Interaction Management Hub

Interaction Management Hub Secure Messenger

Secure Messenger Video & Voice

Video & Voice

Customers want choice. They want flexibility. Omnichannel banking is perfectly positioned to offer this level of adaptability, allowing customers to choose their preferred means of communication with their bank on that particular day, whether it’s sending a text on the go or chatting via video call with their advisor. This boosts satisfaction and loyalty, which, in turn, drives conversions and sales.

In this post, we’ll take a look at key statistics and trends related to omnichannel banking. We’ll see how the COVID-19 pandemic has changed banking habits and preferences, discover an increased demand for flexibility and personalization in both retail and private banking, and see how client preferences have evolved regarding self-service vs. human help.

How the pandemic has changed customer preferences

.png)

The COVID-19 pandemic has accelerated a shift in consumer demands. It forced customers to experiment with banking online—and many of them found they preferred it. We’re also witnessing increased demand for an omnichannel service whereby customers can interact with their bank via a range of channels as part of a seamless and digitally-enabled journey.

Online banking, particularly mobile banking, has boomed since COVID-19. 76% of US online adults used online banking on a computer at least once a month during the pandemic. 61% did so on a smartphone (Forrester, 2021).

While only 15% of consumers had spoken to an advisor via video call pre-COVID-19, 46% said they would be up for doing so when branches reopened. 35% said they would prefer this to a face-to-face meeting (Accenture, 2020).

71% of European private banking clients now prefer multichannel interactions while 25% want a fully digitally-enabled private banking journey with the option of remote human help when necessary (McKinsey, 2020).

New demands for better retail banking services

Today’s retail banking customer wants greater flexibility. They expect 24/7 service and multi-channel interactions. There’s a greater preference for using online services, even for things traditionally done in branches, like opening a new account. Interestingly, those customers who are inclined towards digital banking also seem to be less loyal towards their bank.

76% of customers expect an omnichannel experience and 59% of customers expect on-demand, anywhere anytime customer service (Capgemini, 2021).

47% of customers say they would open a new bank account online via their computer. 37% would do so via a mobile app or website. 47% would prefer face-to-face with an advisor (Accenture, 2020).

55% of ‘digital-centric’ consumers say they “definitely will” reuse their primary bank for their next financial services purchase, compared to 61% of ‘branch-dependent’ consumers. (J.D. Power, 2020).

Private banking clients are willing to explore online services

In private banking, clients are seeking more digitally-advanced and personalized services, with support that goes beyond just investments. These high-net-worth consumers are increasingly willing to experiment with new forms of banking, especially younger clients who are notably attracted to virtual advisory services.

51% of HNWIs say they are not satisfied with their firm’s personalized offerings or digital interfaces. 36% state that a company’s lack of value-added services might lead them to look elsewhere (Capgemini, 2021).

49% of affluent US investors say they’re willing to try new things, perhaps signaling increased openness to integrating digital and physical experiences (Forrester, 2021).

50% of HNWIs under 40 would like the option to select purely virtual advice from their firm, compared to 39% of HNWIs overall (Capgemini, 2021).

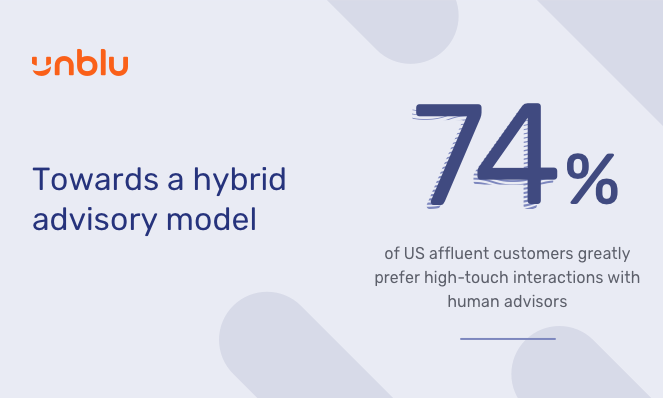

Towards a hybrid advisory model

While some HNWIs are exhibiting a stronger inclination to manage certain banking tasks themselves using self-service tools, as customers become more affluent, they tend to favor human advisors over digital tools due to their need for increasingly complex financial advice.

71% of HNWIs in Asia-Pacific (excl. Japan), 63% of HNWIs in Europe, and 53% of North American HNWIs say they prefer to conduct transactions and access information independently, rather than via an advisor. (Capgemini, 2021).

US affluent customers greatly prefer high-touch interactions with human advisors (74%) to digital self-service tools (26%). (Forrester, 2021).

Omnichannel Banking & Unblu

Discover how building a personal and omnichannel customer service can help you to stand out from the competition and boost customer satisfaction and loyalty with Unblu’s conversational banking platform. Book a demo today.