physical location to help them manage their finances.

- The micro-branch surge: The traditional 5,000-sq-ft branch is being replaced by agile formats. Accenture also reports that 76% of consumers are now willing to use micro-branches or smart banking booths – compact spaces that blend immediate self-service with instant video access to remote specialists.

4. Artificial Intelligence: Retail banks must step up

In a short time, Generative AI has moved from an exciting development to one of the most important tools in the entire financial sector. AI plays a role in shaping customer experience trends in banking by evolving from reactive chatbots into agentic systems that resolve complex workflows autonomously. Research from McKinsey indicates that Agentic AI can return 10 to 12 hours a week to bankers, expanding client coverage capacity by 40 percent.

Capitalizing on this productivity gain requires a unified environment where AI handles the administrative heavy lifting. Solutions such as Unblu’s AI-powered Workbench are designed for this specific purpose, streamlining background tasks so that advisors can prioritize personalized strategy and relationship building.

5. Hyper-personalization: The opportunity of niche journeys

There is a growing trend of neobanks concentrating on specialized market segments. Instances include platforms for the LGBTQ+ community or those dedicated to sustainability. Advanced analytics and AI-powered tools that empower banks to tailor financial personalized recommendations have resulted in a 5x increase in click-through rates for personalized offers.

In 2026, the new frontier is solving the so-called “emotional resonance gap”. While most institutions have achieved functional digital efficiency, Accenture reports that these channels are often "functionally correct, but emotionally devoid."

For leaders, the competitive edge no longer lies in digital availability, but in customer advocacy and growth. Banks that achieve high advocacy grow revenues 1.7x faster than their peers. The goal is to move from transactional interfaces to interaction layers that facilitate "emotional resonance" through seamless human-digital hybridity.

6. Orchestrating the "Digital Memory"

A critical friction point in 2026 remains the "Hand-off Problem." Accenture reveals that 64% of consumers still revert to physical branches when digital channels fail, only to find they must "start over" due to fragmented customer data.

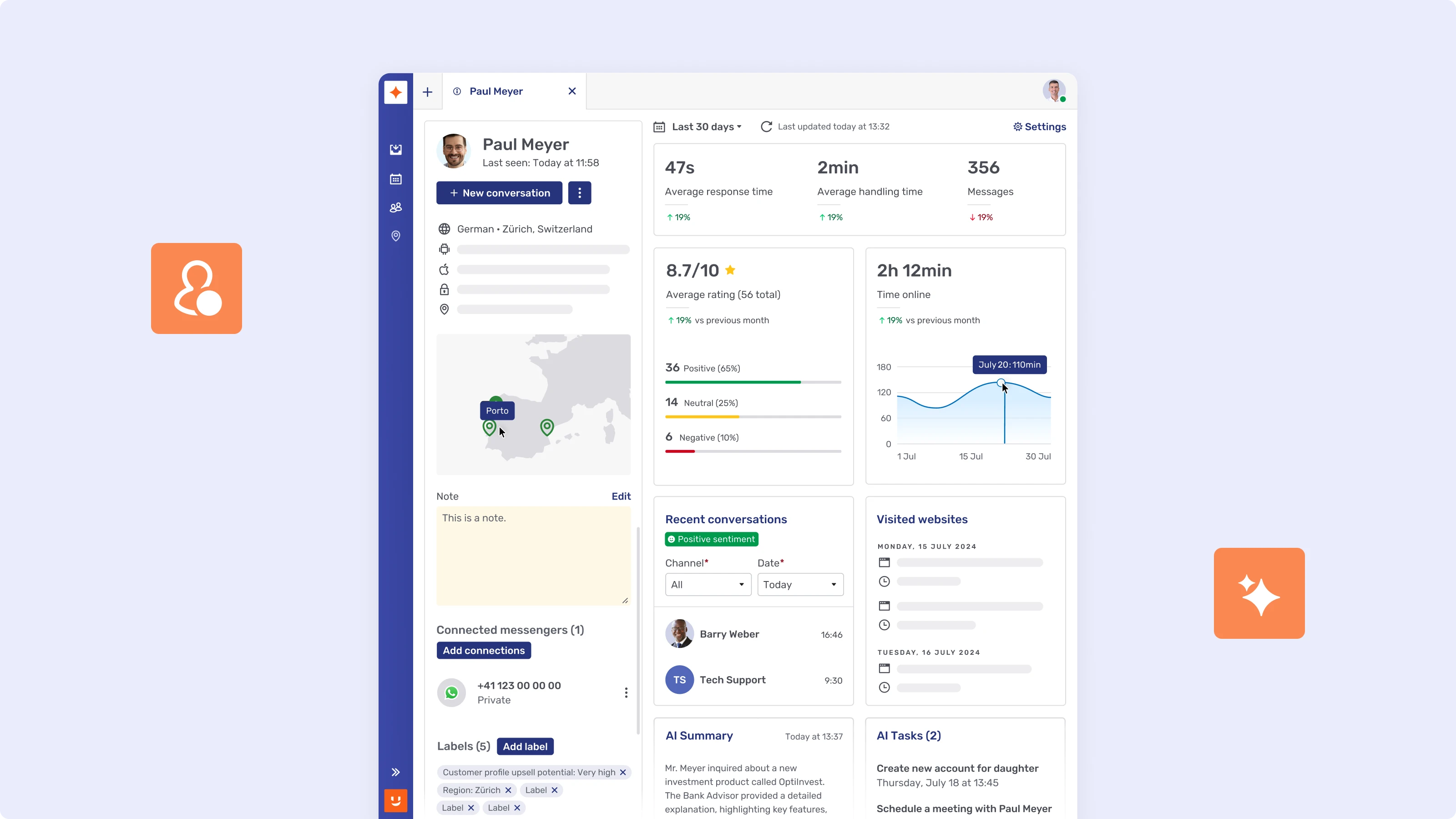

Success requires a "Digital Memory" layer that maintains conversation context across every touchpoint. Technologies driving customer experience trends in banking include unified conversation layers, Mobile Co-Apping, and secure messaging tools that preserve context throughout the lifecycle.

This ensures that every interaction is a continuation of the last, transforming service from a "cost center" into a primary value driver for the firm. Achieving this seamless experience is now a top priority for 86 percent of banking executives who recognize that context is the key to service excellence.

7. The benefits of social banking

AI-powered capabilities aren’t the only fad set to transform banking customer behaviors entirely.

Social media is changing the game and banks are increasingly using platforms like Instagram, TikTok, and YouTube to connect with younger audiences by building trust through authentic and engaging content.

In fact, a reported 35% of Gen Zs have used social media to search for information, compared to just 21% of Millennials. When we look at older generations, the percentage falls even further, with 13% of Generation X, 11% of Boomers, and only 9% of the Silent Generation using social media to this end.

Another source found that the number of 18-34 year old investors who use Reddit and TikTok to access financial knowledge has jumped dramatically in the last three years, moving from 17% to 26% on Reddit and from 12% to 20% on TikTok.

Strategies for experience-led growth in banking

As the financial industry pivots toward deeper personalization, experience-led growth has become a strategic imperative. As McKinsey says, banks need to “reimagine, not just de-friction, priority journeys,” finding ways to deliver a smooth customer journey across touchpoints.

Practical frameworks

- The 3Cs Model: Context, Continuity, Convenience.

- Hybrid engagement layers: Combine asynchronous (e.g., Secure Messenger) and synchronous (e.g., live chat, video banking) channels.

- Action steps: Invest in collaboration tools, implement journey analytics, and train advisors for digital empathy.

The future of banking in 2026

This year, financial services organizations should focus on providing superior customer experiences. Customer expectations are continuing to evolve and driving loyalty is no easy task. From the actual products to the incorporation of agile technology solutions, the ability of banks to provide agility without sacrificing deeper customer engagement is paramount.

The banks that will come out on top are those that provide robust digital channels that avoid poor experiences. By providing a mix of mobile banking apps, physical branches, and niche products that cater to the entire customer journey, professionals will be better positioned to drive revenue growth while avoiding the "emotional void" of 2026.