.png)

How does your bank or credit union compare to other financial institutions in terms of customer service? Are they offering new digital banking services that improve their customers' experiences?

Digital banking is transforming the financial industry by shifting the focus from purely transactional interactions to a model centered on continuous, data-driven customer engagement. This evolution is driven by the need to stay competitive against non-bank competitors, as banking decision-makers now prioritize long-term digital maturity over one-off transformation projects.

The dramatic shift in digital habits, behaviors, and digital capabilities has led to a tumultuous landscape filled with challenges and opportunities. Not only are traditional banks facing unprecedented competition from nonbank competitors and digital-native banks, but banks and credit unions are also competing against each other for consumer spend. To further complicate things, the rise of mobile payments and new operating models has led to increased competition between traditionally brick-and-mortar banks and online or mobile banks.

As these changes continue to unfold, traditional banks and credit unions must adapt to stay competitive. The future of banking lies in providing a more active customer experience through innovative solutions and CX strategies.

Although trends have been evolving over the last few years, an emphasis on digital transformation has been a common overarching theme. Banks and credit unions are well aware of the need to innovate drastically – but how well is the banking industry doing as a whole?

Key trends at a glance

The era of digital dominance

Mobile banking is no longer just a trend for the digitally native; it has become the universal standard for engagement. According to a November 2025 survey and national data from the American Bankers Association (ABA), 54% of Americans now use mobile apps as their primary banking channel – a figure that has more than doubled since 2017.

Customer behavior has changed with the rise of digital banking as users now prioritize speed, convenience, and the ability to access complex support through their mobile devices. While Gen Z leads this shift, ABA research indicates that over 50 percent of Gen X and nearly 40 percent of Baby Boomers now also rely on mobile apps as their top management tool.

However, a "Productivity Paradox" still exists: the human gap remains. According to the Unblu modern banking whitepaper, 70% of bank employee time is still locked in legacy systems and operational tasks, leaving only 30% for direct customer interaction. This is why banker priorities are shifting toward automation that actually serves the front line.

We are also entering the "Rise of the Machine Proxy" and the "zero-click" era. Forrester predicts that by mid-2026, human visits to bank websites will drop by 20%, while machine-initiated traffic from personal AI agents will surge by 40%. To avoid falling behind, financial services leaders must transition from isolated digital tools to a Unified Engagement Layer. This ensures that every interaction – whether machine or human – is consistent, secure, and trust-driven.

Digital trends and demographic shifts

The shift in the banking landscape is redefining how different generations perceive and interact with financial institutions. For younger demographics like Gen Z and Millennials, convenience, speed, and self-service are front and center.

That's not to say Gen X and Baby Boomers aren't embracing digital banking. However, there is greater demand for clarity, trust, and accessible support. The Boomer generation is increasingly happy to carry out routine tasks like checking balances or transferring funds through mobile banking apps. But when it comes to more in-depth scenarios, they still expect access to human advisors through in-app collaboration.

In fact, the desire for real-time, human support remains strong across all age groups. Gen Z and Millennials show a high preference for conversational interfaces, while Baby Boomers still lean toward physical branches or phone support.

The future banking trends already in progress

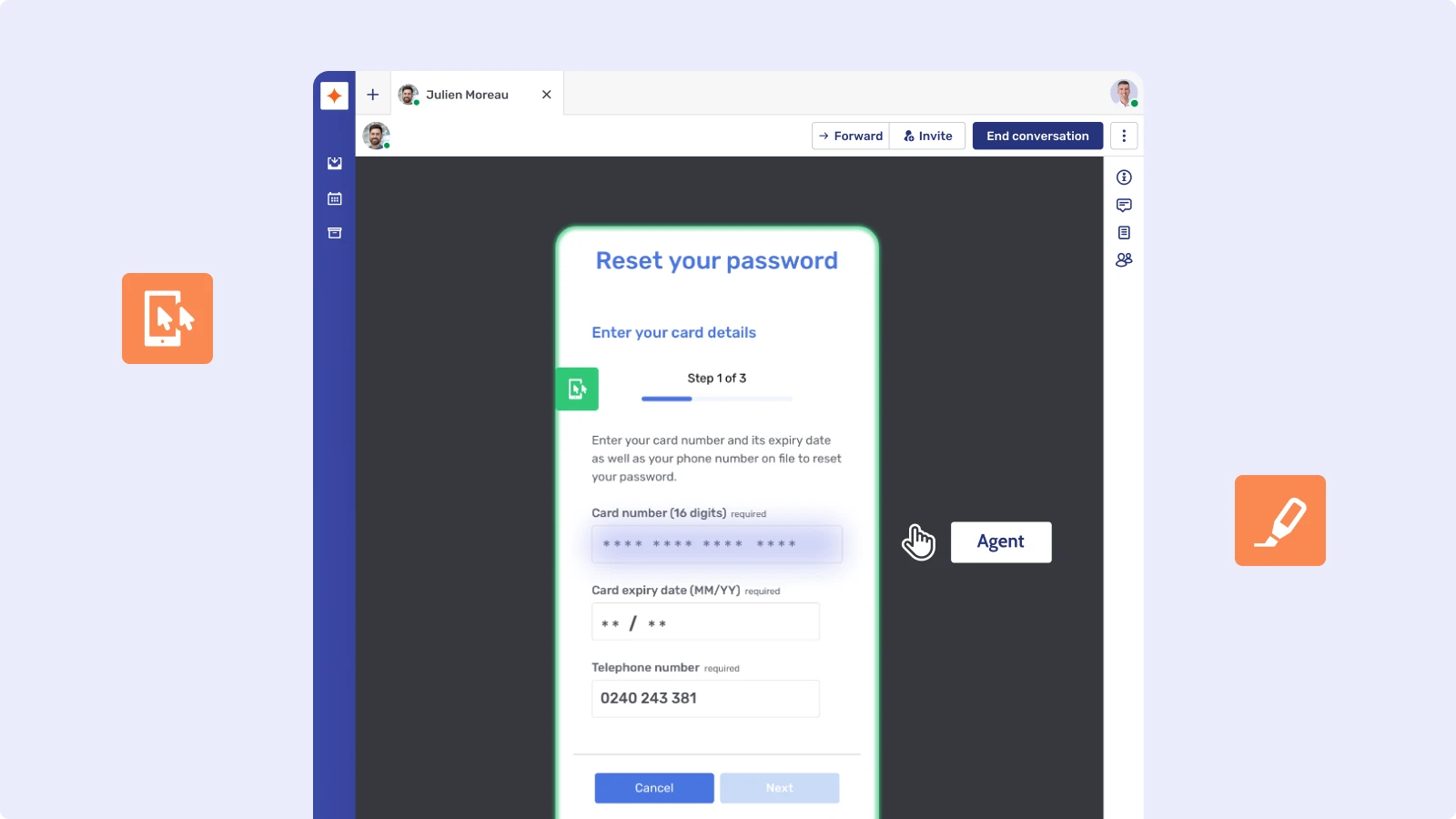

1. Omnichannel and mobile-first or you don’t exist

The number of digital banking users continues to rise. As with previous years, the key trend towards mobile has reached a stage of almost complete ubiquity. One report found that digital touchpoints have become the most important engagement channel that account holders have with their financial institutions.

Technologies driving innovation in digital banking include mobile co-browsing, secure messaging, and real-time video, which transform transactional apps into collaborative environments. Integrating these collaboration tools allows banks to move from being a "utility" to a strategic partner in the customer's financial life.

By equipping agents with Co-Apping, banks can bridge the satisfaction gap and improve customer satisfaction scores, turning routine sessions into high-value advisory moments.

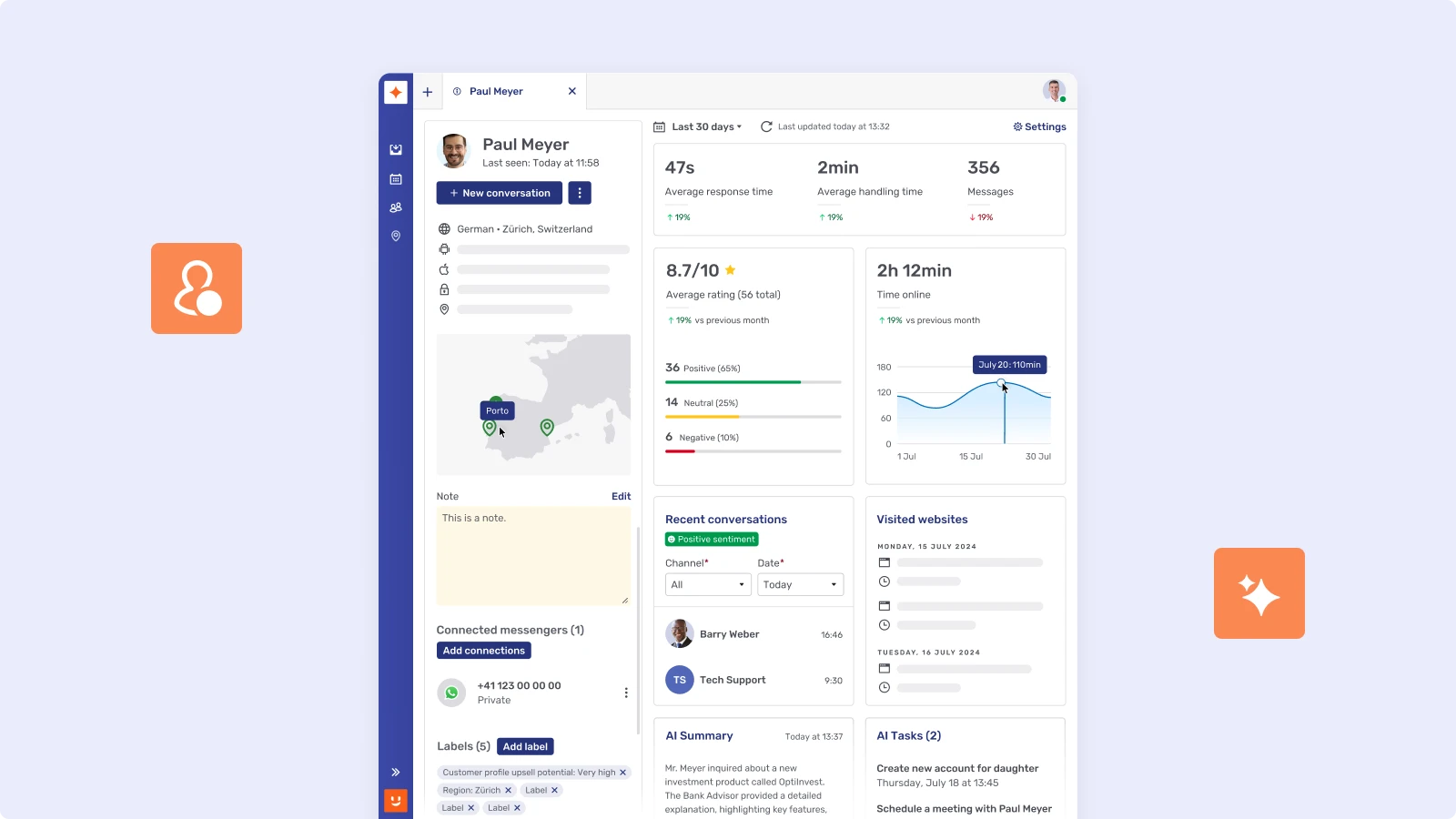

2. Orchestrating the "Digital Memory"

A primary driver of friction in 2026 is the "Hand-off Problem." Accenture reveals that 64% of consumers still rely on physical branches when digital channels fail, yet they are forced to "start over" due to a lack of real-time data capabilities in orchestration.

Banks must develop a "Digital Memory" – the ability to maintain a single, continuous conversation across every touchpoint. With 86% of banking executives now prioritizing a seamless user experience across all channels, the winner will be the institution that views customer service as a primary value driver.

3. The Rise of Agentic AI

Best practices for banks implementing digital transformation involve using AI to automate the "administrative load" rather than just replacing human support. In 2026, the standard for digital interaction has officially graduated from Generative AI to Agentic AI.

These advanced autonomous agents move beyond the chatbot resolutions of the past to act as expert team members capable of independent reasoning and complex problem-solving. To achieve this, many banks are moving their infrastructure to cloud computing to support the massive data needs of these agents.

- The Productivity Dividend: McKinsey indicates that Agentic AI is returning 10–12 hours a week to bankers by automating "admin load," potentially improving client coverage by 40%.

- The Machine-Initiated Surge: We are entering an "Agent-to-Agent" economy. Forrester predicts that human visits to bank websites will drop by 20% as machine-initiated (AI agent) traffic surges by 40%.

This efficiency is most effective when paired with tools that handle routine servicing, such as the Unblu AI-powered Workbench, which automates compliance monitoring tasks to free staff for high-empathy advisory roles.

Leaders must transition from "cost-minimization" AI to "Value-Creation" AI. The goal is to use generative artificial intelligence and AI-driven analytics to reduce regulatory compliance report preparation time by up to 50%, freeing up staff to focus on high-empathy advisory roles.

4. Solving the "emotionally devoid" digital crisis

While the "plumbing" of digital banking is complete, the "soul" of the customer experience is in crisis. In 2026, the retail banking landscape has moved into an era of emotional orchestration. Most institutions have achieved functional digital efficiency, yet Accenture reports that these channels are often "functionally correct, but emotionally devoid."

For C-suite leaders, the competitive edge no longer lies in digital availability, but in customer loyalty and advocacy-driven growth. Banks that achieve high customer advocacy grow revenues 1.7x faster than their peers. The strategic goal is to move from transactional interfaces to interaction layers that facilitate "emotional resonance" through a seamless blend of human empathy and digital customer experience precision.

5. From Artificial Intelligence to "trusted intelligence"

In 2026, trust is no longer just about keeping money safe; it is about the "Trust-Value Flywheel." While consumers still trust digital banks less than traditional banking incumbents to safeguard their personal data (66% preference for banks, this trust is being tested by the "emotional void" of digital interactions).

Banks that provide Open APIs to allow customers to view their full financial picture can help bridge this gap by offering more transparency and financial inclusion.

- The Advocacy Gap: Accenture found that 73% of customers now engage with multiple financial brands beyond their primary institution because their main relationship feels "transactional, not relational."

- The Reassurance Preference: Despite 53% of consumers regularly using Generative AI, the "human-in-the-loop" remains a trust anchor. Research from Deloitte shows that customers still prefer high-touch human support for "clarity and reassurance" in complex situations like home purchases.

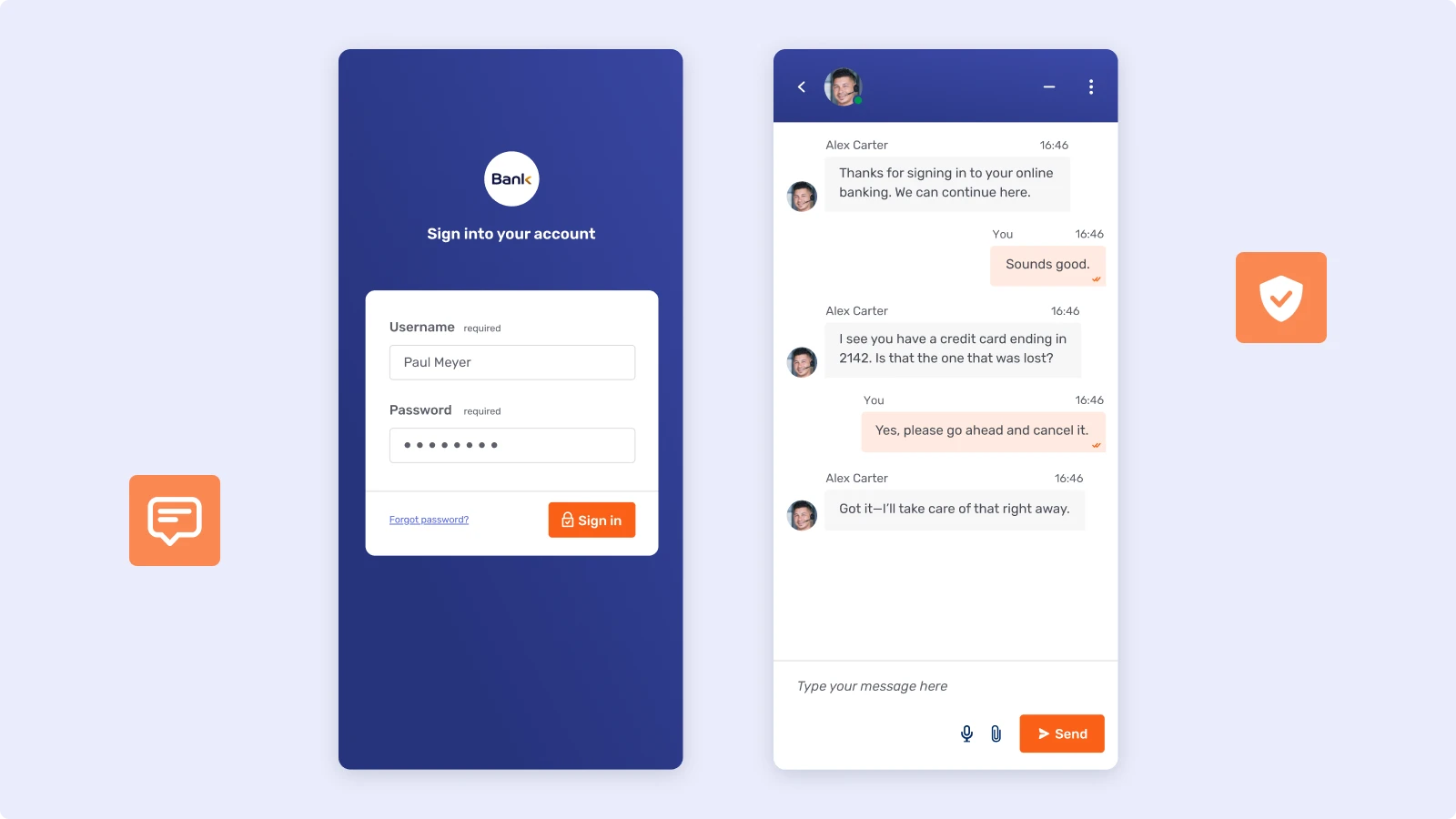

Security challenges associated with digital banking require a move toward "trust by design," where every interaction is authenticated and protected within a secure, compliant framework – from clear in-session biometric security cues to verifiable message delivery. Solutions like Unblu’s Secure Messenger enable this by providing a familiar chat experience that remains fully compliant and auditable, ensuring that trust is a repeatable operational outcome.

The final word: Where are we in 2026?

The leap the banking industry has taken from last year to now is defined by a fundamental shift: the rise of Agentic AI. We have moved past the era of passive digital transformation into an age where financial technology doesn't just wait for a user to click – it anticipates. The "emotional void" of early online banking is finally being filled by what we now call "trusted intelligence."

From transactions to trusted intelligence

In this digital age, providing elevated customer experiences is no longer a luxury; it is the primary differentiator. Whether a firm is a legacy institution or one of the agile challenger banks, the goal is the same: move beyond "Artificial" interactions and toward meaningful digital experiences. By intelligently leveraging customer data, banks can now provide personalized recommendations for financial products that actually align with a user's life goals.

High-value use cases

The most successful use cases we’re seeing in 2026 involve a proactive approach to a customer's financial health. For a small business, this might mean an AI agent that monitors cash flow in real-time, suggesting a line of credit before a shortfall even occurs.

Redefining the value chain

While banks must remain hyper-vigilant regarding fraud prevention and risk management, the focus has shifted toward the human side of the ledger. Modern digital banking experiences ensure that support channels and the contact center are no longer seen as "cost centers" to be minimized, but as vital touchpoints for building loyalty.

Banks that succeed will be those that view customer service as their primary value driver. By humanizing their digital footprint, they aren't just managing money – they're claiming market share through resonance and trust.