.png)

While the move to digital preceded the events of 2020, it’s undeniable that the unique conditions of the pandemic accelerated it. Across the world, banking customers who were reluctant to use digital channels or applications quickly found they had no other choice.

This increased uptake in digital channels had a knock-on effect and retail banks or other financial institutions had to race to improve their digital offering. Even those that had invested already in transformation initiatives were put to the test as these services saw increased usage.

In fact, only 35% of global banking executives report that their digital initiatives are successful. More worryingly, 12% only have plans to develop transformation initiatives and 6% have no plans at all.

This is of course at odds with the overarching trend, which shows that customers are using digital channels more often. The same Forrester report shows that 77% of Canadian customers, 71% of US customers, and 69% of Spanish use their online banking services at least every month. There’s no doubt that digital is here to stay.

How customers are using digital channels

Even with the outliers mentioned above, the fact is that the majority of retail banks have maturing or mature digital transformation and online banking initiatives. It’s also true that they are being received positively by customers.

However, when we look more closely at the statistics, there’s room for improvement with regard to customer behavior when using digital channels or online banking. Looking specifically at mobile usage, for example, 30% of survey respondents from a Forbes study claim to use mobile applications for transferring funds, 22% for paying bills, and other small percentages use it for peer-to-peer payment (9%) or to find nearby ATMs (8%).

There’s a similar trend with regard to artificial intelligence tools like smart speakers for financial transactions or resolving simple customer issues. Among those who use smart speakers, 30% of US customers use it frequently to check their bank account balances. In the UK, the same percentage use it for simple transfers to another individual and 22% of Canadians use it to transfer money between accounts.

Using Co-Browsing technology for complex transactions

What’s notable about these statistics is the apparent reluctance people have to carry out more complex transactions – such as the entire loan application process – remotely. While, by their nature, these will happen less frequently, there’s still an issue of trust or confidence when making such important decisions online. This would explain the somewhat contradictory statistic where, while 24% of customers expect to visit branches less often, an incredible 82% still believe having a branch nearby is extremely or very important.

When taking out a loan, customers need the reassurance that only a human agent can provide. Beyond that, they need them to be able to interact and collaborate with them at the same level as if they were in the same room. Self-service tools are great for initial research and direct messaging channels like Live Chat can help resolve simple queries, but the closer they get to the moment of truth, the more important a high-touch approach becomes.

Collaborative browsing or “Co-Browsing” software represents the missing link in the customer journey for complex transactions like loans and for any subsequent customer onboarding. This browser-based technology allows the customer and advisor to share and interact with the same document or web page, without ever leaving a secure, encrypted environment. We’ve gone into detail before about what Co-Browsing support is and its specific features. In essence it offers the customer an experience that not only emulates an in-person experience but enhances it, boosting trust and effectively leveraging the moment of truth.

How can a Co-Browsing solution boost loan applications?

No two customer journeys are the same. In another post, we explored what it could look like for customers to take out a mortgage using entirely digital channels, which also includes using a Co-Browsing tool. That customer journey would best represent someone who is already familiar and comfortable with online tools and communication channels.

However, what happens when a customer gets in contact through more traditional means. This target is more likely to fall into the 82% who consider having a branch nearby to be extremely important. Given the trend towards branch consolidation, what can retail banks offer these individuals to complete the entire loan application process online while dealing with any doubts or worries they may have?

1. Inbound call

When applying for a loan, traditionally a customer would need to make a phone call to their bank to solicit information about the bank’s different loan products. They would then need to listen to the agent’s sales speech and most likely make a trip to the branch at some point.

Listening to all this information from the end of a phone line is not particularly engaging for the customer, who is likely to drift off and miss important information.

Nor is it a particularly streamlined or efficient way to begin the loan application process. A long period of time could elapse between the initial conversation and the point when the customer finally comes into the branch to continue the application.

2. Elevating the conversation

Instead, after initiating a conversation with an advisor with access to the Unblu platform, the customer is provided with a PIN code to ensure a high level of security. This code enables Embedded Co-Browsing and allows the customer and advisor to connect within a Co-Browsing session.

Or, in the case of the bank BNP Paribas, the PIN code link is displayed in their homepage footer. This PIN code is an identifier that can be used to match a customer with an advisor.

Customer and advisor can then join a Co-Browsing session together to continue the conversation with the added help of a visual context.

3. Providing remote advice

With the Embedded Co-Browsing solution now activated, the advisor is able to see exactly what the customer sees in their browser. This visual context puts advisor and customer on the same page to provide high-quality real-time assistance, which makes the conversation far more productive and efficient.

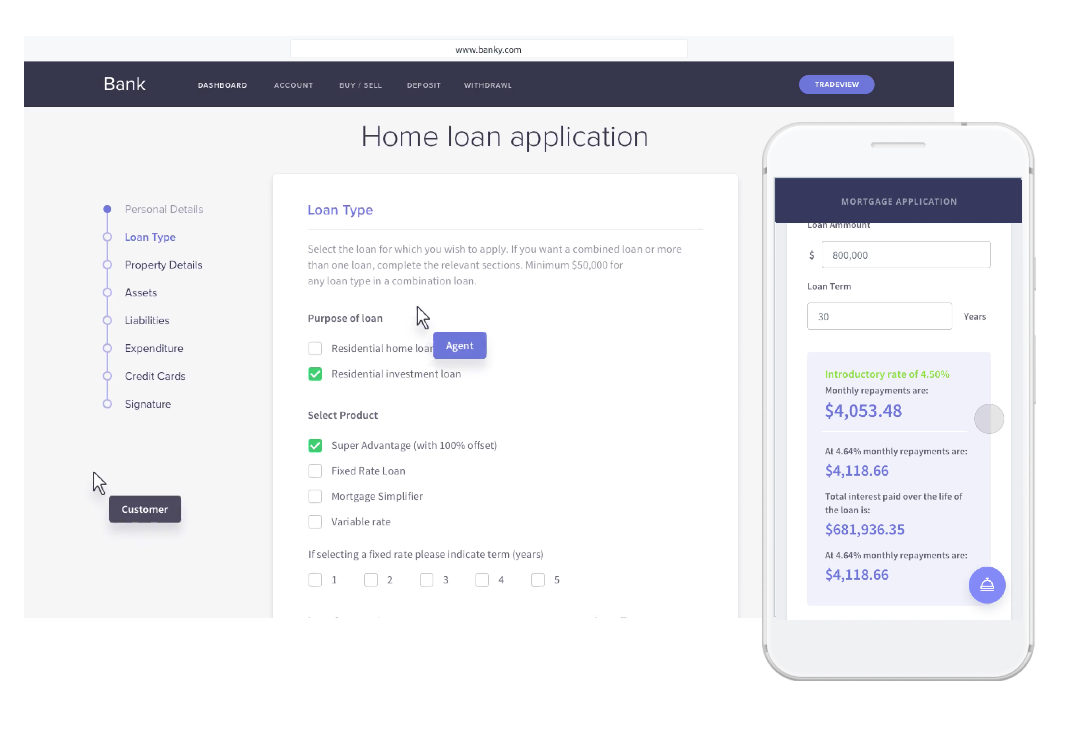

The advisor can use the mark and highlight tool to point out relevant information on their screen as they guide the customer through the decision-making process, showing rather than telling them different details.

Customers and advisors can even use a loan simulator together to help understand how different deals would work and better understand the application process. This makes the conversation even more personalized and specific.

4. Multiple interactions, one seamless journey

This onboarding process may require more than one interaction and the customer experience should allow for that. The customer will likely want to sleep on it before making any decisions. In fact, this process could stretch over several days and weeks as the customer gathers more information and thinks about what they need and want.

Every new interaction builds on the previous one. A new advisor will have access to the conversation history so they can start up where they left off before.

This journey may also make use of different digital tools as part of an omnichannel customer journey. For example, for their next conversation, a customer might want to move to voice or video chats for greater reassurance or they might want to ask a few simple questions via Secure Messenger.

5. Secure collaboration with history

During the Co-Browsing session any sensitive information will be shielded from view using field masking, ensuring that any remote access remains safe and secure.

Once the customer has made the decision to buy a particular loan product, an advisor can share the application form through the document Co-Browsing collaboration tool. Using this tool, the customer support agent and customers can co-edit the form together.

6. Digital signature

To finalize the application and ensure it’s compliant with all financial regulations, the advisor can request the prospect for e-signature and ID recognition. E-signature software such as DocuSign can be integrated into the customer journey in a simple and streamlined way with no need for them to download anything.

This allows the agreement for even complex forms to be both carried out and concluded online. There’s no requirement for the customer to come into the branch to complete the entire process, which is convenient for both them and the loan officer.

Co-Browsing & Unblu

Unblu’s Co-Browsing solution elevates the customer engagement experience, creating opportunities for more flexible and meaningful interactions. Learn more by booking a demo today.

Thinking outside the bots

Download