Interaction Management Hub

Interaction Management Hub Secure Messenger

Secure Messenger Video & Voice

Video & Voice

Understanding and defining a client's journey is no easy task. Because it goes beyond internal processes, getting an end-to-end picture can be challenging. That being the case, it’s easy to overlook some of the smaller stepping stones in the client journey—especially if those steps don’t appear to deliver any value or worse, are perceived as a cost center. Meanwhile, overlooking a “bad” step within a client journey can easily negate the efforts and investments made on more profitable ones.

A good industry case to examine is one specific practice from the online retail industry; namely, the repurposing of customer returns. By unpicking how that practice positively impacts upon the entire client journey, we’re able to see the tremendous effect it can have on customer loyalty, peer recommendations, and profits.

So, what can financial services and investment firms learn from retail? In this article, we’ll explore the possibilities by building upon the work from HBR Webinar “Omnichannel Retailing: Reverse Logistics and Customer Loyalty” that leverages the expertise of Dr. Dale S. Rogers, as well as the UPS study “Rethinking Online Returns”.

The retail returns rush: converting convenience into loyalty

The retail industry has long since begun its journey towards integrating digital channels into client journey strategies. Today, it is standard for retailers to strive for the customer experience holy grail: delivering omnichannel experiences.

Among an incredible diversity of improvements and initiatives, there is one that stands out for its staggering CX value: client-friendly return policies, and associated reverse logistics. While Amazon was one of the first well-known retailers to blaze that trail, many retailers have since embraced the benefits of implementing client-oriented return policies. Offering unparalleled flexibility has made it easier than ever to return an online purchase.

This begs an obvious question: why? Why would a company, whose business is to sell products, facilitate returns? It’s clearly part of the client journey—but at first glance, it is not a very profitable one.

Let's consider the issue from a pragmatic standpoint.

- Step 1: Your online advertising did its job.

- Step 2: Your website did its job.

- Step 3: Your logistics infrastructure did its job.

- Step 4: Your payment service did its job.

- Step 5: The money is in the bank, but the client requests a return. By granting the client an easy, hassle-free return process, you make it easy for that money to be refunded, as well as creating pressure on your logistics infrastructure.

As any supply chain beginner will know, this is no easy exercise. Short of being able to deny a return, companies could (and some still do) make it very difficult and painful for clients to return products bought online. Naturally, this decreases the likelihood of having to refund clients.

Dealing with returns is costly, creating a challenge for any company. And yet, every successful retailer—big, medium or small—is adopting a more positive approach to returns. This involves making it easier and easier for clients to return their purchases, integrating returns into their strategies in the interest of forming a long-term relationship with the customer.

So what’s the advantage?

According to the UPS study “Rethinking Online Returns”:

- 95% of shoppers will shop again if the returns policy is seen to be convenient.

- On the contrary, 95% of shoppers are not likely to repeat their custom if the returns policy isn’t convenient.

- The returns policy is a top customer priority. 88% of shoppers look at it when shopping online, and 67% check it once more before hitting the buy button.

The new consumer environment

Those facts can be explained by rising client expectations coupled with an abundance of diverse information. As Logistics & Supply Chain Management Professor Dr. Dale S. Rogers has pointed out: “Think of any shopping experience—a lot more information is available to the customer”. This is valid for retailers as much as it is for banks, insurance firms, and other institutions. Whether it’s products or services, it has become easier to compare offers, meaning consumers have developed the habit of comparing and constantly seeking alternatives.

As client behavior becomes less linear and predictable, there is an added degree of complexity for omnichannel experiences. Nonetheless, they can generate significant value if an organization is ready to offer a diversity of channels for a holistic, consistent experience.

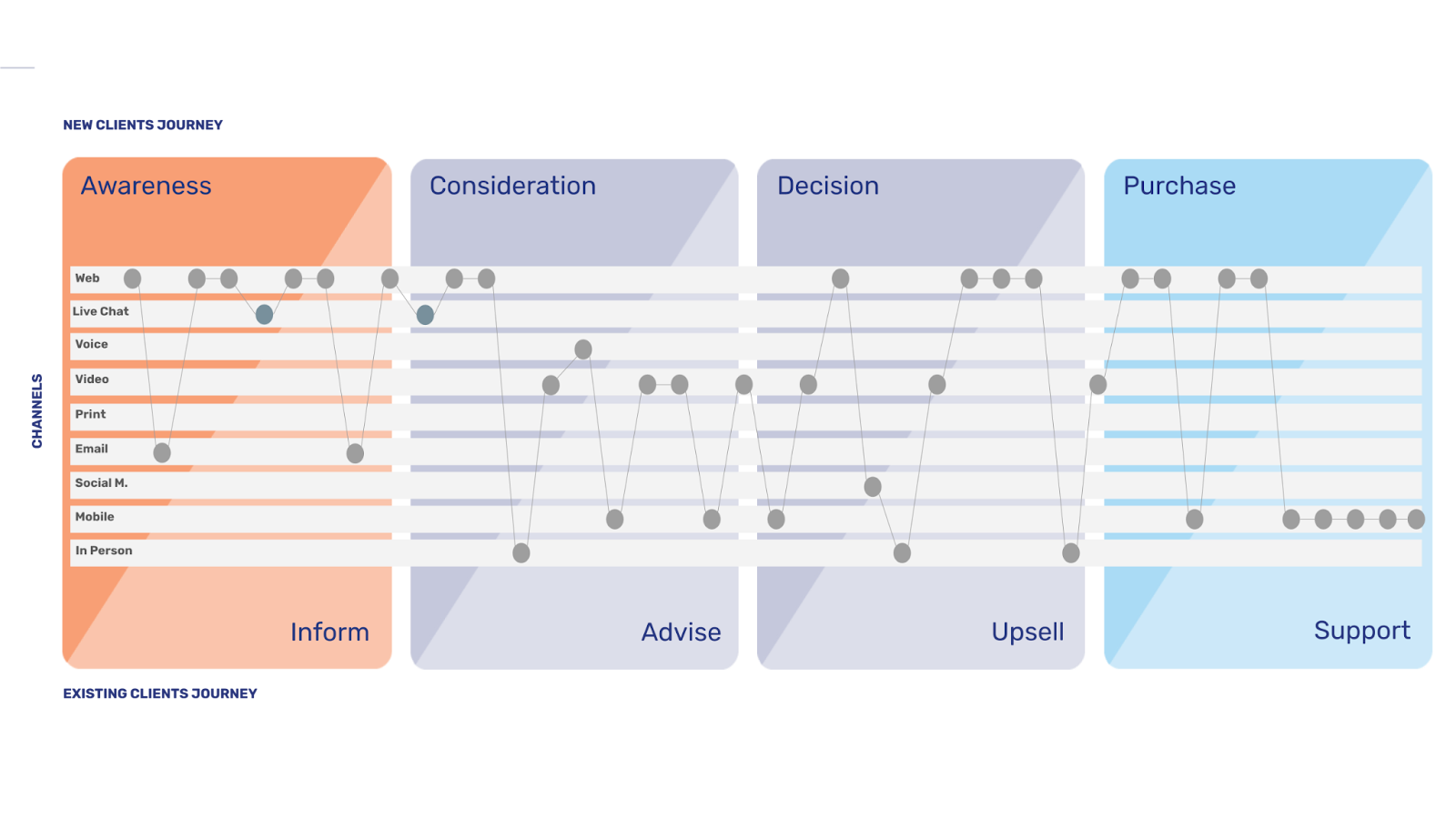

At this point, it becomes necessary to add a new layer to the traditional way of illustrating a sales/client journey. The more simplistic visualization doesn’t capture the diversity in combinations of touchpoints leading to a sale or serving existing clients.

However, the profusion of choice and information isn’t so much the cause as it is the enabler to those behaviors and habits. In fact, according to Dr Dale S. Roger, “returns have always been a concern”. This finds its roots in the fact that clients—and humans generally—tend to favor relationships with low risks. Thus, when an organization is successful in creating a low-risk relationship, it starts building loyalty. Loyalty will in turn become a powerful vector in creating and maintaining a long-term relationship and generating more profits, as people become willing to pay a premium in return for a low-risk engagement.

Superior CX is a cross-industry strategy

Retailers are funneling their efforts towards meeting expectations throughout the complete client journey, proactively supporting customers along the way. It’s a simple equation: superior CX and its underlying processes are driving profits, because one positive experience sets up many more in the future.

Parallels aren't so easily drawn between industries, and it can be difficult to see how lessons from one can also serve others. However, the key principles of CX remain the same. Loyalty, long-term relationships, embedded experiences, proactive behaviors, and omnichannel strategies are all relevant—and that goes for any company looking to balance physical and digital engagements in a cohesive client experience.

How to get started: A non-exclusive list of tips

- Refine the lesser or “bad" steps in your client journeys for:

- becoming a new client,

- asking for help,

- receiving educational and valuable advice

- Assess the hoops that your clients need to jump through in order to execute a task. Consider:

- how that number could be decreased

- how you could create a linear experience

- how you could remove uncertainties or delays

- how you could meet clients on their preferred channel of communication

- Think about the elements of the client relationship around complex and profitable products that might not be satisfactory from a client perspective.

- Consider the number of channels, touchpoints available to clients, and how to maintain a consistent user/brand experience independently of the path taken.

For more insights, reach out to the Unblu marketing team (no strings attached!) and we’ll see where we can help.