.png)

The battle for customer loyalty and acquisition has never been more intense among financial institutions. Achieving sustainable customer acquisition at a reasonable cost is a huge challenge as today’s consumers are more discerning than ever, expecting both seamless transactions as well as personalized experiences that cater to their unique financial needs.

For banks to thrive in this competitive landscape, a strategic focus on both customer acquisition and retention is paramount. But what can retail banks do to put their customers at the center of their growth strategies?

What current and potential customers care about

When designing a new strategy, the first port of call should always be examining customer preferences, particularly with regard to customer engagement. Modern banking customers have entirely transformed when compared to even ten or twenty years ago. This raises a number of interesting questions in the banking sector.

Digital vs. in person options

There has been an undeniable trend towards digitalization and digital banking in the financial services industry, which has put strain on traditional banking operations. For example, there has been a consistent downward trend in the use of physical branches, with customers expecting digital channels and mobile applications as part of their everyday banking experience.

But physical branch locations shouldn’t be relegated to the annals of history as there is still a definite demand for them – even if people plan on using them less. Although people plan to visit them less often, 82% of customers still value having one locally.

This would explain why we’re seeing strong success with hybrid branch options, which are more cost-effective to run while also offering the in-person experience that customers require at specific moments.

When customers prefer human support

Even with the incredible leaps forward in AI, there are times in the customer journey when they prefer to speak to a human agent, something that is essential for ongoing customer loyalty. In fact, a Forrester report found that seamless experiences that are hybrid score higher on effectiveness, ease, and emotion than digital-only or physical-only experiences.

This isn’t solely based on financial institutions’ self-reports and surveys. In terms of customer acquisition strategies, there are trends that appear to support that going entirely digital will result in challenges down the road. Over the last few years or more, there has been a solid rise in digital-only fintech companies.

One that proved particularly popular in the United Kingdom was Monzo. As is characteristic of these fintech companies, Monzo offers current and potential customers a truly exceptional digital experience, with everything from onboarding to ongoing interactions taking place in an entirely virtual environment.

In 2018, Monzo took the United Kingdom by storm, cementing a large market share and winning a lot of business from incumbent institutions. This trend, while slowing, continued up until 2022, when for the first time their customer churn overshadowed acquisition, losing more than 2,000 customers in the fourth quarter 2022.

It is too early to tell exactly why Monzo is losing customers. It could be to do with the rise of competitors like Revolut, which has the most current customers of any digital bank in Europe. That said, if we look at the acquisition numbers for 2023, what’s notable is that all the banks with positive acquisition numbers are traditional banks or ethically focused ones, as in the case of Triodos Bank.

What is safe to say is that robust digital experiences alone are not enough for effective customer acquisition or to meet ongoing customer expectations.

An exceptional yet balanced experience

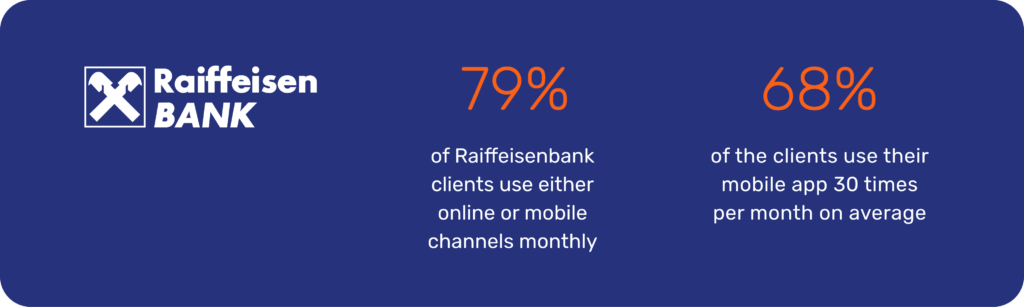

For an example of robust digital tools combined with a human-centric strategic approach, we can look at Raiffeisenbank, a retail bank that’s based in the Czech Republic and is part of the RBS group.

Like the fintech companies, Raiffeisenbank has a strong digital offering. In total, 79% of their clients use either online or mobile channels monthly, and 68% of them use their mobile app 30 times per month on average. Having a strong digital foundation certainly played a key role in the customer acquisition process.

Reputation among your customer base

However, reputation is everything. In the banking sector, just like every other context, loyal customer referrals are an exceptionally important means of continued customer retention and in growing a bank’s customer base. For example, a series of online reviews with poor customer feedback going back to at least 2020 undoubtedly affected Monzo’s reputation and curbed their growth.

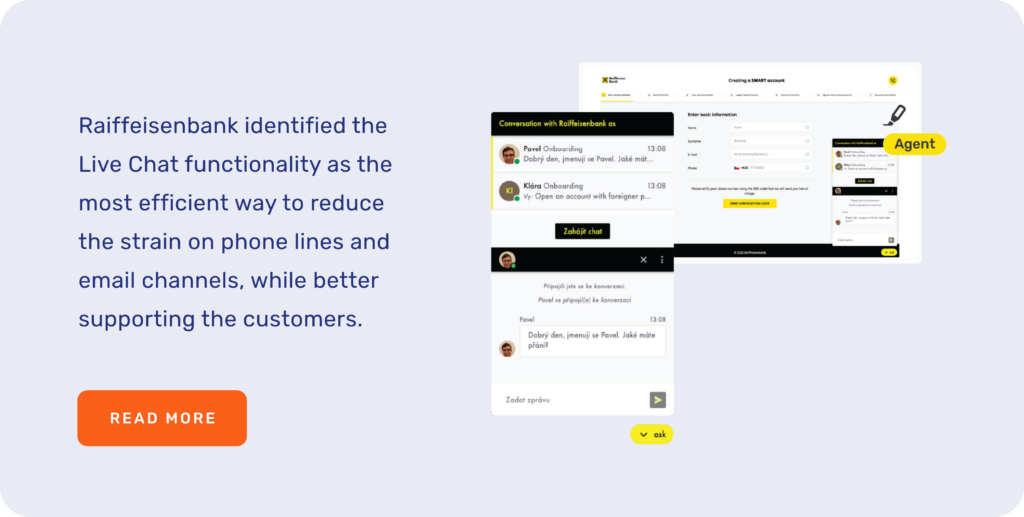

This was the exact scenario that Raiffeisenbank wanted to avoid, specifically with regard to their customer service experience. Displaying great foresight, the team realized that they were fielding too many calls in their contact center, which was risking a poor customer experience.

To address this, Raiffeisen began collaborating with Unblu, incorporating the Live Chat functionality to deflect calls. While this worked, the bank soon found an increase in overall inquiries and customer queries (as it was easier to get through to the bank) and so they took the step to implement Co-Browsing as well. These steps allowed the bank to ensure their ongoing reputation remained positive.

Maximizing conversions

Having improved the customer experience, Raiffeisenbank was in a better position to leverage conversion opportunities. To capitalize on this, at the end of successful interactions with happy customers, agents were instructed to offer financial products based on a recommendation from the bank’s CRM.

On the Live Chat channel, a total of 12,00 sessions took place during the tracking period. Out of these, 6,400 showed the potential to lead to a new upsell opportunity, with 320 new deals actually taking place by August 2022. This represented a 5% conversion rate – which rose to 8% the following September.

Interested in Raiffeisenbank’s story? Read the full case study here.

Boosting bank customer acquisition and retention

There is no magic customer acquisition strategy to boost acquisition and retention in banking. To achieve success, it requires a mixture of robust digital capabilities, a differentiated product offering, effective marketing strategies, a social media presence, and a strong overall reputation.

By collaborating with Unblu, banks gain access to a flexible conversational solution that molds to their specific context, allowing them to deliver better and more engaging interactions.