.png)

Wealth management in 2026 is defined by a fundamental shift in how client relationships are built, managed, and sustained. Performance still matters – but it is no longer enough.

Today’s leading firms are moving from fragmented tools and reactive service models toward orchestrated, intelligence-driven experiences that combine personalization, security, and human expertise at scale.

From unified client intelligence and agentic AI to mobile-first engagement and digital trust, the trends shaping this year point to a single imperative: advisors must be empowered to act with greater context, confidence, and relevance at every moment that matters.

The following trends reveal how industry leaders are making that transition.

1. The emergence of the “Unified Client Brain”

In 2026, wealth management is moving decisively beyond fragmented data models toward what many leaders now describe as the “Unified Client Brain.” Rather than relying on disconnected CRMs, portfolio systems, and engagement tools, firms are consolidating behavioral signals, market sentiment, and life-stage indicators into a single, AI-driven intelligence layer.

This architectural shift marks a move from backward-looking analysis to continuous, real-time understanding of the client. As highlighted by Oliver Wyman, a Unified Client Brain allows firms to deliver true personalization at scale – not through static segmentation, but through dynamic interpretation of intent, context, and opportunity. The result is a transition from reactive reporting to proactive, high-touch orchestration of the client relationship.

What this means for wealth managers:

- Move beyond the traditional CRM

Client profiles must now incorporate real-time digital interaction data – including chat conversations, Co-Browsing, and video-based sentiment signals – and feed it directly into core analytics and decision engines.

- Orchestrate digital journeys, not touchpoints

The Unified Client Brain enables firms to identify high-value “moments of truth” and trigger timely human intervention, while automating routine activities such as portfolio monitoring and rebalancing. Advisors engage where they add the most value; technology handles the rest.

This trend sets the foundation for a more responsive, scalable, and relationship-driven wealth management model – one where every interaction is informed, intentional, and context-aware.

2. Alternative investment strategies

By 2048, an estimated 83.5 trillion dollars in wealth will be passed down to younger generations, specifically Gen X, millennials, and Gen Z individuals, who are considered “Next-gen HNWIs.”

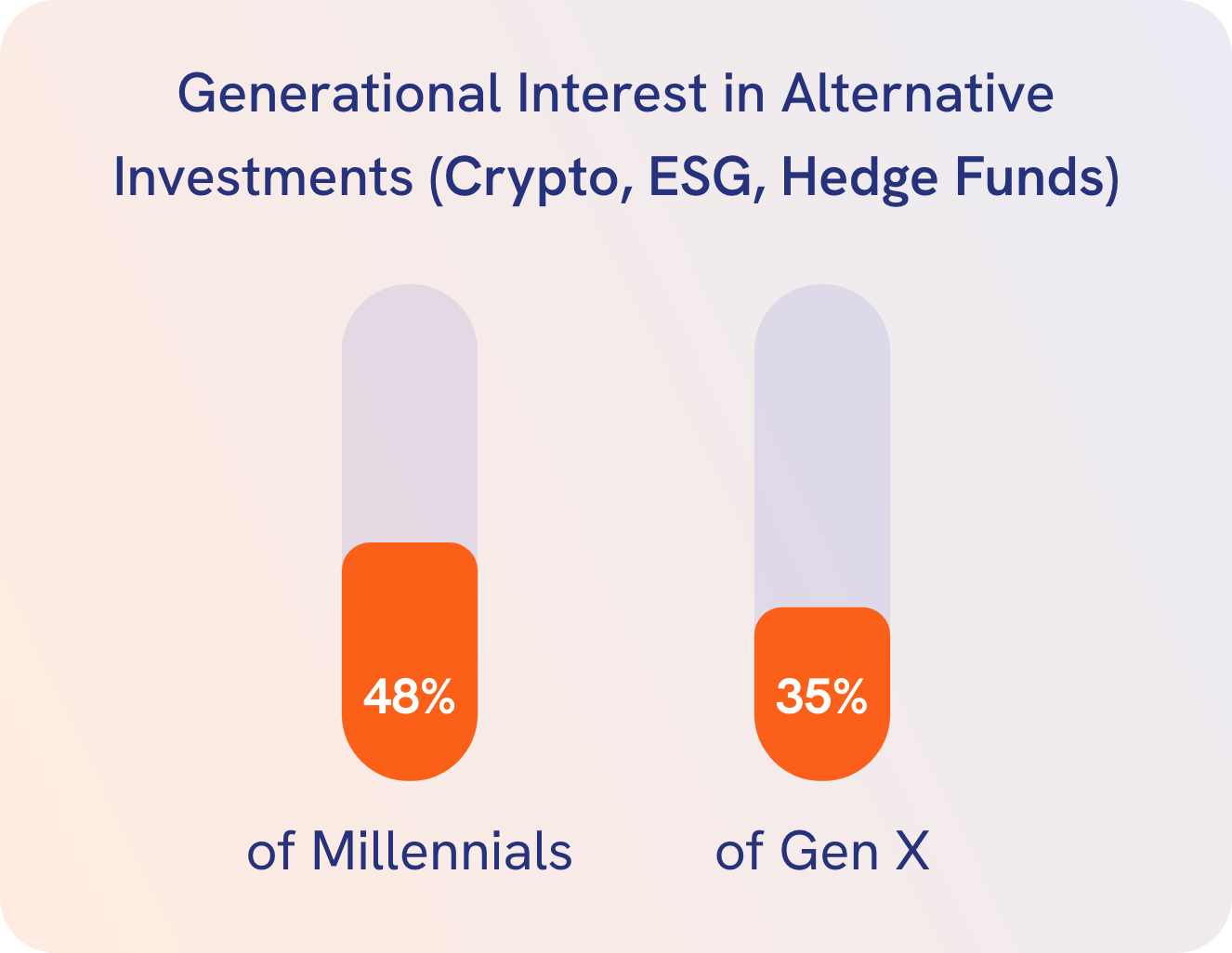

Gen X and Millennial wealth holders are showing increased interest in cryptocurrencies, ESG investments, hedge funds, and similar options, with a reported 48% of Millennials and 35% of Gen X claiming they’d like to discuss crypto investments with their financial advisors.

For wealth firms, adjusting to this new reality means aligning with “beneficiaries’ aspirations” as the Capgemini trends report puts it. As a result, we are witnessing a new trend where WM firms are tailoring their offerings to younger generations. This includes “providing digital advisory and adapting investment strategies to align with the diverse interests of the new heirs.”

3. Increasingly sophisticated service expectations

Investment performance remains a core expectation, but in 2026 it is no longer the primary driver of client satisfaction. Instead, personalization and service quality have become the key differentiators in the wealth management experience. Client behavior has shifted and they now expect interactions that are timely, relevant, and tailored – combining digital convenience with trusted human advice journeys.

These expectations span demographics and wealth segments, led by younger and digitally native investors, but increasingly shared across all client groups. Research shows that 51% of high-net-worth individuals now demand self-service tools and advanced technologies to support portfolio management and everyday interactions. Digital capability is no longer optional, even for traditionally relationship-led clients.

At the same time, investors want more proactive and meaningful engagement from their advisors. According to Accenture, 39% of clients want to hear from their advisors more frequently, particularly during periods of market volatility or life-stage change. This shift requires firms to move beyond reactive, schedule-driven reviews.

Wealth managers can meet the evolving service expectations of wealth management clients using tools such as Unblu’s Co-Browsing, which turn portfolio reviews into interactive, collaborative sessions – strengthening understanding, confidence, and long-term trust.

4. The growing female segment

fueled by an unprecedented intergenerational wealth transfer. Market intelligence firm Cerulli anticipates that $124tn in wealth will be transferred between generations by 2048. Of this amount, $40tn is projected to transfer to widowed women from the baby boomer and older generations, before ultimately being passed on to heirs and charities (PWM).

But what does this segment want? According to Capgemini, women value quality service more than their male counterparts, alongside putting emphasis on fees, product transparency, and data privacy and security. When it comes to services, 75% state that retirement and inheritance planning is important, while 76% value tax consultation and 71% focus on legal support.

They also have less confidence in their primary wealth management industry organizations than men and in their ability to grow wealth over the next year. Firms that are able to better personalize their offerings for this segment will gain a competitive advantage.

5. From chatbots to agentic AI partnerships

The phase of lightweight Generative AI pilots is largely behind us. In 2026, wealth management firms are shifting their focus to Agentic AI – autonomous systems designed to execute complex, multi-step workflows rather than simply respond to prompts or queries.

According to EY, nearly 70% of banking firms now use agentic models to support advisor desktops, delivering real-time “next-best-action” recommendations, surfacing relevant insights during client interactions, and continuously monitoring for compliance risks.

This represents a fundamental evolution in how AI supports the advisory function: from passive assistance to active participation.

Crucially, this trend is not about removing the human from the equation. Instead, it marks the rise of the AI-augmented advisor. By delegating research, documentation, and administrative preparation to AI agents, advisors reclaim time and cognitive capacity for what matters most – trust-building, empathy-driven strategy, and holistic life-planning conversations that high-net-worth clients increasingly expect.

As one industry narrative now puts it: we are moving from AI as a tool to AI as a colleague, with the advisor acting as the primary orchestrator of a high-tech ecosystem that works continuously in the background to elevate every client interaction.

6. Cybersecurity as a high-touch client experience

Cybersecurity has moved beyond the back office to become a front-line client experience issue. As AI-driven deepfake fraud and advanced social engineering attacks accelerate, clients are increasingly judging wealth managers by the security and integrity of their digital interactions, not just investment outcomes.

Legal experts at Baker McKenzie warn that AI is a double-edged sword for cyber resilience: it strengthens defenses while enabling more convincing attacks. In response, leading firms are adopting zero-trust communication frameworks, ensuring every interaction is authenticated, monitored, and protected by design.

For ultra-high-net-worth individuals, secure communication is no longer a hygiene factor. It signals professionalism, discretion, and long-term reliability. In 2026, cybersecurity is not simply about risk mitigation – it is a defining element of a premium, trust-led client experience.

7. Secure and compliant messaging channels

Secure and compliant messaging channels are crucial for wealth advisors because clients expect instant, conversational access. While consumer apps offer convenience, their unauthorized use has resulted in billions in regulatory fines and significant reputational damage across the industry.

Financial-grade messaging platforms allow advisors to remain “always on” while ensuring all communications are encrypted, recorded, and fully auditable. This is essential in an environment of heightened regulatory scrutiny, where informal channels create unnecessary compliance exposure.

In 2026, leading firms are moving away from WhatsApp and SMS toward purpose-built messaging solutions for regulated environments. Tools such as Unblu Secure Messenger combine a familiar chat experience with data sovereignty and compliance – protecting both the advisor relationship and the institution.

8. Mobile-centric client experiences

Mobile accessibility is no longer optional in wealth management, it is a core digital transformation expectation, particularly as 40% of banks now view Big Tech firms as their primary competitors for younger investors’ portfolios. Clients increasingly expect to manage, monitor, and engage with their wealth wherever they are, through the device they use most.

Mobile-centric experiences matter for modern wealth management clients because they provide real-time visibility and control, from tracking tax documentation to accessing timely trading insights. For modern clients, especially younger generations, mobile is the default channel for decision-making and interaction. However, trust remains a critical factor. Research shows that 54% of younger investors still distrust robo-advisors during periods of market volatility, reinforcing the continued importance of human guidance.

This creates a clear imperative: wealth firms must combine mobile convenience with advisor access. Technologies such as Unblu’s mobile Co-Apping make this possible by allowing advisors to securely join clients inside their mobile app.

Advisors can guide decisions in real time, explain options, and provide reassurance during critical moments – delivering a mobile-first experience without sacrificing the human relationship.

9. Relationship manager productivity

Despite rising client expectations, advisors today spend only 58% of their time on client-facing work, with the remainder absorbed by administrative tasks, documentation, and KYC processes. This imbalance limits both advisor effectiveness and relationship depth.

Modern wealth managers leverage technology to improve productivity by automating routine transactions, compliance checks, and document verification. When these operational tasks are handled by technology, advisors regain time and focus for high-value activities such as strategic planning, proactive outreach, and relationship development.

Platforms like Unblu support this shift by combining AI-enhanced secure messaging, video and voice communication, and visual collaboration in a single environment. Advisors and clients can exchange ideas, documents, and approvals seamlessly, without switching channels or compromising compliance.

In practice, this approach has delivered measurable results: firms using Unblu have seen a 25% increase in front-office productivity and a 5–10% uplift in the time relationship managers spend with clients. Integrated artificial intelligence further streamlines onboarding and servicing, allowing advisors to focus on what matters most – building trust and delivering personalized advice.

10. Appealing to younger generations with social media

ESG initiatives have been on the rise for years. However, this trend appears to be changing.

A 2024 Stanford Graduate School of Business study found a significant decline in support for environmental, social, and governance (ESG) initiatives among Millennial and Gen Z investors.

But that’s not to say these initiatives are completely out the window for younger generations. Despite this decline, this generation does continue to prioritize transparent environmental, social, and governance (ESG) factors more than previous generations, as highlighted in a Financial Times article.

As for where younger generations get their information, we are also noticing a demographic shift. While only 3% of Baby Boomers use social media to make investment decisions, Millennials and Gen X are increasingly turning to these channels. A reported 33% and 21% respectively claim to use social media in this way, especially on YouTube and X (formally Twitter).

For wealth firms, this activity on social media platforms and forums can provide insights into current opinions among specific private market segments. It also provides an opportunity to have a positive impact by attracting new and highly active investors, while increasing long-term engagement.

Orchestrating trusting human relationships

Taken together, these trends signal a decisive evolution in wealth management: from managing products and processes to orchestrating trusted, human-centered relationships through technology. Unified intelligence, agentic AI, secure communication, and mobile engagement are no longer separate initiatives. Now, they are interdependent capabilities that define modern advisory excellence.

In 2026, competitive advantage belongs to firms that use technology not to distance advisors from clients, but to bring them closer – with better insight, stronger trust, and more time for meaningful conversations. The future of wealth management is not automated or analog. It is orchestrated, secure, and deeply human.